A Promissory Note is a legally binding document that outlines the terms of a loan made by a Borrower to a Lender. In the note, the borrower promises to fully repay the lender within the allotted timeframe.

It ensures the parties have a thorough and comprehensive written record of the deal and their intentions and includes all the terms and conditions of the loan transaction. Therefore, the note should be completed before any money is exchanged. The record serves as a formal record of the transaction as well.

What Is a Promissory Note?

A promissory note is a legally binding contract between a borrower and a lender that specifies the borrower’s promise to repay the lender with a certain amount of money. Depending on the terms of the note, that payment may be made immediately or over the course of a certain period of time.

When might you use a promissory note, for instance?

A promissory note is also referred to as a:

Types of Promissory Notes

Promissory notes come in two main categories: secured and unsecured, and the difference between the two will determine how the note will be enforced in the event of non-payment.

Paying Back the Promissory Note

You must repay the loan given through a promissory note. But there are a couple of options for doing that. Promissory notes can be negotiated more effectively if you are aware of your options and the repercussions of missing or making late payments.

What are the options for paying back a note?

You have two options for paying the promissory note: in full or in installments.

When choosing an installment payment option, the borrower pays the lender back over time in predetermined installments, such as 12 monthly payments over the course of a year. A promissory note can also be repaid in instalments with a final “balloon” payment made at the conclusion of the predetermined repayment period. With a loan of $5000, the borrower could pay $500 each month for six months before making the $2000 final payment.

When paying off the entire balance of the note at once, you have two options: pay by the due date specified on the note or pay the lender “on demand.” When the lender asks for payment, if there is a “due on demand” payment option, the borrower must pay.

What is prepayment of the promissory note?

Prepayment is the ability of the borrower to pay back the loan before the due date. At that time, they are free to pay back the entire loan or just a portion of it. Some lenders demand that the borrower first send them a written notice

What happens if the borrower misses a payment or pays late?

Late fees and other penalties may apply to borrowers who miss a payment or pay after the due date. These will be determined by the terms of the promissory note and must also adhere to the laws governing money lending. For instance, it would be unlawful to charge an interest rate that is higher than the state’s usury rate.

Selling and Transferring Promissory Notes

A promissory note is classified as a ‘negotiable instrument’. Signed documents that promise a certain party money are known as “negotiable instruments.” They can be used in place of money because they are naturally transferable documents.

Let’s say Larry lends Betty $100,000 so she can open a 3D printing business. According to the promissory note Betty signs, Larry must receive $1,500 from her each month, with $500 going toward an annual interest rate of 6% and $1,000 going toward principal.

The loan term is 100 months. However, Larry decides he wants the money back sooner than expected 20 months later. He wants to invest it in his dog-walking business.

The remaining amount, which is made up of Larry’s note’s principal of $80,000 and future interest payments of $40,000, can be obtained by selling the note. But he will need to sell it at a discount. He may sell it to Lisa for $90,000 total. Lisa will receive Betty’s monthly payments after that for 80 months and profit $30,000 from the transaction.

Promissory notes are transferable by nature, but the borrower may include clauses in the contract that prevent transfers.

Tax Benefits of Promissory Notes

For tax purposes, you might want to record in some circumstances whether the money you’re lending is a gift or a loan.

For instance, the IRS currently permits gifts of up to $16,000 per person and per year without incurring gift tax. This limit is called the annual gift tax exemption. For instance, in order to lower their estate taxes, your grandparents could annually give each of their grandchildren a combined $32,000. Couples can also make $16,000 in gifts to one another each year and deduct that amount from gift taxes.

Additionally, the $16,000 annual gift limit does not apply to medical or educational expenses that are paid directly on behalf of someone else. There are many factors to take into account if you want to exempt gifts or estate from taxation because the IRS levies such a sizable 40% gift and estate tax [1] To learn more about gift taxes, visit the IRS website and look through the Frequently Asked Questions section. [2].

Minimum IRS Applicable Federal Rates (“AFR rates”), which are released each month, apply to family loan agreements. Fortunately, the IRS’s required rates are typically lower than those for commercial mortgages, and all interest and principal payments are made to the family. So, if you’ve reached your annual giving limit, you can use a promissory note to assist a family member who is in need.

What Are Promissory Notes Used For?

If you’re borrowing or lending money, you should draft a promissory note. Payment information, interest rates, security, and late fees ought to be included. You can use various promissory note types for a range of purposes, including:

Promissory Note vs. Loan Agreement

Creating a deal between a borrower and a lender using promissory notes and loan agreements can be efficient and legal. In general, you should choose a loan agreement for more complex loan requirements and promissory notes for simple loans with simple repayment structures.

