Note from the Editor: This article’s content is solely based on the author’s opinions and suggestions. It might not have received approval from any of our network partners through reviews, commissions, or other means.

The ability to deduct the interest you pay on your mortgage from your taxable income thanks to the home mortgage interest deduction can result in significant tax savings. It’s one of the benefits of homeownership, but not everyone with a mortgage is eligible for it, and the savings may not always be substantial. We’ll go over every detail, including who is eligible and how to figure out how much you can save.

How Does LendingTree Get Paid?

Companies on this website pay LendingTree, and this pay may have an impact on where and how offers appear on this website (such as the order). Not all lenders, savings products, or loan options are offered by LendingTree in the market.

Note from the Editor: This article’s content is solely based on the author’s opinions and suggestions. It might not have received approval from any of our network partners through reviews, commissions, or other means.

The ability to deduct the interest you pay on your mortgage from your taxable income thanks to the home mortgage interest deduction can result in significant tax savings. It’s one of the benefits of homeownership, but not everyone with a mortgage is eligible for it, and the savings may not always be substantial. We’ll go over every detail, including who is eligible and how to figure out how much you can save.

What is the home mortgage interest deduction?

With the help of the home mortgage interest deduction, homeowners can reduce their total taxable income by deducting the interest they pay on a mortgage during a given tax year. The interest paid on mortgages secured by a taxpayer’s primary residence (and a second home, if applicable) for loans used to purchase, construct, or significantly improve the property is deductible from their taxes.

The deduction typically only applies to interest paid up to a predetermined maximum amount, which depends on when you took out your loan and whether you are filing jointly with a spouse.

What’s deductible: Loans and expenses that qualify

Important rules and exceptions:

Mortgages used to build or improve your primary home or a second home.

Exceptions: The loan is not deductible if it was used to repair rather than improve your home.

Home equity debt on a primary home or second home.

There are other types of interest that you can deduct from your yearly tax bill in addition to the interest component of your mortgage payment. You can also deduct:

→ Mortgage points, or prepaid interest, paid at closing

Mortgage insurance premiums, including the VA funding fee, private mortgage insurance, and insurance on FHA and USDA loans

Late payment fees that are not connected to a particular loan service

→ Prepayment penalties assessed for paying your mortgage off early

Interest received as a result of taking part in the Emergency Homeowners Loan or Hardest Hit Fund programs.

Should I deduct my mortgage interest?

The home mortgage interest deduction only applies if you are itemizing your deductions, which is important to understand because for most people, doing so doesn’t make financial sense. When filing their taxes, most homeowners will save more money by taking the standard deduction as opposed to itemizing.

Keep in mind the total amount of interest you paid and contrast it with the standard deduction applicable to your taxpayer filing status. For instance, the standard deduction amounts for single people, married couples, and unmarried heads of households in 2022 are $12,950, $25,900, and $19,400, respectively.

Imagine that the interest you paid the previous year exceeded your standard deduction. If so, itemizing all of your deductions, including the mortgage interest tax deduction, could help you save money. Consult a tax professional for additional guidance.

Things You Should Know

The Tax Cuts and Jobs Act was instituted in 2017 and virtually doubled the standard deduction for most taxpayers. Since then, the amount of Americans itemizing and utilizing the home mortgage interest deduction has plummeted. In the year immediately following the passage of the Act, the number of taxpayers who used the mortgage interest tax deduction fell by 40%.

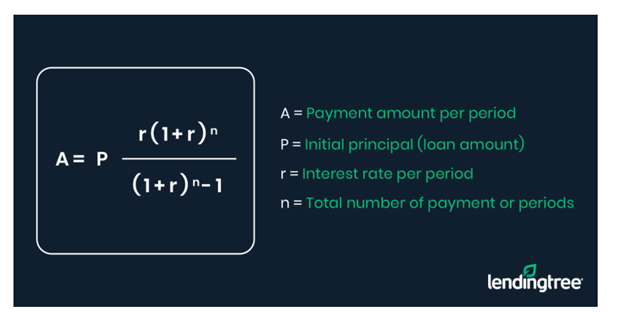

How is mortgage interest calculated?

