Reviewed Editorial Note: We earn a commission from partner links on Forbes Advisor. Commissions do not affect our editors opinions or evaluations.

Building a house from scratch can be a great opportunity to get the home you’ve always wanted. But construction costs can add up quickly and timelines can be unpredictable. Luckily, a variety of construction loans provide the upfront cash needed to pay for the land, materials and labor to build a new house.

Construction loans allow future homeowners to finance the building of a new house from the ground up. But how long do borrowers have to complete construction and repay these types of loans?

In this comprehensive guide, we’ll explain everything you need to know about construction loan terms, including:

- What is a construction loan?

- How do construction loans work?

- Average construction loan terms

- Factors that determine repayment periods

- Tips for securing a longer repayment term

- What happens when the loan term ends

- Alternatives to short-term construction loans

What Is a Construction Loan?

A construction loan is a short-term financing option that provides funds to cover the costs of building a new home The loan amount is based on the total projected costs to build the home

Construction loans can be used to pay for:

- Purchasing land

- Paying contractors

- Buying materials

- Covering labor costs

- Paying for permits and fees

- Financing contingency reserves for unexpected overages

With a construction loan, funds are issued to the borrower in installments as certain stages of the building process are completed. This is different from a traditional mortgage, where you receive the full loan amount upfront.

How Do Construction Loans Work?

Construction loans provide access to financing in stages based on the progress of construction. Here’s a breakdown of the process:

-

You apply and get approved for the construction loan before beginning your project. This pre-approval is based on detailed plans, timelines, budgets, etc.

-

At closing, you’ll receive the first disbursement of funds to purchase the land, pay contractor deposits, etc.

-

As you complete certain phases of construction, your lender will schedule inspections.

-

After inspections, the lender releases additional funds to cover completed work and the next stages.

-

This process repeats until the home is built. Many construction loans then convert into permanent mortgages.

-

If yours doesn’t convert, you must get a new loan to pay off the construction loan balance.

What Is the Average Construction Loan Term?

Most construction loans have terms lasting between 9 and 18 months. The most common term length is 12 months.

This gives borrowers one year to complete construction and either convert the loan to a mortgage or secure a new loan for the balance.

Some lenders offer construction loan terms up to 24 months. Longer terms of 18-24 months give borrowers more flexibility in case of delays or other issues during the building process.

What Factors Determine the Loan Term?

Construction lenders offer terms ranging from 6 months to 24 months. The length of your repayment period depends on several factors, including:

Type of Construction

What you’re building plays a role in determining the term length needed. For example:

-

Single family homes – These are the most common projects financed with construction loans. The typical home can be built within 12 months.

-

Multi-unit properties – Projects like condos, townhomes, and apartment buildings often require longer 18-24 month terms since they’re more complex.

-

Custom/unique homes – Luxury homes with custom designs and features may also need longer terms, especially if employing rare construction materials or methods.

Experience of the Builder

Your builder’s skills and track record will influence the estimated construction timeline. An experienced general contractor that has successfully built similar projects is more likely to finish on schedule.

Some lenders even require demonstrated builder experience before approving loans. Novices and DIY builders often run into issues that cause delays.

Total Project Cost

The total loan amount and overall budget can factor into the term length. Larger projects typically require longer build times and loan terms.

Of course small homes can run into delays too. But there’s less risk for lenders with lower balance loans, so they may allow faster timelines.

Geographic Location

Weather conditions and other location factors may determine how quickly construction can be completed.

For example, projects in cold climates may need longer terms to account for winter months when building may not be feasible. Sites prone to natural disasters may also need flexible loan terms.

Tips for Getting a Longer Construction Loan Term

If your project requires more than 12 months to complete, here are some tips to improve your chances of getting a longer repayment term:

-

Provide a detailed construction timeline – Work with your builder to create a realistic, month-by-month timeline. Submit this to show your lender why you need a longer term.

-

Get multiple builder bids – Seek bids from several respected general contractors. Submit these to illustrate experienced builders also estimate a longer timeline.

-

Offer a larger down payment – Lenders are more comfortable lending for longer periods when borrowers have more skin in the game. Offer to put down 25-30% if possible.

