Buying your first home is an exciting milestone! But it also involves making some big decisions, like choosing the right mortgage loan Two popular options for first-time homebuyers are Rural Development loans and FHA loans. In this article, we’ll compare these government-backed loans to help you decide which is a better fit.

What Are Rural Development and FHA Loans?

Both Rural Development loans (also called USDA loans) and FHA loans are insured by government agencies This makes them more accessible to buyers with lower incomes, smaller down payments, or weaker credit

Rural Development loans are backed by the U.S. Department of Agriculture. As the name implies, they are for buying homes in eligible rural areas. The USDA sets maximum income limits based on the location and family size.

FHA loans are insured by the Federal Housing Administration. They have more flexible income and credit standards than conventional mortgages. FHA loans can be used to buy homes anywhere, not just rural locations.

While the government insures them, you still get Rural Development or FHA loans through private lenders like banks and credit unions. The lender collects an upfront mortgage insurance premium and ongoing fees to cover the government backing.

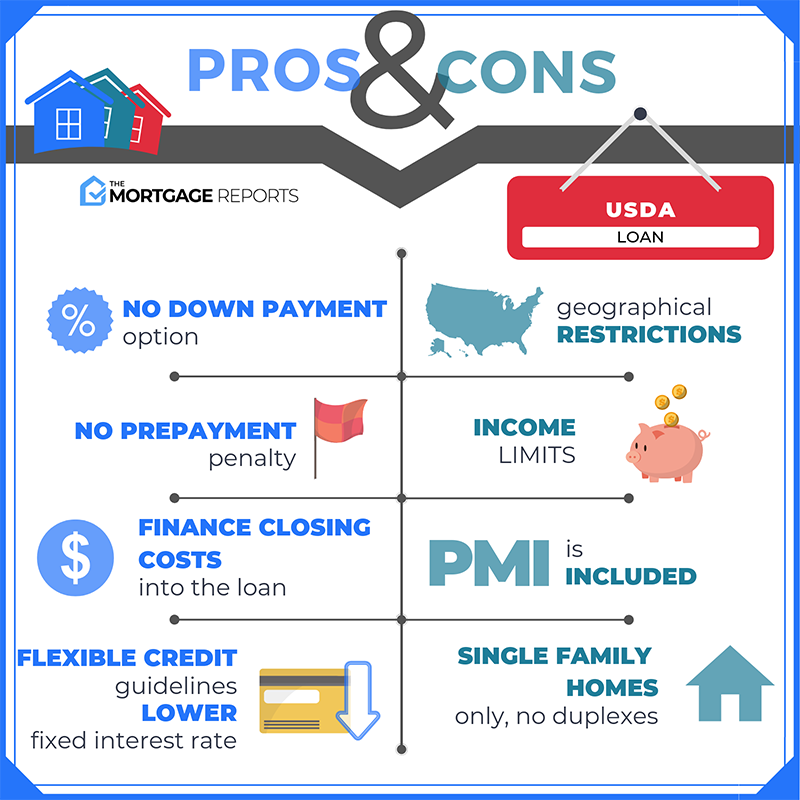

Rural Development Loan Pros

Rural Development loans offer some nice perks, especially for cash-strapped first-time homebuyers.

No Down Payment Required

The biggest benefit of Rural Development loans is that no down payment is required. You can finance 100% of the purchase price plus closing costs. With an FHA loan, you need at least 3.5% down.

Being able to buy with no money down makes homeownership more feasible for those without much cash saved. It also means you don’t have to drain your emergency fund.

Low Mortgage Insurance

Rural Development loans charge an upfront guarantee fee of 1% of the loan amount and an annual fee of 0.35%. On a $200,000 loan, you would pay a $2,000 guarantee fee at closing and $700 annually for mortgage insurance.

On an FHA loan with 3.5% down, you’d pay an upfront mortgage insurance premium of 1.75% of the loan amount ($3,500 on a $200,000 loan), plus 0.45% to 1.05% annually. So Rural Development loans cost less in both upfront and annual mortgage insurance.

Potentially Lower Rates

Since they are government-backed, Rural Development loans can offer better interest rates than you may find with conventional loans, especially if you have lower credit scores or income. They don’t guarantee the lowest rates, but they provide rate flexibility.

Buy in Rural Areas

Rural Development loans are one of the few 100% financing options available for rural home purchases. Their purpose is to encourage homeownership and community growth in small towns and remote areas. If you want acreage or to live far from urban centers, a Rural Development loan makes that possible.

