Whether youre an avid fisher, enjoy water skiing or want to relax on the open water with your family and friends, youre glad that you bought a boat. One thing you might not be so thrilled about, though, is the loan you took out to afford to purchase the boat. Depending on your circumstances at the time of purchase, your boat loan might have a high interest rate. Alternatively, the monthly payments might not work with your current budget.

If your current loan isnt working for you, you can refinance a boat loan to get terms that are a better fit for your current financial situation. Learn more about how a new or used boat refinance works and the numerous benefits of doing it.

Owning a boat can be an incredibly rewarding experience With the freedom to explore open waters and create lasting memories, boat ownership brings a lot of joy. But boats also come with hefty price tags Financing your boat through a boat loan is often necessary to make owning one possible.

Over time though, your financial situation may change in a way that makes refinancing your boat loan a smart money move. Refinancing can help lower your interest rate reduce monthly payments or alter the loan term.

Navigating how and when to refinance a boat loan can get confusing though This comprehensive guide breaks down everything you need to know about the boat loan refinancing process

What is Refinancing a Boat Loan?

Refinancing a boat loan means taking out a new loan to pay off your existing boat loan. You are replacing your current boat loan with a new one under hopefully better terms.

The steps involve:

- Applying for a new boat loan with a different lender

- Using the proceeds from the new loan to pay off the old loan

- Continuing to make payments on the new loan with hopefully better rates/terms

You still keep the same boat as collateral. Only the financing terms change through refinancing.

Why Refinance a Boat Loan?

There are a few key reasons refinancing an existing boat loan could be beneficial:

Lower Interest Rate – Interest rates fluctuate over time. Refinancing at a lower rate decreases your payments and overall savings.

Shorten Loan Term – Refinancing resets the payoff timeline. You may want to shorten the term to build equity faster.

Lower Monthly Payments – Even if rate stays the same, you can lower monthly costs by extending the loan term.

Tap Equity – If the boat has increased in value and you’ve paid down principal, you can access that equity through cash-out refinancing.

Change Lenders – You may want to refinance with a new lender if your current one offers poor rates or customer service.

When to Refinance a Boat Loan

Timing is an important factor when refinancing a boat loan. Here are some key times refinancing tends to make the most financial sense:

-

Interest Rates Drop – Monitor rate trends. When rates decrease by 1% or more below your current rate, refinancing can mean big savings.

-

Improved Credit Score – A jump of at least 30 points in your credit score might qualify you for a lower rate through refinancing.

-

Halfway Point – Consider refinancing around the halfway point of your loan term when you’ve built up equity.

-

Life Changes – Major life events impacting income or expenses may warrant refinancing to lower payments.

-

Loan Incentives – Lenders sometimes offer refinancing incentives you may want to take advantage of.

-

Poor Service – Bad customer service or inflexibility from current lender may motivate you to refinance.

How to Refinance a Boat Loan

Ready to move forward? Here are the key steps involved:

1. Review Current Loan

Start by reviewing your existing boat loan terms including:

- Interest rate, loan balance, and monthly payment amount

- Loan type (fixed or adjustable) and length of remaining term

- Prepayment penalties or other loan restrictions

This gives you a baseline for potential savings.

2. Check Qualifications

Before applying to refinance, confirm you meet basic requirements:

- At least 20-30% equity in the boat

- Improved credit score since taking original loan

- Reduced debt-to-income ratio if possible

This helps ensure you qualify for the best new rate.

3. Research Lenders

Shop around with multiple lenders to compare refinancing options:

- Banks, credit unions, online lenders

- Get rate quotes and run loan estimates

- Ask about rates, fees, terms, and closing timeline

Cast a wide net to find the most competitive boat loan refinance.

4. Submit Refinance Application

After selecting the best lender option, complete their refinancing loan application including:

- Financial and employment documentation

- Boat ownership and insurance records

- Existing loan details and payoff information

This kicks off the official underwriting and approval process.

5. Close on New Loan

Once approved, you can close on the new loan and the lender will pay off your old boat loan balance. Make sure to get wire confirmation to avoid any gaps in payment.

Then you are all set! The boat is now financed through the new, ideally better loan terms.

How Much Does it Cost to Refinance a Boat Loan?