How To Write a Promissory Note

For a legal promissory note to be enforceable, it must be properly drafted. It should have the following details and clauses:

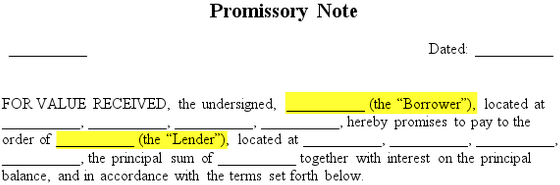

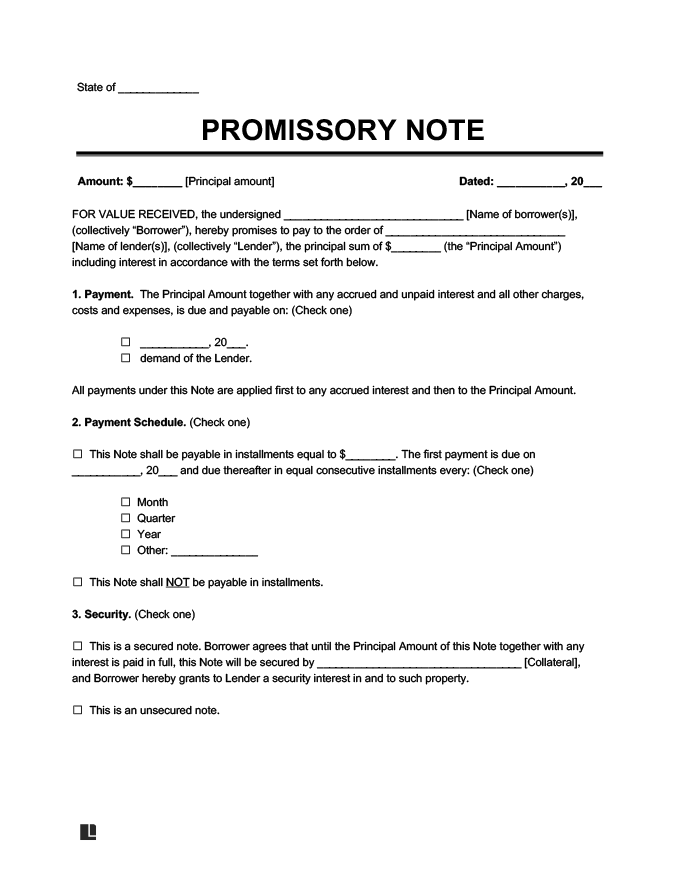

Step 1 – Full names of parties (“borrower” and “lender”)

A typical promissory note should identify the parties receiving the funds or credit (the “borrower”) and those responsible for collecting the loan repayments (the “lender”). A promissory note must only be signed by the borrower, but it is advisable to also include the lender’s signature.

Step 2 – Repayment amount (“principal” and “interest”)

The repayment amount is the sum the borrower must payback. Regardless of whether it’s a straightforward promissory note or not, it must always list the amount borrowed. The note should state if interest is being charged by the lender. Also, include whether the interest is compounded monthly or yearly.

Visit the Wells Fargo Rate and Payment Calculator, Prosper Loans, or Lending Club to compare personal loan interest rates if you’re unsure of the amount to charge. The principal and monthly interest payments over the loan’s life can then be seen using an amortization calculator. Most states have regulations that limit the amount of interest you can charge.

Before drafting your note, research the interest requirements in your state. For instance, in Texas and California, the interest rate on a promissory note is limited to 10%. Promissory notes in Florida are subject to interest rates of up to 18% for loans under $500,000 and 45% for loans over $500,000.

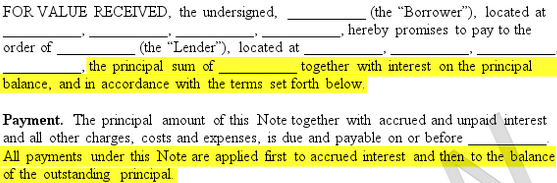

Payments made on the note are applied first to the interest and then the principal.

Step 3 – Payment plan

The promissory note should detail the borrower’s repayment plan. That could be by a certain date or on-demand.

