Buying your first home is an exciting milestone, but it can also be daunting especially when it comes to choosing the right mortgage. Two popular options for first-time homebuyers are FHA loans and USDA loans. But what exactly is the difference, and which one is better for you?

An Overview of FHA and USDA Loans

Both FHA and USDA loans are government-backed mortgages aimed at making homeownership more accessible.

FHA loans are insured by the Federal Housing Administration. The FHA doesn’t lend money directly, but it protects lenders against losses if borrowers default. This allows lenders to offer FHA loans with low down payments and flexible credit requirements.

Similarly, USDA loans are backed by the US Department of Agriculture. The USDA guarantees these mortgages to encourage homeownership in rural areas. USDA loans offer affordable financing and require no down payment.

While the two programs have similarities, there are some key differences when it comes to eligibility, costs, and other factors.

Comparing the Eligibility Requirements

To qualify for an FHA loan, you’ll need a credit score of at least 580 if you put down 3.5%. The minimum goes up to 620 for a 3% down payment. With FHA, you can buy a primary residence, second home, or investment property. There are no income limits.

For a USDA loan, you’ll need a 640 credit score. The home must be your primary residence in an eligible rural area. And household income must be below 115% of the median income for that location.

So FHA loans allow lower credit scores overall. But USDA has tighter requirements when it comes to your income and the home’s location.

Down Payments and Mortgage Insurance

One of the biggest perks of USDA loans is that they require zero down payment. You can finance 100% of the purchase price.

With an FHA loan, you’ll need at least 3.5% down if your credit score is 580-619. And you’ll pay an upfront mortgage insurance premium of 1.75% of the loan amount.

Both loans charge ongoing mortgage insurance:

- FHA – 0.45% to 1.05% of the loan amount per year

- USDA – 0.35% of the remaining balance per year

You’ll pay this for the life of the loan in most cases.

Interest Rates and Loan Limits

Government backing allows FHA and USDA lenders to offer competitive interest rates. USDA has no set loan limits. FHA loan limits vary by county but can go up to $970,800 in high-cost areas.

For both loans, you’ll work with private lenders approved to offer these programs. Shop around for the best deals. Interest rates and fees will vary by lender.

The Home Buying Process

With both FHA and USDA mortgages, you’ll go through the usual process of getting preapproved, shopping for a home, making an offer, and closing on the purchase.

FHA loans may have a slightly quicker underwriting process. USDA loans require an extra underwriting step by the agency itself, which can add a week or two.

Either way, go in knowing these government-backed loans are designed to be borrower-friendly. Lenders will work with you if you have limited funds or credit challenges.

Pros and Cons of FHA vs. USDA

| FHA | USDA | |

|---|---|---|

| Pros | – Lower credit score requirements <br>- Available nationwide <br>- Lower mortgage insurance costs | – No down payment required <br>- Very low mortgage insurance <br>- Helps buyers in rural areas |

| Cons | – Requires 3.5% down <br>- Mortgage insurance lasts until 78% LTV reached | – Home must be in eligible rural area <br>- Tighter income limits <br>- Slower underwriting process |

As you can see, each program has unique advantages. Your individual situation will determine whether FHA or USDA is a better fit.

How to Decide Between FHA and USDA

If your choice isn’t obvious, ask yourself:

- Is my income below the limit for USDA loans in my area?

- Is the home I want in an eligible rural location?

- How much can I afford to put down upfront?

- What are my plans for the future?

You should also get rate quotes from lenders for both loan types. Comparing the costs and fees will help guide your decision.

And don’t forget to account for total monthly payments. The mortgage amount, interest rate, mortgage insurance, and other costs all factor in.

Focus on Finding the Right Home for You

As a first-time buyer, having financing options like FHA and USDA loans is invaluable. You can move forward with confidence knowing the mortgage process will be smooth.

Keep focused on finding the perfect home for your needs and budget. With the right loan choice, you’ll be well on your way to an exciting new chapter in homeownership.

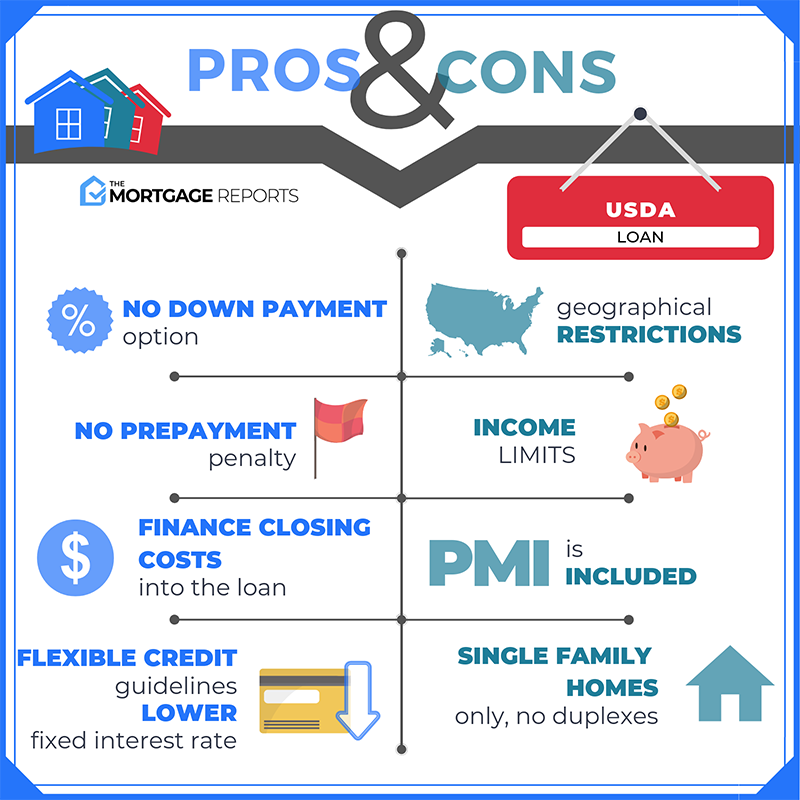

Pros and cons of USDA loans

The USDA loan has quickly risen in popularity with first-time and lower-income borrowers thanks to its zero-down allowance and low rates. But not everyone will qualify. Here’s what you should know.

Differences between USDA and FHA loans

When comparing USDA vs FHA loans, both government-backed, differences emerge in terms of application, underwriting, appraisal, loan amounts, mortgage insurance, interest rates, and more. Prospective borrowers should carefully analyze the details of USDA vs FHA loans to make an informed decision based on their specific financial circumstances and homeownership aspirations.

Are USDA or FHA Loans Better?

FAQ

Which is better FHA or USDA?

Are USDA loan payments cheaper?

What is the advantage of a USDA loan?

What are the debt to income requirements for a USDA loan?