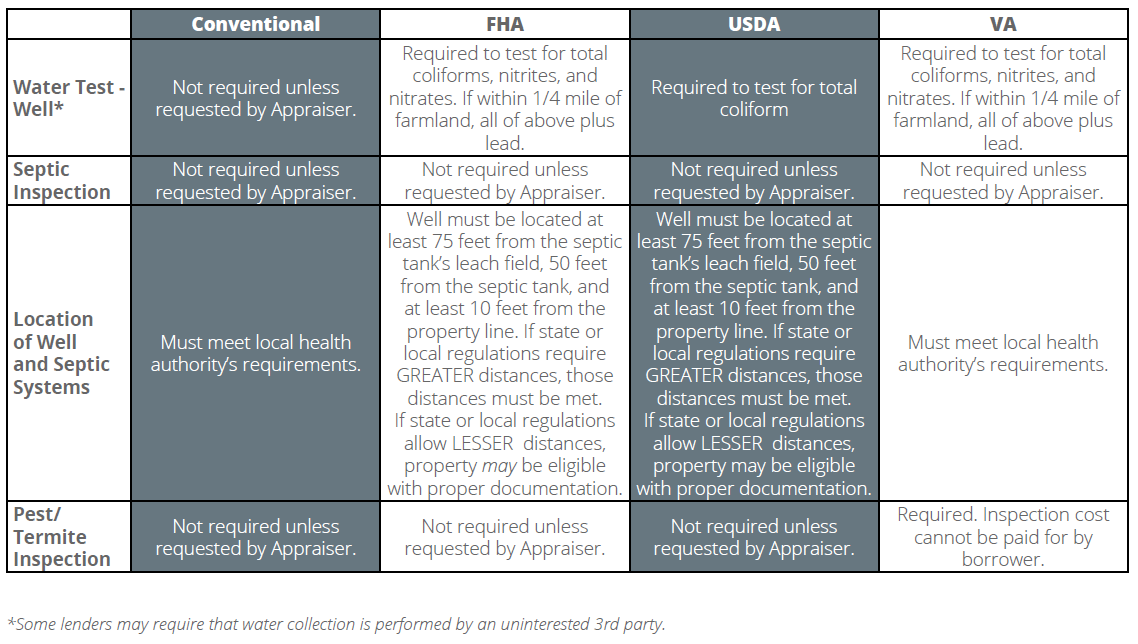

Though USDA loans only officially require an appraisal — not an inspection — USDA buyers should still consider seeking one. Home inspections help buyers better understand the property they’re planning to purchase and provide options in the event the home has problems or defects.

It’s easy to confuse an appraisal with a home inspection. Though both involve a third-party assessment of a property, they each have a unique end-goal in mind. While the appraisal is meant to assess the home’s fair market value, the home inspection is designed to evaluate the property’s safety and condition for the buyer.

Appraisals for government-backed loans include a look at the property in light of broad health and safety guidelines. But this evaluation is not as in depth or extensive as a home inspection.

The USDA home loan program helps low-to-moderate income buyers in rural areas finance a home, These government-backed mortgages offer competitive interest rates and require no down payment

But before you can close on a USDA loan, the property must pass an eligibility inspection. Pest and termite inspections are a key component.

In this comprehensive guide we’ll cover everything you need to know about pest and termite inspections for USDA loans including

- Why they’re required

- When they need to be completed

- Who can perform the inspection

- What specifically is looked for

- How to handle any issues found

Understanding the pest inspection requirements for a USDA home loan will help ensure your purchase goes smoothly

Why Pest Inspections Are Required

The USDA wants to minimize risks to themselves and the buyer by requiring a professional pest inspection. Termites, wood boring beetles, and fungal rot can severely damage the structural integrity of a home if left unchecked.

Pest infestations can be extremely expensive to treat. The USDA mandates a qualified inspector assess the property so any existing issues are identified before you take ownership.

Both your lender and appraiser can also make pest inspections a condition of approving the loan or establishing value. It provides one more layer of protection for all parties.

When Do Pest Inspections Need to Be Done?

Ideally, the pest inspection should be completed as soon as possible once you are under contract.

USDA guidance states it must be finished no more than 30 days prior to loan closing. Any wood destroying insects or organisms found must be treated prior to closing as well.

Doing the inspection early on gives you plenty of time to negotiate treatment or repairs if any problems are uncovered. You don’t want to delay closing because issues surfaced at the last minute.

Who Can Perform the Inspection?

USDA regulations require a state-licensed pest control operator or other qualified professional complete the inspection. This ensures an experienced, knowledgeable inspector assesses the property.

Some states license general home inspectors to perform pest inspections while others require a specialized pest control operator license. Your real estate agent can provide inspector recommendations that meet state requirements.

Termite inspectors, also called wood destroying organism (WDO) inspectors, are most common. But have the inspector verify they can conduct a full pest inspection suitable for USDA approval, not just termites.

What Do Pest Inspectors Check For?

At minimum, the pest inspector will check all accessible areas of the interior and exterior for signs of wood destroying insects and fungus. This includes:

- Termites – Subterranean, drywood, dampwood

- Carpenter ants, carpenter bees

- Powderpost beetles

- Old house borers

- Wood decay fungi

They will look for conducive conditions, like moisture or wood-soil contact, that enable pest infestations. Evidence such as mud tubes, frass, and pinholes will be noted. Recommendations for corrections will be provided.