Four Types of Repayment Options

| Installment Payments | Installments with Final Balloon Payment | Due on Specific Date (“Lump Sum”) | Due on Demand (“Payable on Demand”) |

|---|---|---|---|

| Specific due date | Specific due date | Specific due date | No specific due date |

| Payments for principal and interest are made at regular intervals | Payments for interest only are made at regular intervals, principal amount due on maturity date | Entire amount owed, including interest, is paid all at once | Entire amount owed is due whenever the lender wants his or her money back |

| Example: $1,500 monthly payment actually consists of $500 towards the outstanding principal and $1,000 towards the interest with $1,500 due on the maturity date | Example: $500 monthly payment is applied only towards interest and full $10,000 loan amount is due on the maturity date | Example: $10,000 loan for a friend’s small business is due on a specific date | Example: $10,000 loan for a friends small business is due at any time or whenever financially feasible |

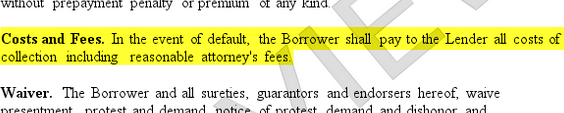

Step 4 – Consequences of non-payment (“default” and “collection”)

Suppose the borrower is unable to make the repayments on time and breaches the agreement. If so, the lender may enforce the promissory note and require payment in full (or the collateral, if the borrower used an asset as security for the note).

The lender may take legal action against a nonpayer. If the borrower loses the lawsuit, they will be responsible for the promissory note as well as the costs of debt collection. That includes fees the lender paid to an attorney.

Step 5 – Notarization (if necessary)

A promissory note isn’t required to be notarized. However, it’s wise to check your state’s laws to confirm any requirements for witnesses and signatures.

Step 6 – Other common details

A promissory note may include additional provisions, such as:

- if the borrower becomes bankrupt

- if the borrower fails to make payments

- if the borrower passes away

- if the borrower wants to pay off the note early

- if the borrower sells a significant amount of its assets

Each party should receive a copy of the note, and the original should be kept in a safe place.

What To Include in a Promissory Note

Knowing what to include in a promissory note will help to ensure that it is legal and enforceable in court.

Information About the Borrower and Lender

An individual or a business, such as a corporation or LLC, can serve as the borrower, lender, or both. Any company that is one of the parties to the promissory note must have a representative sign on the company’s behalf.

Include the full legal names and addresses of the lender and borrower in the promissory note as part of the contract information.

If there are multiple lenders or borrowers, each party’s name should appear on the note.

Having a cosigner or guarantor is optional. It offers protection in the case that the borrower defaults. If the borrower’s credit is in doubt, the lender might insist on a cosigner as additional security.

If the borrower defaults, this person will jointly sign the contract and be liable for the debt. A cosigner typically has excellent credit and stable finances.

The lender must give the borrower’s repayment schedule as well as the principal amount, interest rate, and repayment method they will use to pay back the loan. There should also be additional conditions, such as what happens if the borrower defaults on the loan and information about prepayment.

Collateral May be Required

Any asset used to secure the promissory note and worth more than the loan amount is known as collateral. Although it is not required, many lenders will ask for it. Without collateral, lenders may charge a higher interest rate.

Consider Adding the Lender’s Signature

By default, the only signature needed is the borrower. It’s optional to include the lender’s signature.

Example of a Promissory Note

Download a free promissory note template below. You can choose to make it either secured or unsecured.

Promissory Note Frequently Asked Questions

No. The notarization of a promissory note is not legally required. But if you want to (and the other party agrees), you can have the note notarized.

Can a promissory note be handwritten?

Yes, a promissory note can be handwritten. However, it is not advised because a handwritten note makes it simpler to add or change information.

Who signs a promissory note?

Typically, only the borrower signs a promissory note. The only signature that is legally required is theirs, but the lender may also sign the note if they so choose.

Is a promissory note a contract?

Yes. A promissory note is a contract and is legally enforceable.

Legal Templates only uses credible sources, such as peer-reviewed studies, to substantiate the information in our articles. To learn more about how we maintain our content’s accuracy, dependability, and trustworthiness, read our editorial guidelines.

Related Personal Finance Documents

Free Promissory Note Template

Create Your Promissory Note in Minutes!

FAQ

How do you write a promissory note for a personal loan?

- Date.

- Name of the lender and borrower.

- Loan amount.

- Whether the loan is secured or unsecured. If it’s secured with collateral: What is the collateral? .

- Payment amount and frequency.

- Payment due date.

- Whether the loan has a cosigner, and if so, who.

What are some examples of promissory note?

- PROMISSORY NOTE.

- The undersigned (the “Maker”) hereby promises to pay the principal amount of $ ____________ in accordance with the terms and conditions stated here to the order of ____________________ (LENDER NAME) (the “Payee”) in exchange for the value received.

- PAYMENT OF PRINCIPAL.

Can I write my own promissory note?

You can make a promissory note online or with a template. But before getting started, you’ll need to gather some data and decide how the loan will be structured. You will initially require the borrower’s and the lender’s names and addresses (also known as the “payee”).

How do you write a perfect promissory note?

In order to satisfy the UCC’s requirements for perfection by possession, a promissory note security interest may be perfected in one of two ways: either the borrower delivers the note to the lender along with a blank, undated note power; or filing a properly completed UCC-1 in the appropriate filing office.