VA loans are mortgage loans backed by the US. Department of Veterans Affairs that help eligible veterans, active duty service members, and surviving spouses finance a home Texas has one of the largest veteran populations in the country, so VA loans are very popular for homebuying in the state. This comprehensive guide covers everything you need to know about getting a VA mortgage in Texas.

Overview of VA Loans

The VA home loan program started in 1944 as part of the GI Bill to help WWII veterans purchase homes after returning from the war. It has expanded over the years and now offers the following key benefits:

-

No down payment required – 100% financing means veterans don’t need cash savings to buy a home

-

No monthly mortgage insurance – Unlike conventional loans, no additional monthly MI premiums are required.

-

Lower interest rates – VA loans often have lower rates than conventional or FHA loans.

-

More flexible credit guidelines – VA has more lenient standards for credit score, debt-to-income ratio and bankruptcy.

-

Reusable benefit – Veterans can use their VA eligibility again and again to purchase additional homes.

These features make VA loans one of the most affordable and accessible mortgage options for eligible borrowers.

VA Loan Eligibility in Texas

The basic requirements to get a VA loan in Texas include:

- Minimum of 90 days active duty service

- Dishonorable discharge exclusion

- Entitlement not previously used up

- Sufficient income and credit qualifications

Detailed eligibility guidelines can be found on the VA website. Those who qualify receive a Certificate of Eligibility (COE) to verify their status to lenders.

Surviving spouses of veterans may also be eligible if the veteran died in service or from a service-connected disability.

How VA Loans Work in Texas

VA loans themselves come from private lenders – banks, credit unions, mortgage companies. Eligible borrowers can shop multiple lenders to find the best rates and fees.

Rather than originating loans, the VA guarantees a portion of the loan amount, protecting the lender against loss if the borrower defaults. This enables lenders to offer better terms than conventional loans.

It is important to note the VA does not actually lend money directly. They simply set the rules of the program that lenders must adhere to.

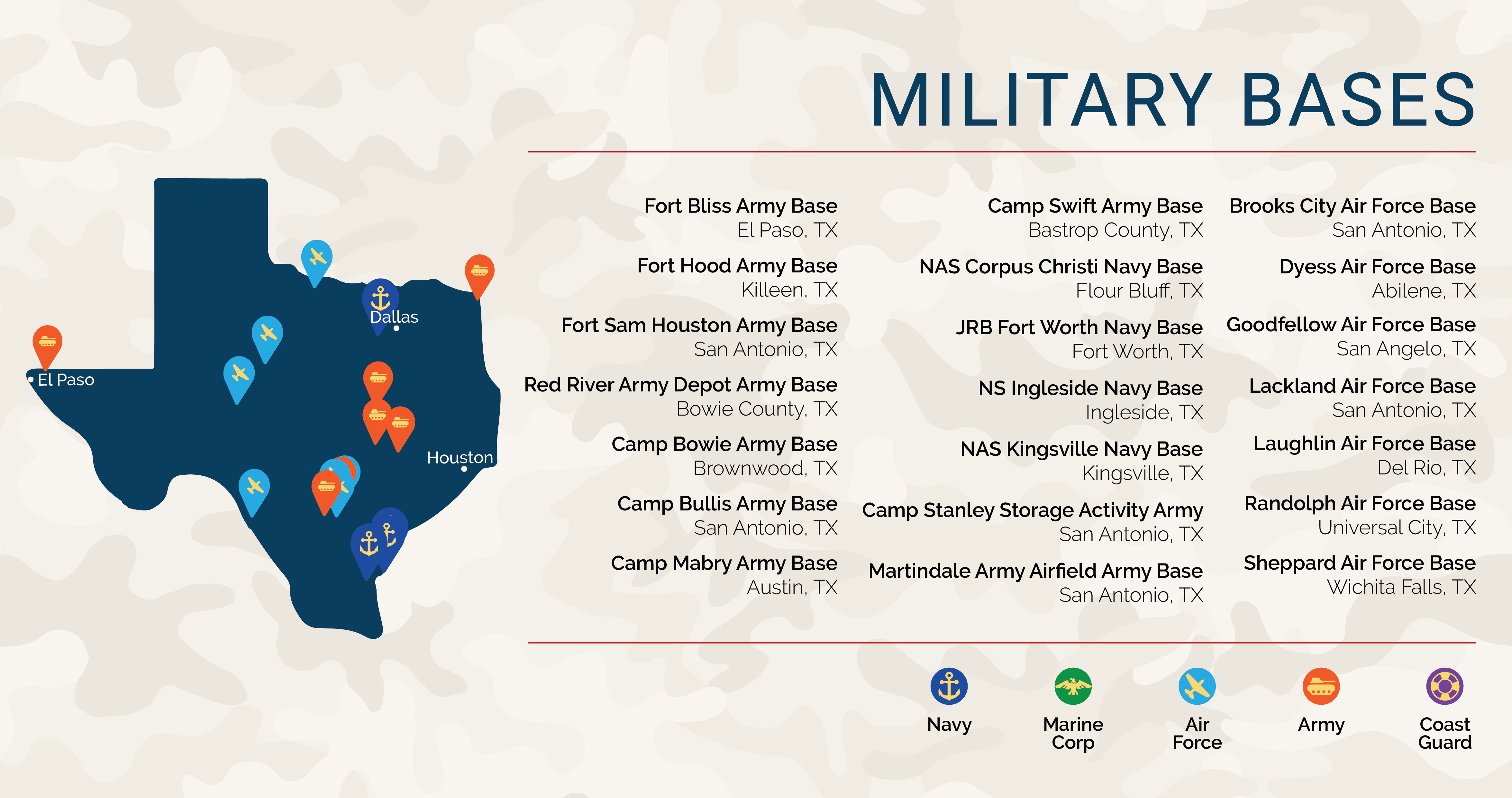

VA Loan Limits in Texas

The 2023 VA loan limits for Texas counties are:

- $723,750 for most counties

- $1,089,300 for El Paso, Fort Bend, Hays, and Travis counties

- $1,581,750 for Dallas, Denton, Tarrant, and Collin counties

Higher cost areas like Austin, Dallas and Houston have VA limits exceeding conventional conforming loan amounts. This allows veterans in these markets to finance more expensive homes without a jumbo loan.

Loan limits for surviving spouses are lower than for veterans in Texas. See the VA website for details by county.

Texas VA Loan Options

Veterans in Texas can use their VA home loan benefit in a few different ways:

-

VA Purchase Loan – For buying a home as a primary residence. This is the most common usage.

-

VA Cash-Out Refinance – Pulls equity out of an existing home to get cash. Requires seasoning rules to be met.

-

VA Streamline Refinance – Lower rate/payment on current VA mortgage with limited documentation.

-

VA Renovation Loan – Finance home improvements into the mortgage.

-

VA Energy Efficient Mortgage – Buy/renovate a green home and finance energy updates.

Each type has specific guidelines and purposes for utilizing a VA loan. Veterans can discuss options with a lender to decide the best fit.

Applying for a VA Home Loan in Texas

The process for getting a VA mortgage in Texas involves just a few key steps:

- Obtain Certificate of Eligibility from the VA

- Get pre-approved from a lender

- Make an offer and enter contract on a home

- Allow lender to order the VA appraisal

- Complete loan application and provide documents

- Close on the home purchase

It is very similar to a conventional mortgage timeline, with the main difference being the required VA appraisal.

Getting pre-approved early on gives veterans in Texas better buying power for negotiating and placing competitive offers.

Texas Veterans Land Board VA Home Loans

Beyond regular VA loans from private lenders, Texas veterans also have access to the Veterans Land Board loan programs administered by the Texas General Land Office. These include:

- VLB VA Home Loans

- VLB VA Home Improvement Loans

VLB offers below market interest rate VA loans to Texas veterans. This state veterans program provides an additional source of 100% financing.

Eligibility requires Texas residency. VLB VA loans can be used alongside or separately from regular VA entitlement.

Finding a VA Lender in Texas

It’s important for veterans in Texas to shop different lenders to find the best VA loan terms and service. Key factors to consider include:

- Interest rates

- Origination fees

- Closing costs

- Discount points charged

- Processing timelines

- Customer service

Both national and local lenders offer VA loans in Texas. Online lenders provide a simple option, while community banks and credit unions cater to more customized lending needs.

The VA does not recommend any specific lenders. Veterans should evaluate multiple quotes before choosing where to apply.

The Bottom Line on Texas VA Loans

For eligible veterans and military members buying a home in Texas, a VA loan provides affordable 100% financing options with many perks over conventional mortgages. Understanding the guidelines, exploring all the VA loan types available, and shopping different lenders will lead to success in finding the best financing.

Main pillars of the VA home loan benefit

- No downpayment required (*Note: Lenders may require downpayments for some borrowers using the VA home loan guaranty, but VA does not require a downpayment)

- Competitively low interest rates

- Limited closing costs

- No need for Private Mortgage Insurance (PMI)

- The VA home loan is a lifetime benefit: you can use the guaranty multiple times

About Home Loans

VA helps Veterans, Servicemembers, and eligible surviving spouses become homeowners. As part of our mission to serve you, we provide a home loan guaranty benefit and other housing-related programs to help you buy, build, repair, retain, or adapt a home for your own personal occupancy.

VA Home Loans are provided by private lenders, such as banks and mortgage companies. VA guarantees a portion of the loan, enabling the lender to provide you with more favorable terms.

VA Loan Updates and Changes in 2024: What #veterans and #military should consider before buying

How do I qualify for a VA loan in Texas?

To get you started, we’ve outlined some basic VA loan requirements in Texas. To start the loan application process, you must apply for a Certificate of Eligibility (COE) from the VA. We can also take care of the COE application on your behalf. This document specifies your entitlement, or VA-approved funds, to your mortgage company.

What is the maximum VA loan amount for Texas?

Since the Texas VA loan limit is $647,200, the total amount the VA will insure is $161,800, or 25% of $647,200. This means you have a total remaining entitlement of $86,800—the difference between $161,800 and $75,000. If you’re interested in purchasing a home, reach out to an OVM Financial expert.

What are the benefits of a VA loan in Texas?

One great benefit of VA home loans is that there’s the option of a 0% down payment. Your COE spells out what you can borrow without having to put further money down. However, if you have remaining entitlement, you may have to make a down payment if 25% of your home’s price exceeds your remaining entitlement.

Are VA loans available to veterans in Texas?

Depending on your eligibility, you can secure a VA home loan in Texas if you’re a veteran, active service member, or surviving spouses with the help of the U.S. Department of Veterans Affairs.