-

Have contingency reserves – Set aside 10-20% of the loan amount to cover unexpected delays and overages that may arise. This gives you a buffer if the project takes longer than planned.

-

Improve your credit score – Lenders offer better terms to lower-risk borrowers. Boost your score before applying for the best construction loan financing.

-

Provide collateral – Putting up other property, like your current home, as additional collateral can help secure a longer repayment term.

-

Comparison shop – Shop around with multiple lenders to find the best construction loan term for your unique situation.

What Happens When the Loan Term Ends?

As your construction loan repayment date approaches, you have two options:

1. Convert to a Mortgage

Many construction loans can convert to permanent mortgages once building is complete. You’ll then be able to repay the balance over 15-30 years.

Conversion to a mortgage often happens automatically. But some lenders require you to submit a separate application and go through approval for the mortgage.

Rates and terms for the permanent financing are set when you first get approved for the construction loan. So you’ll know what to expect well in advance.

2. Pay Off the Balance

If your construction loan doesn’t convert to a mortgage, you’ll need to secure a new loan to pay off the construction loan balance at the end of the term.

This may involve applying for a traditional mortgage, home equity loan, or other financing option. You’ll likely have to pay closing costs and fees again for the new loan.

If you don’t repay the balance by the loan maturity date, the lender can foreclose. Make sure you start on alternative financing well before the term ends.

Alternatives to Short-Term Construction Loans

If you need more time to finish your project, here are a few alternatives to short-term construction loans:

-

Renovation loans – These mortgages cover purchase and renovation costs for fixer-uppers. Terms are longer since funds are issued upfront.

-

Secured lines of credit – HELOCs and home equity loans offer revolving credit you can tap as needed to self-finance construction over time.

-

Owner-builder loan – This financing allows DIY builders to complete construction in stages by directly receiving disbursements. Terms are usually longer.

-

Two-close construction loans – These provide an initial 12-month loan, which you can extend for another 6-12 months once building is underway.

-

Three-close construction loans – Here the loan converts to a 24-month term after the first year, giving you up to three years total.

-

Interest-only construction loans – Only pay interest during the building phase, then convert to a mortgage to repay the principal over 15-30 years.

The Bottom Line

Most construction loans have repayment terms lasting between 9 and 18 months. The typical construction loan term is 12 months. Extensions up to 24 months may be possible based on the scope and complexity of your building project.

Carefully evaluate whether you can realistically complete construction within a standard 12 month term. If you think you’ll need longer, discuss options with lenders. With proper planning, it’s possible to secure construction financing that aligns with your project’s timeline.

Pros and Cons of a Construction Loan

Construction loans are a considerable investment of time and money. Before applying for a construction loan, consider these benefits and drawbacks.

- The construction loan amount is based on the project and/or the future value of the property.

- The short repayment term for the loan means you only have to make interest payments during the construction period.

- It’s a good financing option for current homeowners who want to build a new home but don’t have enough equity for a home equity loan or line of credit.

- The loan amount is set in advance, giving the borrower little flexibility in the event of unexpected costs.

- The entire balance of the loan is due at the end of the construction process. If the construction loan doesn’t automatically convert into a permanent mortgage after construction, you’ll have to get a new loan to pay what you owe, which means paying two sets of closing costs and fees.

- You’ll pay higher interest rates on a construction loan compared to other loan options.

