If you’re a veteran or active military looking to build your dream home, a VA new construction loan may be a great option for you. As someone who has researched these unique loans extensively, I want to provide an in-depth guide to help you understand what VA new construction loans are, who qualifies, and how the process works from start to finish.

What is a VA New Construction Loan?

A VA new construction loan is a mortgage issued by private lenders that allows eligible borrowers to finance the construction of a new home. It provides Veterans and servicemembers a way to build a custom home tailored to their needs and family size without requiring a down payment.

Unlike a traditional VA loan where you receive one lump sum to purchase an existing home, a VA new construction loan disburses funds in phases based on the stages of construction This ensures the home is built according to the approved plans and specifications

Key Benefits of VA New Construction Loans

There are several advantages to VA new construction loans that make them appealing to Veterans and active duty servicemembers:

-

No down payment required – This major perk sets VA new construction loans apart. No down payment is needed to start construction on your new home

-

No private mortgage insurance (PMI) – Because no down payment is required, you won’t have to pay for PMI which is usually mandatory with low down payment mortgages. This saves you money each month.

-

Lower interest rates – VA new construction loans typically come with lower interest rates compared to other loan programs Rates are set by lenders but VA loans offer very competitive rates

-

No VA funding fee – On a traditional VA loan, you normally have to pay a VA funding fee. However, eligible borrowers can receive an exemption from this fee when using a VA new construction loan.

-

Customizable home design – You get to work with a builder to design your ideal home tailored to your family. This level of customization is not possible when buying an existing house.

-

Single closing – Some lenders offer VA construction loans with only one closing. This saves significantly on closing costs compared to other construction loans.

-

May recoup down payment – If you opt to make a down payment, it may be possible to recoup those funds in cash back at closing when you convert to a permanent VA mortgage.

Who Qualifies for a VA New Construction Loan?

To be eligible for a VA new construction loan, you must first meet the basic VA loan requirements:

- Be an active duty servicemember, Veteran, National Guard/Reservist, or qualifying surviving spouse

- Have sufficient income and credit score to qualify

- Occupy the home as your primary residence

In addition, VA new construction loans have these extra requirements:

- Locate a VA-approved builder

- Provide complete construction plans and specifications

- Use a VA appraiser to assess the building plans

- Supply any additional documentation the lender requests

Meeting standard VA loan criteria along with the new construction-specific guidelines is necessary for approval. I’ll explain the detailed process shortly.

How Does the VA New Construction Loan Process Work?

Now that you understand the basics of VA new construction loans, let’s walk through the steps to get one. Be aware this is a lengthy process that demands patience and organization.