The inspector should also check for other pests like rodents, cockroaches, and fabric pests. Alerting the USDA of any pest conducive conditions supports their mission of improving rural housing.

How Are Issues Handled?

If the inspection reveals active wood destroying insect infestation, the lender will require evidence of treatment prior to closing. Fungi and pest conducive conditions will need correction as well.

Most lenders can escrow funds at closing for minor pest control and repairs needed. Anything more substantial requires correction beforehand.

If major structural damage from untreated prior infestations is uncovered, the property may fail to meet USDA health and safety standards. In that case, significant repairs would need to be negotiated with the seller before closing.

Being aware of the home’s condition early allows time for proper treatment and repairs. Don’t wait until the last minute!

5 Tips for Passing Pest Inspection

Follow these tips to help ensure your property passes the pest inspection process smoothly:

1. Have the inspection done ASAP once under contract. This gives you plenty of time to address any issues found. Waiting until right before closing risks delay.

2. Hire a qualified, state-licensed inspector. Confirm they meet USDA and state requirements to perform pest inspections. Ask your real estate agent for references.

3. Attend the inspection. You can get a first-hand look at the home’s condition and ask the inspector questions.

4. Negotiate pest treatment and repairs with the seller quickly. Get everything completed well in advance of closing day.

5. Thoroughly review the inspection report. Understand any recommendations that need to be followed post-closing to keep the home pest-free.

The Bottom Line

Pest and termite inspections protect you and the USDA from undisclosed property conditions that could be costly down the road. By being proactive and hiring a skilled inspector, you can identify and correct any issues before closing.

While the process adds one more step, take comfort in knowing your new home will be pest-free. Following USDA guidelines helps ensure your loan experience goes smoothly from contract to keys in hand!

USDA Home Inspection Requirements

Since home inspections aren’t technically required, there are no specific USDA inspection requirements to adhere to. Buyers are free to hire any home inspector, and real estate agents can often recommend one or more reputable companies in your area.

Home inspection fees can vary based on the property, where in the country you’re purchasing and more. Buyers may want to compare fees and customer reviews from several home inspectors before making a decision.

Appraisals are typically meant to assess the total value of a property — essentially to ensure it’s worth the loan the lender is offering.

After a lender accepts an application on a USDA eligible property, they must order the appraisal within three days. The appraiser will visit the property in person to:

- Evaluate the value and worth of the home on the current market

- Ensure the property meets all requirements on the Uniform Standards of Professional Appraisal Practice

- Verify it meets state and local building codes

In addition, USDA appraisers evaluate the property to make sure it’s safe, sound and sanitary. Homes need to meet a broad set of Minimum Property Requirements to help ensure homes are move-in ready.

Depending on what the appraiser finds, there may be additional inspections or repairs required. For example, if the appraiser finds signs of termite damage, the lender may require a termite inspection before the loan proceeds. Similarly, signs of water damage could require a mold inspection.

Those kinds of issues may need to be repaired before the loan can close.

The bottom line is that appraisals and inspections are not the same thing. Appraisals are required for a USDA loan, and while home inspections aren’t mandatory, buyers in almost every instance should invest in one.

Check your USDA eligibility with a USDA loan specialist.

Benefits of a Home Inspection

Getting a USDA home inspection provides a buyer with numerous benefits — both short- and long-term. A USDA home inspection can:

- Provide peace of mind – The main goal of the inspection is to identify potential hazards on the property that might pose a safety issue or threaten the health of the buyer or their loved ones.

- Help with negotiations – If issues or repairs are found, the buyer can renegotiate to have the repairs made or the sales price adjusted to account for them.

- A better long-term investment – Buyers can ensure they’re purchasing a home that will hold its value and deliver returns in the long-run.

- Prevent costly repairs and maintenance issues – The inspection can help prevent any hidden issues from cropping up later, posing a financial burden.

2,425 people found a USDA lender in the last 24 hours!

USDA repairs and inspection

FAQ

What disqualifies a home from the USDA financing quiz?

How strict is the USDA appraisal?

Does USDA have a 90 day flip rule?

Is an USDA appraisal different from an FHA appraisal?

Do I need a termite inspection for a USDA loan?

“Termite/pest inspections are not required unless the lender, appraiser, inspector or State law requires the inspection to confirm the property is free of active infestation,” according to the appraisal/inspection guidelines of the USDA.

Does a USDA home loan have a termite problem?

Answer: USDA (like FHA and VA home loans) follows many of the same HUD requirements when it comes to the property condition. Generally speaking – any safety, electrical, plumbing, structural, HVAC, roof, or WDO termite issues will likely need to be corrected before closing.

What happens if a USDA inspection fails?

Sometimes, repairs can be integrated into the loan terms. A failed USDA inspection indicates that the property does not meet specific health, safety, or structural standards set by the USDA. This failure can result from various issues, ranging from significant structural problems to minor, but essential repairs.

Can I apply for USDA Rural Housing If I have a foreclosure?

USDA Rural Housing has other restrictions (set waiting periods) for applicants who have any past bankruptcy, foreclosure, short sales, or other serious financial hardships. Mortgage qualifying requirements have changed dramatically over recent years. Contact us today for the latest USDA approval requirements.