Getting your first home loan can be an intimidating process. With so many options out there, it can be hard to know where to start. Two popular mortgage programs for first-time homebuyers are USDA and FHA loans. Both offer low down payments and flexible credit requirements. But there are some key differences you need to understand before deciding if a USDA or FHA loan is right for you.

In this comprehensive guide, we’ll explain everything you need to know about USDA and FHA loans. You’ll learn about

- The basics of USDA and FHA loans

- Key eligibility requirements

- Pros and cons of each loan type

- How to choose the best option

Let’s dive in!

What Are USDA and FHA Loans?

USDA and FHA loans are government-backed mortgage programs aimed at helping low-to-moderate income buyers and those with lower credit scores purchase a home.

The main benefits of these loans include:

- Low or no down payment required

- More flexible credit standards

- Lower interest rates than conventional loans

- Access to down payment assistance programs

USDA loans are backed by the United States Department of Agriculture. They are exclusively for homes ineligible rural and suburban areas.

FHA loans are insured by the Federal Housing Administration (FHA). They can be used to buy a home anywhere in the U.S.

Now let’s take a closer look at the eligibility requirements.

USDA and FHA Loan Eligibility

When deciding between USDA vs FHA, the first thing to look at is which loan you qualify for. Here are some key eligibility factors:

Location

USDA – Only eligible in rural areas and some suburban neighborhoods. Not available in cities.

FHA – Available in any location across the U.S.

Income Limits

USDA – Must be below 115% of the median income for your area, Income limits vary by county

FHA – No income limits.

Credit Score

USDA – Typically requires a minimum credit score of 640.

FHA – Allows scores as low as 580 with a manual underwrite.

Debt-to-Income Ratio

USDA – Max DTI of 29%/41% (with compensating factors).

FHA – Max DTI of 31%/43% (with compensating factors).

Down Payment

USDA – 100% financing available. No down payment required.

FHA – Minimum 3.5% down payment required.

As you can see, FHA loans are available to more buyers based on location, income, and credit score. USDA has stricter eligibility standards but offers a no down payment option.

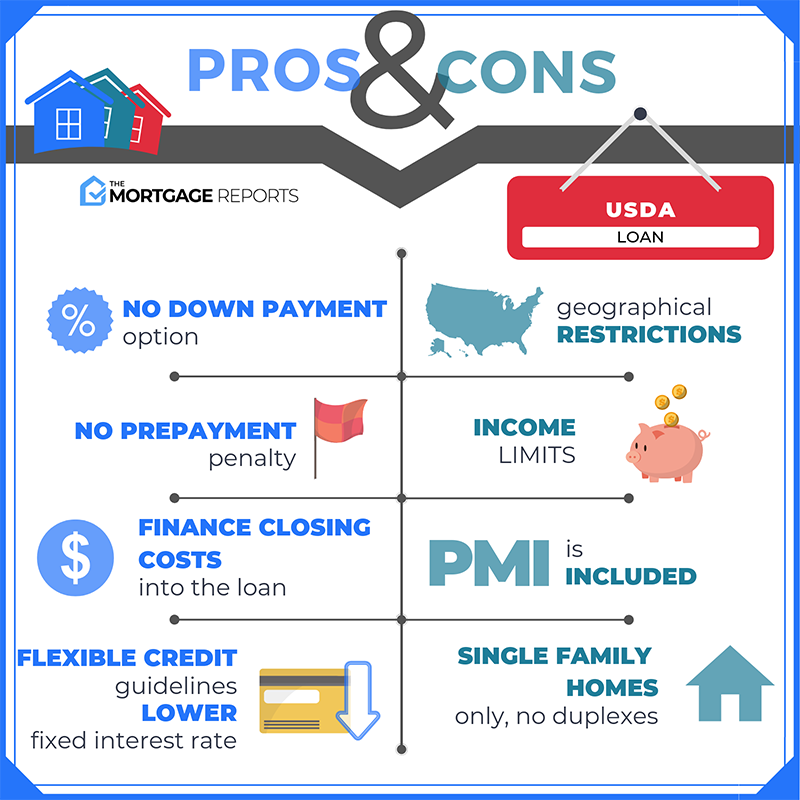

Pros and Cons of USDA Loans

USDA loans offer some great benefits, especially when it comes to affordability. But they aren’t right for everyone. Here are the key pros and cons:

Pros

- No down payment or closing costs required

- Low mortgage insurance rates

- Fixed low interest rates

- Can finance up to 100% of the home’s value

- More flexible debt-to-income ratios than conventional loans

Cons

- Limited to rural/suburban areas

- Income limits apply

- Must meet USDA property requirements

- Slower loan process due to double underwriting

The no down payment feature and cheap mortgage insurance make USDA loans very appealing. Just keep in mind eligibility is limited to certain locations and borrowers.