Closing costs are incurred with refinancing just like when you originated the loan. Typical refinancing fees include:

- Application fee – $50-500

- Points – 0-5% of loan amount

- Title search charge – $25-250

- Recording fees – $10-100

- Appraisal fee – $300-500

You’ll also pay interest on the new loan from the closing date. Shop lenders to minimize total costs. Often you can roll closing costs into the new loan amount as well.

Aim for breakeven in 18 months or less where savings exceed closing costs.

Should You Refinance? Key Factors to Consider

Refinancing a boat loan can yield significant interest savings, but also involves fees and paperwork. To decide if it makes sense for your situation, weigh the following:

Credit Score Change

If your credit score has increased at least 30 points since getting your original boat loan, you’re a prime candidate for refinancing thanks to better rate qualification.

Interest Rate Reduction

To make refinancing worth it, look for a new rate around 1-2% lower. This creates enough savings to offset closings costs within 12-24 months.

Original Loan Term

The longer the term remaining on your current boat loan, the greater potential savings from refinancing to a lower rate.

Lower Monthly Payments

Even if your rate doesn’t change, you may want to refinance to a longer loan term and reduced monthly payments to improve cash flow.

Prepayment Penalties

If your current loan includes early repayment fees, make sure savings exceed the penalty amount.

Closing & Processing Costs

Aim for total refinancing fees under 2% of the loan amount so they breakeven quicker through lower payments.

By modeling potential savings and weighing the above factors against costs, you can make an informed decision about refinancing your boat loan.

Boat Loan Refinancing Process Step-By-Step

Follow this more detailed walkthrough of the full boat loan refinancing process from start to finish:

1. Gather Key Loan Documents

Locate your current boat loan paperwork, including:

- Original signed promissory note

- Truth in Lending Disclosure with rate and term details

- Payment history showing principal paid down

This provides essential details for researching new options.

2. Check Your Credit Report

Order a copy of your credit report from Experian, Equifax or Transunion. Review for any errors that could impact qualification and start disputing immediately.

3. Get Current Loan Payoff Quote

Contact your current boat loan lender and request a loan payoff quote. This shows your remaining principal balance plus any prepayment penalties.

4. Shop Refinancing Lenders

With your loan docs and credit report in hand, apply with multiple lenders for rate quotes on refinancing options. Compare terms and total costs.

5. Select Best Lender

Choose the lender offering the lowest rate/fees and terms that align with your goals. Confirm required paperwork and closing timeline.

6. Formally Apply for Loan

Complete full loan application providing financial statements, employment verification, insurance documentation and all required paperwork.

7. Get Boat Appraisal if Needed

Depending on equity, lender may require a current appraisal to confirm boat value supports the new loan amount. Expect fees around $300-500.

8. Get Loan Approval

After underwriting, you will receive a loan decision from the lender. Make sure terms match your application.

9. Schedule Loan Closing

Once approved, you can schedule closing where you sign final loan documents. Closing costs are due at this time via wire transfer or check.

10. Finalize Payoff of Old Loan

Lender will wire payoff funds to your old boat loan, releasing its lien. Confirm your title shows the new lender’s lien for the refinanced loan.

And that’s a wrap! With these steps completed, you can start making payments on the refinanced boat loan.

Alternatives to Refinancing a Boat Loan

While refinancing is often the best option when looking to modify a boat loan, here are a couple other alternatives to consider:

What Is a Boat Refinance?