FHA Loan Pros

FHA loans have advantages of their own for first-time homebuyers.

More Flexible Income and Credit

The FHA doesn’t set maximum income limits like the Rural Development program does. As long as you can pay the mortgage, insurance, and other debts, your income can exceed the median in your area.

FHA loans also allow lower credit scores, starting at just 580. So they are accessible to more buyers who don’t have pristine credit or high incomes.

Buy Anywhere

You can use an FHA loan to buy a home anywhere in the U.S. — urban, suburban, or rural locations all qualify. Rural Development loans are limited to designated rural areas only. So FHA loans provide more options if you need to live in a metro area or town for work or don’t want to be too remote.

Lower Monthly Costs

Because FHA loans require a small down payment, your monthly mortgage insurance costs will be lower than with a Rural Development loan. On a $200,000 loan, FHA mortgage insurance would add $75 to $175 per month versus $700 annually for a Rural Development loan.

If you can swing the down payment, an FHA loan saves on monthly housing expenses. This can make it easier to afford your home long-term.

Sell Sooner

FHA loans let you cancel mortgage insurance once you build enough equity, usually after 11 years. With a Rural Development loan, you pay the annual fee for the entire 30-year loan term.

So if you may sell or refinance within 5-10 years, an FHA loan could cost less overall and allow you to drop mortgage insurance early.

Rural Development Loan Cons

While they have benefits, Rural Development loans also come with limitations and drawbacks to consider.

Strict Income and Purchase Price Limits

Household income must be below 115% of the median income for your area to qualify for a Rural Development loan. The maximum home purchase price and loan amount are also capped based on local home values.

These restrictions aim to assist true low- to moderate-income buyers. But they rule out Rural Development loans for those above the limits, even if you need assistance. FHA loans are an option regardless of income.

Rural Locations Only

Rural Development loans can only be used to buy homes in approved rural areas. Suburbs near major cities and most towns over 10,000 population are ineligible.

If your job or lifestyle requires living in a more populated area, you’ll need to look at FHA or other loan programs. Rural Development financing won’t be an option.

Higher Upfront Costs

While monthly mortgage insurance is low, Rural Development loans charge a 1% upfront guarantee fee. On a $200,000 loan, that’s $2,000 at closing. FHA loans charge a 1.75% upfront mortgage insurance premium, costing $3,500 in upfront costs.

If you’re able to make a small down payment on an FHA loan, the guarantee fee makes Rural Development loans more expensive at closing.

Must Be Owner-Occupied

Rural Development loans require you to use the home as your primary residence. So you cannot use this financing for a vacation home or rental property. FHA loans allow second homes and investment properties with higher down payments.

FHA Loan Cons

FHA loans also aren’t perfect. Here are a few potential drawbacks:

Higher Monthly Mortgage Insurance

As mentioned above, FHA loans typically cost more per month in mortgage insurance versus the annual fee on a Rural Development loan. If you take the full loan term to pay off the mortgage, a Rural Development loan usually costs less overall.

Must Have 3.5% Down Payment

While it’s not a huge amount, coming up with even a 3.5% down payment can be a hurdle for first-time buyers on tight budgets. The zero down payment feature of Rural Development loans makes them more accessible for those without cash on hand.

Lower Max Loan Amounts

Currently FHA loans are capped at $350,000 to $650,000 depending on the area. Rural Development loans don’t have set limits.

In lower-cost markets, Rural Development loans may allow you to borrow more to purchase a nicer home than FHA financing will permit. The max loan amounts on FHA loans may constrain your options.

Not Ideal for Low Credit Scores

While FHA loans go down to 580 credit scores, lenders often require scores of at least 620 to 660 for the best rates and terms. If your score is below 600, a Rural Development loan with manual underwriting may be a better fit than an FHA loan.

Who Should Consider Rural Development Loans?

Given the pros and cons, here are some signs a Rural Development loan may be right for you:

- You want to buy a home in a rural location

- You have a low to moderate income but are above FHA limits

- You have no down payment funds available

- You want low monthly mortgage insurance costs

- You plan to keep the home long term and can pay the annual fee

Rural Development loans are a great option to open up homeownership opportunities in small towns and rural communities for creditworthy buyers who may not qualify otherwise.

Who Should Consider FHA Loans?

FHA loans tend to work better for these buyers:

- You need to buy in suburban or urban areas

- You want the option of selling or refinancing sooner

- Your income exceeds Rural Development limits

- You can manage a small 3.5% down payment

- You have lower credit scores under 620

FHA loans offer flexibility for those who don’t quite fit the narrow income brackets and rural locations of Rural Development loans. Just be aware of the higher monthly costs and loan limits.