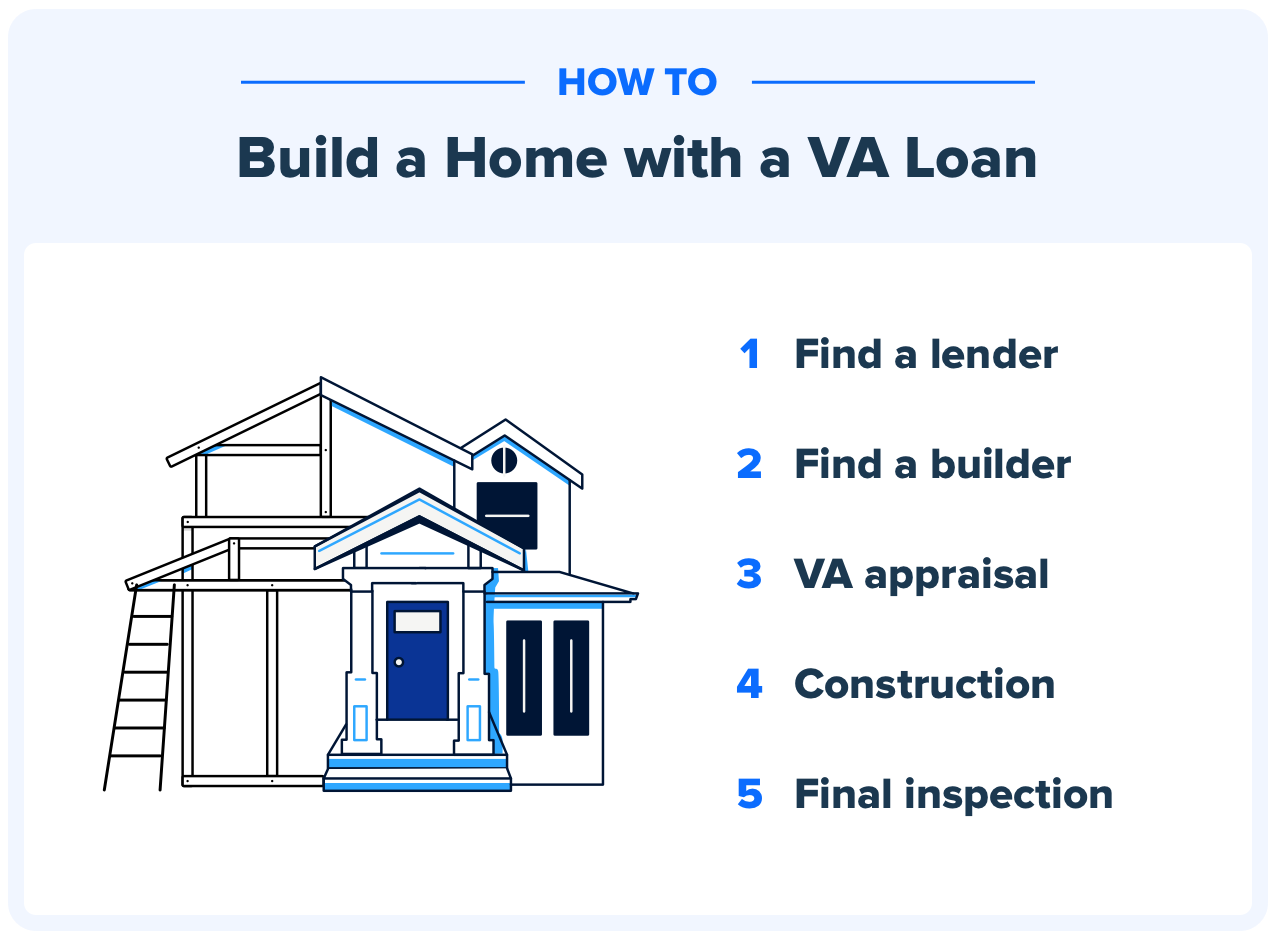

Step 1: Obtain a VA Certificate of Eligibility

The first thing you need is a Certificate of Eligibility (COE) to confirm you meet the VA loan requirements. Submit your COE along with proof of your VA eligibility such as discharge papers.

Step 2: Get Pre-Approved for a Loan Amount

Next, shop around for VA lenders offering new construction loans and get pre-approved. Pre-approval is key to determine the loan amount and type of home you can comfortably afford. Not every lender provides VA new construction loans so search thoroughly.

Step 3: Locate a VA-Approved Builder

You must use a builder registered in the VA database. Confirm their licensing, insurance, credentials, and experience building VA new construction homes. Provide your builder with the construction plans and specs for approval.

Step 4: Order a VA Appraisal

A VA appraiser will assess the building plans and issue a Notice of Value for the home’s estimated value upon completion. The appraisal ensures the home will meet VA minimum property standards when finished.

Step 5: Close on the Loan and Start Construction

Now you can close on the loan and start your exciting build! For a true VA new construction loan, you’ll close before ground is broken on the home. The loan funds will be distributed in phases as construction milestones are met.

Step 6: Complete VA Inspection

The final step is the VA compliance inspection once construction is finished. This confirms your home was built according to the approved plans and meets VA guidelines.

If you followed the proper process, your lender can now convert the construction loan into permanent financing. This is often handled by refinancing into a standard VA mortgage.

Alternatives if You Can’t Get a VA New Construction Loan

Although ideal, VA new construction loans can be hard to come by these days. If you have trouble finding a lender, there are a couple alternative options:

Traditional Construction Loan – Get a conventional construction loan requiring a down payment from a bank or builder. Then convert it to permanent VA financing later. Shop around for the best terms on down payment and interest rate.

Owner-Builder Construction – Act as an owner-builder instead of using a VA-approved builder. Get the construction loan, build the home yourself, and refinance into a VA mortgage when complete. This path demands technical expertise.

Either of these alternatives paired with refinancing to a VA loan allow you to ultimately maximize your VA benefits and save money.

Tips for Getting Approved

To boost your chances of successfully getting approved for a VA new construction loan, keep these tips in mind:

-

Seek out reputable VA lenders and builders with proven experience

-

Ensure your income and credit score meet lenders’ standards

-

Calculate costs accurately and set a realistic budget

-

Research the construction timeline in your area

-

Provide complete documentation quickly when requested

-

Get pre-approved early and start the building process ASAP

-

Double check that all VA requirements are being met throughout

Following the proper steps and guidelines is crucial for securing your VA new construction loan. Being organized and proactive will go a long way.

The Bottom Line

For Veterans and servicemembers looking to build their dream home, a VA new construction loan offers a zero down payment path to homeownership. These specialized loans provide huge benefits tailored specifically to eligible borrowers like lower rates and no VA funding fee.

Despite more complex qualification and approval processes, VA new construction loans enable you to fully customize your home. Working with reputable lenders and builders knowledgeable about VA guidelines streamlines getting your project from blueprint to breaking ground. With proper research and planning, you can make building your own home a reality.

What Is A VA Construction Loan?

Your Credit Profile Excellent 720+ Good 660-719 Avg. 620-659 Below Avg. 580-619 Poor ≤ 579

When do you plan to purchase your home? Signed a Purchase Agreement Offer Pending / Found a House Buying in 30 Days Buying in 2 to 3 Months Buying in 4 to 5 Months Buying in 6+ Months Researching Options

Do you have a second mortgage?

Are you a first time homebuyer?

Consent:

By submitting your contact information you agree to our Terms of Use and our Privacy Policy, which includes using arbitration to resolve claims related to the Telephone Consumer Protection Act.! NMLS #3030

Congratulations! Based on the information you have provided, you are eligible to continue your home loan process online with Rocket Mortgage.

If a sign-in page does not automatically pop up in a new tab, click here

VA One-Time Close :: How To Get A Construction Loan With A VA Loan

FAQ

Can you use a VA home loan on a new construction home?

What is the minimum credit score for a VA construction loan?

What is the debt to income ratio for a VA construction loan?

Do VA loans cover builds?

How do I get a VA loan for new construction?

Talk with a VA lender before getting a construction loan. To secure a VA loan for new construction, you’ll first need to qualify for a VA loan. That means you or your spouse must meet the VA’s service requirements and obtain a VA Certificate of Eligibility (COE), which we’ll discuss more below.

How does a VA construction loan work?

Here’s how it works: 1.**Purpose**: A VA construction loan is specifically designed for building a new home.Unlike regular mortgages, where you receive a lump sum upfront, a VA construction loan provides

Can a VA construction loan help you build your dream home?

For eligible borrowers, a VA construction loan can simplify the process of building your dream home.

Does the VA back construction loans?

The VA doesn’t back loans — whether for new home purchases or construction — for just anyone. You need to meet specific requirements as far as your service goes. Those vary depending on when you served. If you’re on active duty, you’re eligible for a VA construction loan as soon as you hit 90 days of continuous service.