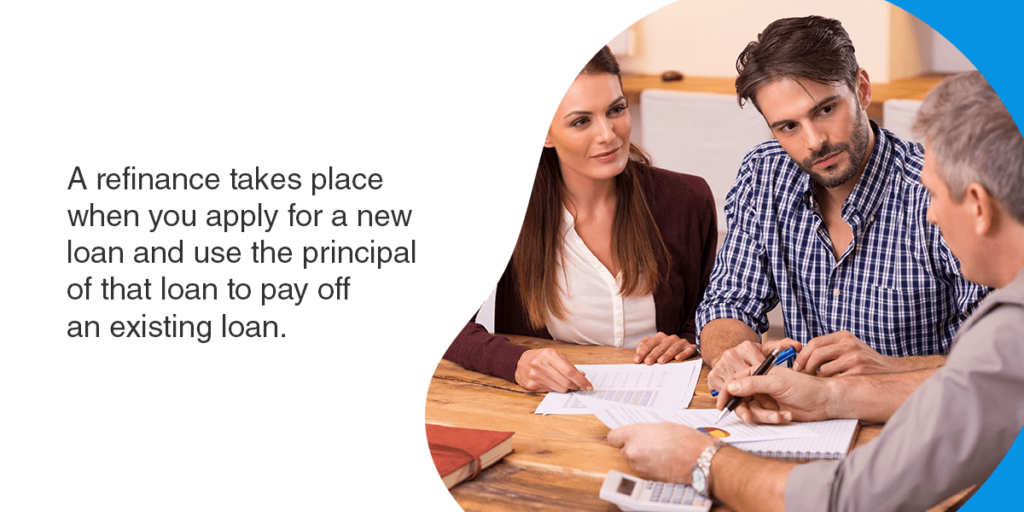

A refinance takes place when you apply for a new loan and use the principal of that loan to pay off an existing loan. You can refinance a wide range of loans. For example, people who own homes can refinance their mortgages to take advantage of reduced interest rates or to cash out some of the equity in their property. People who have car loans might refinance to get a lower interest rate or to change the length or term of the loan.

If youve been through the process of getting a loan for your boat, youre already somewhat familiar with the process of refinancing the loan. Youll need to go through the loan application all over again, providing information like proof of income and your credit history. The lender will make a decision about the interest rate to offer you and then you can decide whether you want to go through with the refinance or not.

A few types of refinance loans are available. The one that is right for you depends on your goals for refinancing and what you hope to get from the loan.

Boat Refinance Rate and Term

With a rate and term refinance, you change the interest rate on the loan or the term of the loan, or in some cases, on both. For example, say your current loan has a remaining balance of $75,000 and an interest rate of 10%. The original term was 10 years. When you refinance the loan, you borrow $75,000 to pay off the balance on the first loan. The new loan has an interest rate of 8% and a term of eight years.

Some of the reasons you might choose a rate and term refinance include:

- You want to pay less interest: If rates have dropped or your credit has improved since you got the first loan, a rate and term refinance allows you to take advantage of lower rates.

- You want more or less time to pay off the loan: Your financial priorities might have shifted since you first took out the loan. You might now want to focus on saving for retirement or paying down your mortgage. Refinancing lets you change the term of the loan, allowing you to spread out your payments. Conversely, you can shrink the repayment period if you want to be free of your loan faster.

- You want a different monthly payment: Changing the rate or term of your loan, or both, means your monthly payment can increase, reducing the time it takes to pay off the loan. Alternatively, it can decrease, meaning you can focus on other financial commitments.

Boat Loans 101: Should You Finance A Boat?

FAQ

Is it possible to refinance a boat loan?

What is a good interest rate for a boat loan?

|

Best for…

|

Starting APR

|

Loan amounts

|

|

Low APRs

|

6.74%

|

$10,000 – $9,900,000

|

|

No fees

|

6.99% (with autopay)

|

$5,000 to $100,000

|

|

Same-day credit approval

|

6.99%

|

$10,000 – $4,000,000

|

|

Large boat loans

|

7.49%

|

Up to $25,000,000

|

Are boat interest rates going down?

What is the average term of a boat loan?

How do I refinance a boat?

Check your rates with as many boat refinance lenders as you can. The more you consider, the better your odds of finding a better boat loan. Apply for the new boat loan. When you find a lender, complete your application for a new boat loan. Keep an eye on the money transfer.

What is the average interest rate for a boat loan?

The average interest rate for a boat loan varies depending on the lender, the size of the loan, your credit score and income, and whether the loan is secured by the boat or unsecured.According to **USA

When should I refinance my Boat loan?

There’s no one size fits all answer to when you should refinance your boat loan. You may be happy with your current boat loan but if you feel like you could benefit from a lower monthly payment, a shorter or longer term, or a lower interest rate, then consider refinancing your current boat loan.

What is a boat loan refinance?

A boat loan refinance, also called a boat refi, may be offered by your current lender or a new one, and serves to pay off and replace your existing loan. Rather than continuing to make scheduled payments to your original lender, after refinancing you will make payments to your refinance lender on your new loan.