The FHA loan program makes homeownership more accessible for buyers who may not qualify for conventional loans. FHA loans only require a 3.5% down payment and have more lenient credit standards. If you’re considering an FHA loan in Virginia, it’s important to understand the program’s specific requirements. In this comprehensive guide, we’ll break down key eligibility criteria for FHA loans in VA.

Overview of FHA Loans

FHA loans are government-insured mortgages backed by the Federal Housing Administration. Key features include:

- Down payments as low as 3.5%

- Flexible credit requirements – minimum 580 FICO score

- Low mortgage insurance rates

- Available for primary residences

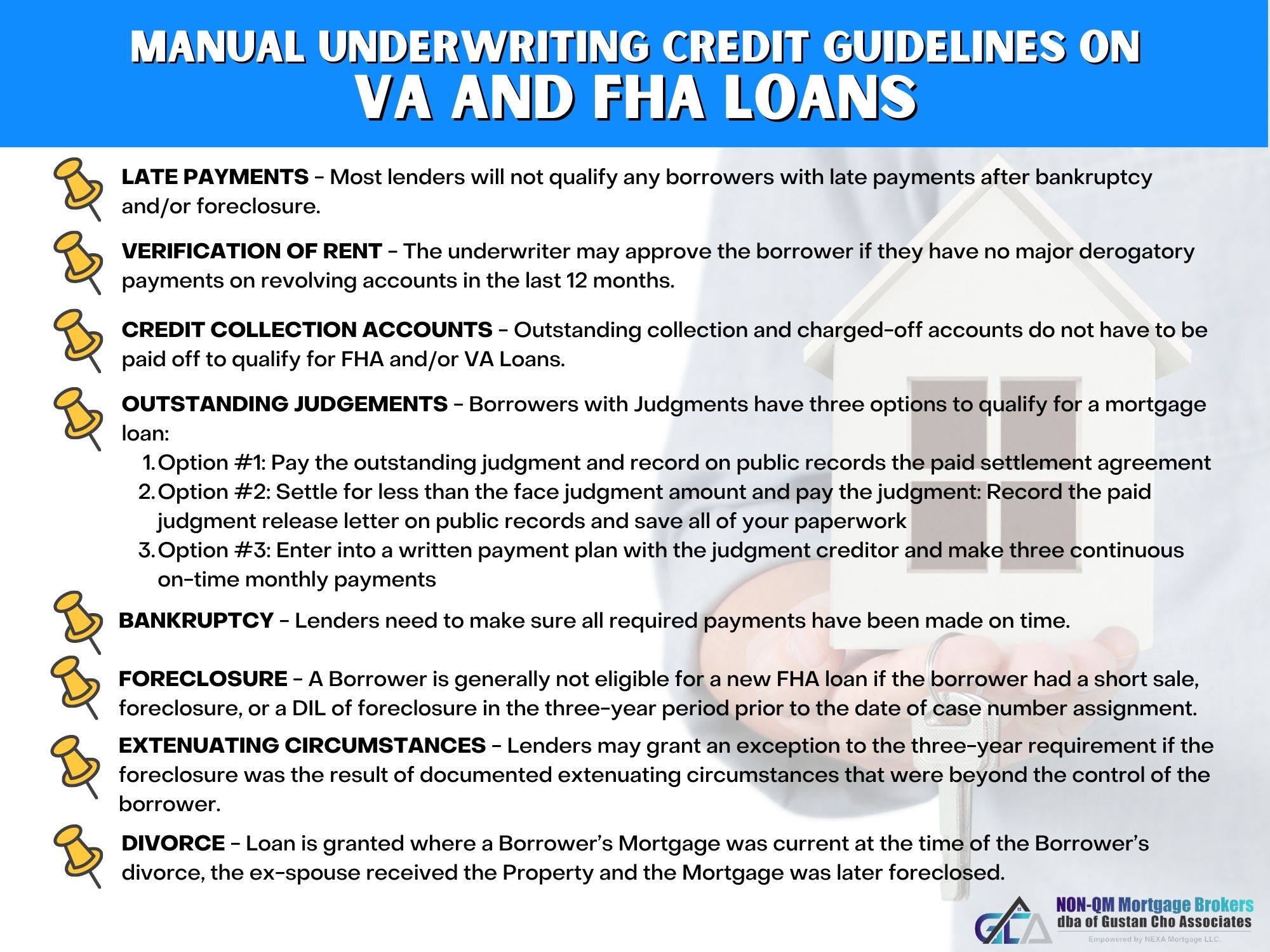

Because the FHA insures these loans, underwriting requirements are more relaxed compared to conventional mortgages. This allows more buyers to qualify. Lenders can also rest assured they will be compensated in case of default.