While using a mortgage payment calculator to figure out your mortgage interest is undoubtedly the simplest option, if you prefer to do it manually, here is the formula:

The mortgage interest deduction does not work “dollar-for-dollar” like a mortgage tax credit, so you cannot reduce your tax liability by the exact amount of mortgage interest you paid. Instead, by decreasing your taxable income, you’ll indirectly lower your tax obligation. You are guided step-by-step through the calculations required to determine how much mortgage interest you can deduct in Schedule A of IRS tax form 1040.

How to claim the home mortgage interest deduction

Wait for your tax form(s) Your mortgage lender will send you a form, called Form 1098, that details the amount of mortgage interest you paid over the year. Review the amount of interest listed as paid in Box 1. If you paid less than $600 in interest, your lender isn’t required to send you this document. Otherwise, you should receive a separate 1098 for each loan you’re still paying off.

Analyze the standard deduction amount against the total amount of deductible mortgage interest and other deductions to decide whether to itemize. This will enable you to decide whether it is more advantageous to itemize your deductions or take the standard deduction. You will save money by itemizing deductions if your total amount is greater than the standard deduction for your tax filing status.

Claim your deductions If your itemized deductions as a whole exceed your standard deduction, you should probably claim the mortgage interest deduction as well as any other deductions that apply. To accomplish this, you must complete Schedule A on Form 1040 and submit it with your tax return.

The maximum is typically $750,000 for individuals and $375,000 for married couples filing separately, depending on when you secured your loan. For loans originated before Dec. The ceiling is $1 million for individuals and $500,000 for married couples filing separately as of December 16th, 2017. Loans from before Oct. 14, 1987 are not subject to a limit.

The mortgage interest deduction is available to anyone who owns a home or who is filing jointly with a spouse who does. Most home types qualify, including condos, mobile homes and houseboats.

The home mortgage interest deduction is available for second homes that you do not rent to other people. Rental property, on the other hand, doesn’t. The number of days a second home is rented out determines whether or not it qualifies as “rental property” for tax purposes. You will not be eligible for the home mortgage interest deduction if you use your second home for less than 10% of the days it was rented out or less than 14 days per year.

Yes, any points paid on a refinance are tax deductible, but there is a significant catch: you have to spread the points out over all of the payments you’ll make throughout the loan’s lifetime. Only the amount that applies to the tax year you are filing for may be written off.

Today’s Mortgage Rates APR as low as

As a homeowner, you are eligible for a variety of tax benefits, such as tax deductions that lower your annual taxable income.

When you obtain a mortgage, some of the closing costs you pay have tax advantages. Here are some examples of tax deductions and exclusions.

This tax season, by learning more about home business tax deductions and using them, you might end up with a few extra dollars in your pocket.

FAQ

Can you claim mortgage interest if married filing separately?

Mortgage interest would be claimed by the person who made the payment when filing a married, separate returns. As a result, if one of you paid from their own account alone, they can deduct all of the property taxes and mortgage interest.

Can mortgage interest be split on taxes?

Each Schedule A should list half as a deduction if each taxpayer paid half of the mortgage and real estate tax costs. A statement describing how you’re splitting the mortgage interest and real estate tax payments should be attached to both of your Schedules A.

How do deductions work when married filing separately?

Both spouses must itemize their deductions or both must take the standard deduction when filing separately. While the other spouse takes the standard deduction, one spouse cannot itemize their deductions. Even if both spouses paid for the expense, only one spouse may claim each deduction when itemizing deductions.

Who gets to deduct mortgage interest if there are two borrowers?

Even though the 1098 lists multiple names, only one person is paying the mortgage or interest, so only that person can deduct it. Multiple people are paying the mortgage/interest on the 1098, and each may deduct their share of the interest paid.