Pros and Cons of FHA Loans

FHA loans are extremely popular due to their flexible credit guidelines and low down payments. But they aren’t perfect either. Here are the key pros and cons:

Pros

- Only 3.5% down payment required

- Available with credit scores as low as 580

- Lower interest rates than conventional loans

- Allows higher debt-to-income ratios

- Available anywhere in the U.S.

Cons

- Requires mortgage insurance (MIP)

- MIP is more expensive than USDA

- Not available for investment properties

- Lower loan limits than conventional loans

The FHA’s lenient credit and down payment requirements make it a top choice for many. Just be prepared to pay the ongoing MIP premium.

How To Choose: USDA vs FHA Loans

So when it comes down to USDA vs FHA, how do you decide? Here are a few key questions to ask yourself:

-

Where do you want to buy? The property location will determine if a USDA loan is an option. Use the USDA eligibility tool to check.

-

What’s your income? Make sure you fall below the limit to qualify for a USDA loan. FHA has no income limits.

-

What’s your credit score? FHA allows much lower scores but USDA may offer better rates if your score is very good.

-

How much can you afford for a down payment? If you can’t afford 3.5% down, USDA is your only zero-down option.

-

Do you qualify for down payment help? Down payment assistance programs can be used with both loans.

-

Which lender has the better deal? Get rate quotes for both loans and compare costs.

Speaking with a knowledgeable loan officer is the best way to weigh the pros and cons of both programs. They can check your eligibility and provide rate quotes so you can make the right decision.

Be sure to ask about down payment assistance programs too. They provide grants, loans, or tax credits that can be combined with USDA and FHA financing to cover your down payment and closing costs.

Tips for Getting Approved

Here are a few quick tips to boost your chances of getting approved for an FHA or USDA home loan:

- Work on improving your credit score – aim for at least 640

- Lower credit card balances to decrease your debt-to-income ratio

- Save up a little money for closing costs and emergencies

- Gather all required documentation early in the process

- Get pre-approved so you stand out when making an offer

Taking these steps will put you in a strong position to get approved and find the right home loan option for your situation.

The Bottom Line

When it comes to affordability and flexibility for homebuyers, it’s hard to beat USDA and FHA loans. Both allow low down payments and have more relaxed credit standards than conventional mortgages.

Just be sure to consider all the pros, cons and eligibility requirements before choosing USDA vs FHA. Connect with an experienced loan officer to get pre-approved and see which mortgage program you qualify for. This will set you up for success on the path to first-time homeownership!

Pros and cons of USDA loans

The USDA loan has quickly risen in popularity with first-time and lower-income borrowers thanks to its zero-down allowance and low rates. But not everyone will qualify. Here’s what you should know.

Differences between USDA and FHA loans

When comparing USDA vs FHA loans, both government-backed, differences emerge in terms of application, underwriting, appraisal, loan amounts, mortgage insurance, interest rates, and more. Prospective borrowers should carefully analyze the details of USDA vs FHA loans to make an informed decision based on their specific financial circumstances and homeownership aspirations.

Are USDA or FHA Loans Better?

FAQ

Is USDA or FHA better?

What is one advantage a USDA loan has over the FHA loan ______?

What credit score do you need for a FHA and USDA loan?

What is the advantage of a USDA loan?

How do I qualify for an FHA vs USDA loan?

Being eligible for an FHA vs. USDA loan means meeting specific requirements. To qualify for an FHA loan, prepare to: Make a down payment of at least 3.5% with a credit score of 580 or higher, or a down payment of 10% with a credit score between 500 and 579. Pay an upfront mortgage insurance premium at closing equivalent to 1.75% of the loan.

Are USDA vs FHA loans better?

When comparing mortgage options, such as USDA vs FHA loans, the better choice largely hinges on one’s financial situation. For instance, individuals with lower credit scores may discover that FHA loans suit their needs best.

What is the difference between FHA and USDA mortgages?

The FHA program offers 30-year and 15-year fixed-rate mortgages, along with adjustable-rate mortgages (ARMs). The USDA offers only a 30-year fixed-rate loan. In addition, both programs require you to buy a primary residence, meaning you can’t use them for a vacation home or investment property.

Why are USDA and FHA loans so popular?

Home buyers with low or moderate incomes may gravitate toward mortgages with more lenient borrowing requirements, especially when it comes to down payments and mortgage insurance. This is why USDA and FHA loans can be so appealing to borrowers. How do the two types of mortgage loans differ, though?