Key Requirements for Virginia FHA Loans

While FHA loans offer more flexibility, you still must meet certain standards to get approved. Here are the key FHA loan requirements in Virginia:

Credit Score

For an FHA loan in VA, you’ll need a minimum credit score of 580. The higher your score, the better your interest rate and terms will be. Here’s how your down payment amount corresponds to your credit score:

- 500-579 FICO – 10% down payment

- 580+ FICO – 3.5% down payment

Some lenders may impose higher score requirements Shop around to find a lender that will approve your credit situation.

Down Payment

FHA loans allow down payments as low as 3.5%. On a $300,000 home purchase, your minimum down payment would be just $10,500.

Gift funds and down payment assistance programs can be used for your down payment if you don’t have sufficient cash on hand.

Debt-to-Income Ratio

Your front-end DTI (or housing DTI) can be no higher than 31% with an FHA loan. This ratio measures your monthly mortgage payment in relation to your gross monthly income.

Your back-end DTI (total monthly debt payments) must not exceed 43%. In certain cases, a ratio up to 57% may be allowed if you have sufficient compensating factors like a hefty down payment or stellar credit.

Mortgage Insurance

FHA loans require you pay an upfront mortgage insurance premium of 1.75% of the loan amount. This premium gets rolled into your loan balance.

You’ll also pay an annual mortgage insurance premium between 0.45% – 1.05% of your loan amount. This gets added to your monthly payment.

Homebuying Counseling

First-time homebuyers in Virginia using an FHA loan must complete HUD-approved counseling before closing. Many programs are available for free online or over the phone.

Occupancy and Property Requirements

FHA loans are only eligible for primary residences – not second homes or investment properties. Single-family homes, townhouses, and condos pre-approved by FHA are eligible.

Employment History

Expect to show 12 months of steady employment history. Self-employed buyers will need to provide additional documentation like tax returns.

Minimum Borrower Investment

Borrowers must contribute at least 3.5% of the purchase price from their own funds. Additional down payment amounts can come from gifts.

Loan Term

FHA loans come in 15-year or 30-year terms. The 30-year option offers lower monthly payments while the 15-year term builds equity faster.

FHA Loan Limits in Virginia

In more expensive housing markets, FHA loans are capped at certain amounts. Here are the 2024 FHA loan limits for Virginia:

- 1-unit home: $498,257 to $1,149,825

- 2-unit home: $637,950 to $1,472,250

- 3-unit home: $771,125 to $1,779,525

- 4-unit home: $958,350 to $2,211,600

Loan limits vary by county and property type. Check your county limit before applying.

Who Offers FHA Loans in Virginia?

Many national lenders and community banks offer FHA loans in VA. Here are some top FHA lenders to consider:

- Quicken Loans

- Fairway Independent Mortgage Corporation

- Caliber Home Loans

- Freedom Mortgage

- loanDepot

- Guild Mortgage

Reach out to multiple lenders to compare interest rates and fees. Look for a lender that provides an easy application process and strong customer service.

Alternatives to FHA Loans in Virginia

An FHA loan isn’t your only option. Here are a few other programs available in Virginia:

VA Loans – Offered to veterans, service members, and some spouses. Require 0% down payment.

USDA Loans – For rural/suburban areas. 100% financing available.

Conventional 97 – 3% down payment option from Fannie Mae or Freddie Mac.

Down payment assistance – First-time buyer programs offering grants, loans, or tax credits to assist with down payment and closing costs.

Compare all programs to find the optimal home loan for your situation.

The Bottom Line

FHA loans open homeownership possibilities for buyers who can’t meet stricter conventional loan requirements. If you have past credit issues or limited funds for a down payment, an FHA loan is a suitable option. Just be sure you understand and meet all the requirements outlined above before applying for maximum approval chances.