Talk to a Lender About Your Options

As you can see, Rural Development and FHA loans each have pros and cons. There’s no one-size-fits-all best loan.

The right choice depends on your specific needs, finances, and home preferences. I recommend talking with a lender early in the home buying process. They can guide you through

USDA vs FHA: Eligibility

A large part of the decision between USDA vs. FHA loans will depend on which type of mortgage you qualify for. Here’s a brief overview of how USDA and FHA eligibility requirements compare.

| Criteria | FHA Loans | USDA Loans |

| Loan Requirements | Minimum credit score of 580 for 3.5% down payment Steady employment history Property must be primary residence | Must meet income eligibility Property must be in a USDA eligible area Property must be primary residence |

| Loan Limits | Vary by county, but typically up to $ for single-family homes in most areas | No set loan limit, but the home must be modest in size for the area, and cannot have luxury features |

| Income Limits | None | Usually 115% of area median income (AMI) |

| Appraisal | Required Must meet HUDs minimum property standards | Required Must meet USDAs property and location requirements |

| Down Payment | Minimum of 3.5% with a credit score of 580 or higher 10% for credit scores between 500-579 | No down payment required |

| Mortgage Insurance | Upfront mortgage insurance premium (1.75% of the loan amount) Annual mortgage insurance premium (0.45% to 1.05% of the loan amount, paid monthly) | Upfront guarantee fee (1% of the loan amount) Annual fee (0.35% of the loan amount, paid monthly) |

| Interest Rates | Vary by lender, credit score, down payment, and other factors Typically lower for borrowers with good credit | Set by the lender, but can be as low as current market rates due to government backing |

| Closing Costs | Vary by lender, but can include appraisal fees, credit report fees, lenders origination fees, etc. Can be covered by seller or lender | Can include appraisal fees, credit report fees, lenders origination fees, etc. Can be rolled into the loan amount or paid by the seller |

The FHA program offers 30-year and 15-year fixed-rate mortgages, along with adjustable-rate mortgages (ARMs). The USDA offers only a 30-year fixed-rate loan.

In addition, both programs require you to buy a primary residence, meaning you can’t use them for a vacation home or investment property. However, FHA loans can finance multi-family homes with 2, 3, or 4 units, whereas a USDA loan can be used only for a single-family home.

Pros and cons of USDA loans

The USDA loan has quickly risen in popularity with first-time and lower-income borrowers thanks to its zero-down allowance and low rates. But not everyone will qualify. Here’s what you should know.

Are USDA or FHA Loans Better?

FAQ

Is FHA or USDA better?

What credit score do you need for a FHA and USDA loan?

What is better than a FHA loan?

What is a USDA Rural Development Loan?

USDA loans are an attractive mortgage option for low- to medium-income homebuyers who live in rural areas and may not qualify for a conventional, FHA or VA loan. Consider a USDA rural development loan if you’re interested in buying, refinancing or renovating a home in a rural community that will be your primary residence.

What is the difference between USDA and FHA loans?

Compared to USDA loans, FHA loans aren’t restricted to rural areas. And, like USDA loans, FHA loan programs require mortgage insurance, but rates are much higher—1.75% at closing and 0.45% to 1.05% per year.

Can I get a USDA loan if I live in a rural area?

USDA loans, also known as rural development loans, are mortgages designed to stimulate homeownership and the economies of rural areas across the U.S. You can only take advantage of a USDA loan if you agree to purchase a home in a qualified rural area. The location must meet certain guidelines and meet state property eligibility requirements.

Why are USDA and FHA loans so popular?

Home buyers with low or moderate incomes may gravitate toward mortgages with more lenient borrowing requirements, especially when it comes to down payments and mortgage insurance. This is why USDA and FHA loans can be so appealing to borrowers. How do the two types of mortgage loans differ, though?

Should I get a USDA or FHA loan?

USDA loans allow no down payment and have cheap mortgage insurance, but you have to buy in a “rural” area and meet income limits. FHA loans are more flexible about income, credit, and location, but they can have higher costs. Check your home loan options. Start here Luckily, there’s an easy way to choose.

Can you buy a home in a rural area?

These government-backed loans can be used to purchase, build, repair or refinance a home in a rural area. The USDA provides several Rural Development Single-Family Housing Programs for homeowners, homebuyers and organizations. These government-backed loans, grants and loan guarantees make homeownership possible for many individuals and families.