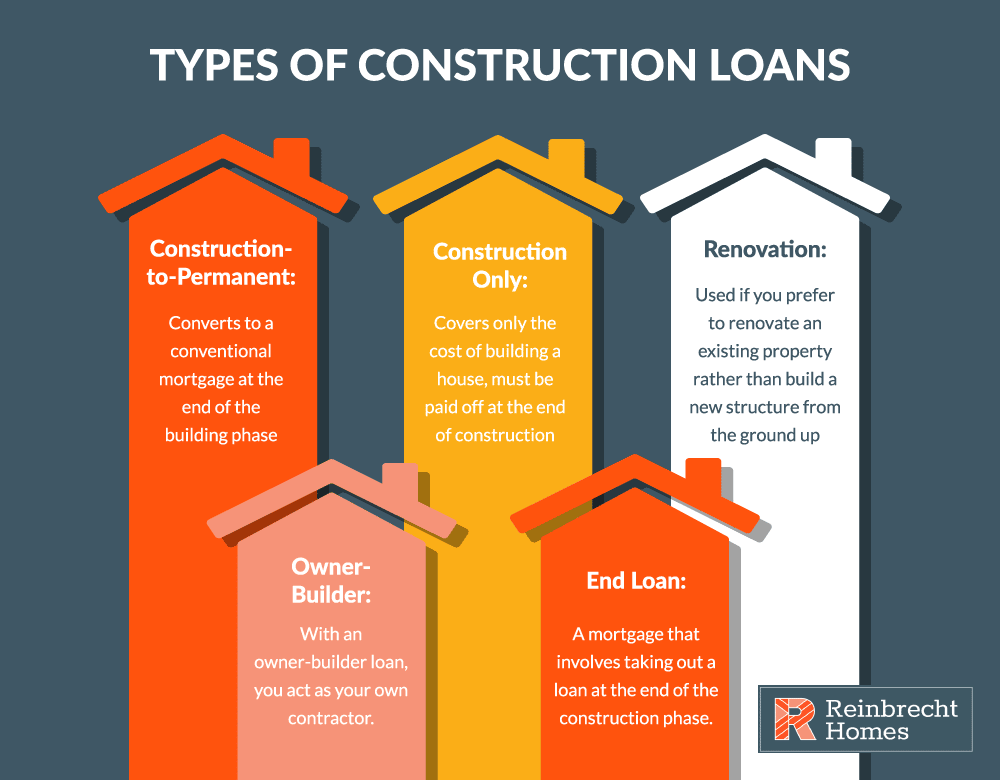

Types of Construction Loans

Building a home is not a one-size-fits-all process. To meet the varying needs of future homeowners, there are several types of construction loans available—primarily, construction-to-permanent and construction-only loans. Owner-builders and homeowners performing extensive renovations on an existing house have separate options.

| Type of loan | How it works | Best for |

|---|---|---|

| Construction-to-permanent loan | This loan finances construction of a home and then converts into a fixed-rate mortgage once the home is completed. | Homeowners who want to save on closing costs and lock in mortgage financing |

| Construction-only loan | Lender issues a short-term, adjustable-rate loan that is used to complete construction of a home. After construction is complete, the loan must be paid in full or refinanced into a mortgage. This requires two application processes and two closings. | Those who have a large amount of cash on hand or who intend to pay off the construction loan with the sale of their previous home |

| Owner-builder loan | Draws are made to the owner-builder, rather than to an approved third-party contractor. These loans are usually only available to owners who can demonstrate experience as a homebuilder—or have a contractor’s license. | Homeowners who have experience building houses and want to act as their own general contractor |

| Renovation loan | Most akin to a traditional mortgage, renovation loans cover the cost of purchasing a home and performing major renovations. Because of this, the loan amount is based on the anticipated value of the home after renovations. | Homeowners who are buying a fixer-upper intending to invest in extensive renovations |

Construction Loans: What They Are and How They Work (IN DETAIL)

FAQ

How long of period are construction loans typically issued for?

Why are construction loans hard to get?

Is a construction loan easier to get than a home loan?

What is the difference between a construction loan and a term loan?

What is a construction loan?

A construction loan is short-term financing that can be used to cover the costs associated with building a house, from start to finish. Construction loans may cover the costs of buying land, drafting plans, taking out permits and paying for labor and materials.

How much money do you need for a construction loan?

You should have enough income to cover payments on your current debts and the new construction loan. Lenders typically require a DTI ratio no higher than 45% for construction loans. Down payment of at least 20%. Borrowers typically need a down payment of at least 20% for a construction loan, but this can vary by lender.

How long do construction loans last?

Because construction loans generally are intended to cover the building process, they’re typically issued for a period of 12 to 18 months. That said, some loans automatically convert into a permanent mortgage once construction is complete. Unlike traditional mortgages, construction loans aren’t secured by a completed house.

How do construction-to-permanent loans work?

For construction-to-permanent loans, the home will serve as collateral for the mortgage once construction is complete. Getting approval for a construction loan might seem similar to the process of obtaining a mortgage, but getting approved to break ground on a brand-new home is a bit more complicated.