What is the max FHA loan in Virginia?

FHA loans have maximum loan limits based on county. There are many counties in Virginia that adhere to the common limit of $498,257 for a single-family home. However, there are many counties where that limit is higher because the value of property is higher. Many counties in Virginia have loan limits up to $1,149,825 for single-family homes.

Virginia FHA Loan Benefits

FHA loans are popular with homebuyers because of their many benefits. They are designed to help people who have no credit history and less-than-perfect credit get a mortgage. FHA loans can also help people who have experienced foreclosure or bankruptcy.

Here are some of the benefits of FHA loans.

- Low Down Payments: Having a low down payment option is one of the main reasons FHA loans appeal to first-time homebuyers. In some cases, borrowers can qualify for a down payment as low as 3.5%.

- Down Payment Assistance Programs: Down payment assistance programs are available throughout the United States. Each state has their own unique programs both at the state and city level. The Virginia Department of Housing and Community Development offers down payment assistance and assistance with closing costs. Down payment assistance is often made available to first-time homebuyers. You can find other resources for homebuyers in Virginia at HUD.

Homebuyer assistance programs have their own sets of requirements for eligibility. It is up to the borrower to research these programs and organize with them independently of their lender.

- Gift funds can be used for down payment: You can use financial gifts from friends and family to pay for the down payment on your home.

- Higher Debt-To-Income Ratio: FHA loans can have a DTI of as much as 57%. This makes FHA loans easier to qualify for than Conventional loans where the DTI can only be up to 45%.

- No Monthly Minimum Income Requirement: Income must be verifiable and consistent for the last two years. However, there is no minimum amount a borrower must make in order to qualify for an FHA loan.

- A Variety of Loan Types to Choose From: There are several FHA loan options for homebuyers. Streamline Refinance and the FHA 203(k) are two of the more popular FHA loans available. Check out all FHA loans offered by New American Funding.

- Some or All Closing Costs Can be Covered by the Seller: FHA loans allow the seller to contribute up to 6% of the sales price to cover the buyer’s closing costs. Closing costs are usually somewhere between 2% and 5% of the purchase price. They can include appraisal and inspection fees, a loan origination fee, and service fees.

- Assumable Loans: The borrower can assume an existing mortgage. The mortgage will be transferred to the buyer from the seller. The homebuyer will be subject to the terms, conditions, and rates of the original FHA loan.

- A Variety of Eligible Properties: They are available for single-family detached homes, 2-4 unit homes, condos, townhomes, and manufactured homes.

Virginia FHA Loans – How to Qualify

FAQ

What are the qualifications for an FHA loan in Virginia?

What will disqualify you from an FHA loan?

What is the downside of an FHA loan?

How much proof of income do you need for a FHA loan?

Can I get an FHA loan in Virginia?

To qualify for an FHA loan in Virginia, your home loan must be below the local FHA loan limits in your area. For 2024, the maximum loan limit in Virginia is $498,257 for a single-family home and $2,211,600 for a four-plex. Limits varies by county. The minimum loan limit is $5,000. Loan limits vary by county and home size.

How do I qualify for an FHA loan in Virginia?

To qualify for an FHA loan in Virginia, you’ll need to meet the following criteria: → Credit score. FHA loans require at least a 580 credit score, but a higher score means a lower down payment. If your score is 580 or above, you can qualify for a 3.5% down payment versus a 10% down payment for scores between 500 and 579. → Debt-to-income ratio.

How much is an FHA loan in Virginia?

You can get an FHA loan in Virginia with a credit score as low as 500. FHA loan limits vary by county and range from $498,257 to $1,149,825 for single-family homes in Virginia. Here’s what you need to know about FHA loans and their limits in Virginia before you apply. How are FHA loan limits determined?

What are FHA loan limits in Virginia?

FHA loan limits vary by county and range from $498,257 to $1,149,825 for single-family homes in Virginia. Here’s what you need to know about FHA loans and their limits in Virginia before you apply. How are FHA loan limits determined? Each year, the FHA sets a maximum loan amount that it will insure within a given area.