Buying a home is an exciting milestone but it can also be a daunting process especially when it comes to financing. That’s where USDA home loans can help! USDA loans offer 100% financing and low interest rates to help make homeownership affordable for low-to-moderate income buyers in rural areas.

If you’re looking to buy a home in Delaware, USDA loans are a great option to consider. In this comprehensive guide, we’ll cover everything you need to know about getting a USDA home loan in Delaware.

What is a USDA Home Loan?

USDA home loans are government-backed mortgages offered through the US, Department of Agriculture’s Rural Development program They help low-to-moderate income buyers in eligible rural and suburban areas obtain affordable financing,

Some key features of USDA loans

-

100% financing – No down payment is required. Closing costs can also be financed into the loan. This makes it easier to qualify.

-

Low interest rates – USDA loans offer competitive fixed rates, generally lower than conventional loans. The current rate is around 4.875%.

-

Low mortgage insurance – An upfront guarantee fee of 1% of the loan amount is charged and monthly mortgage insurance is 0.35% of the balance.

-

Flexible credit guidelines – Credit scores as low as 640 may qualify. Manual underwriting is available for those who don’t meet automated guidelines.

-

No income limits – Your income just needs to be below the area’s limit to qualify. Limits range from $60,000 to $108,000 depending on location.

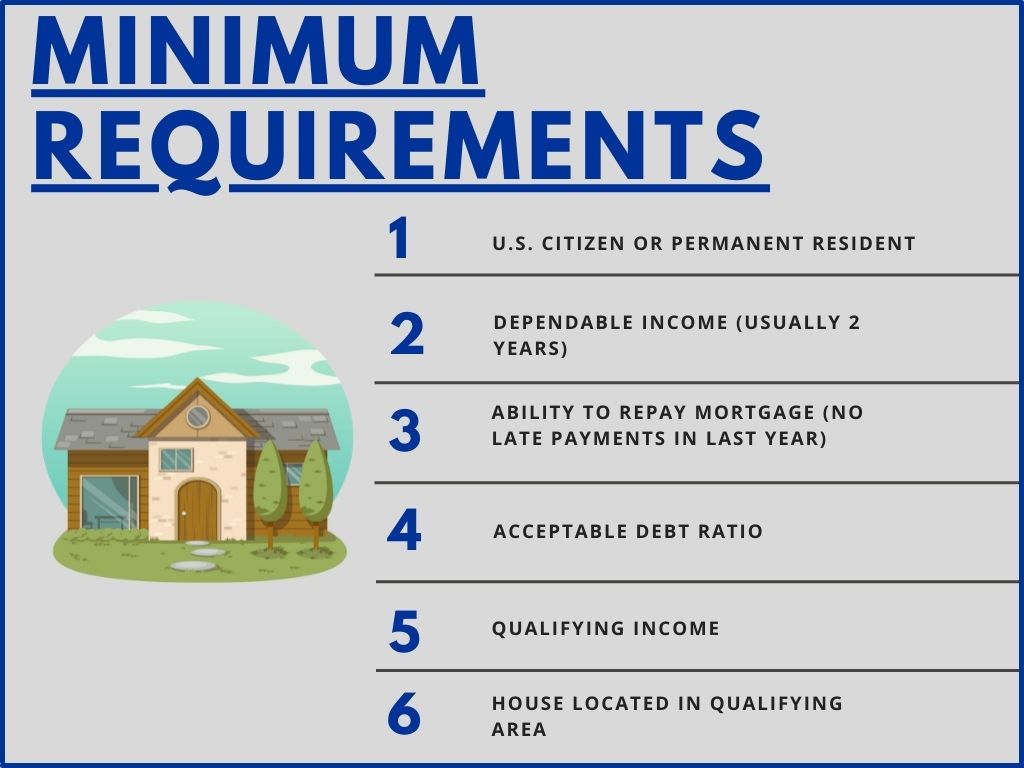

USDA Loan Eligibility in Delaware

To be eligible for a USDA home loan in Delaware, you must meet certain criteria:

Property Location

The home must be located in an eligible rural or suburban area, as designated by the USDA Property Eligibility Site. Generally, cities with populations under 20,000-35,000 qualify. You can check your specific address here.

The entire state of Delaware is eligible, though some cities like Dover, Newark and Wilmington have population limits. Vacation and second homes don’t qualify.

Borrower Criteria

As a borrower, you must:

- Be a U.S. citizen, permanent resident or qualified non-citizen

- Have sufficient and dependable income to repay the loan

- Have a credit score of 640 or higher

- Not have any recent bankruptcy or foreclosure

- Meet debt-to-income limits (typically 29%/41%)

Income limits vary but range from $60,000 to $108,000 for Delaware counties. You can check the limits for your county here.

Property Requirements

The home itself must meet USDA requirements:

- It must be modest in size, design and cost for the area

- Existing homes must be structurally sound; new homes must meet local building codes

- Manufactured homes are eligible if built after June 1976 and meet program guidelines

- 1-4 unit homes qualify; condos and townhomes may also qualify

In Delaware, the maximum loan limit is $420,000. Lower limits apply in some counties.

How to Apply for a USDA Home Loan in Delaware

If you think you may qualify, follow these steps to get started with a USDA home loan in Delaware:

1. Check your eligibility. Make sure the home and your finances meet the criteria above. Use the USDA Property Eligibility Site and Income Limits tool.

2. Find a USDA lender. Work with a lender approved to offer USDA loans. This is required to apply. Local banks, credit unions and online lenders offer them.

3. Choose a property. The lender can give you guidance on maximum purchase price and loan amount you can qualify for.

4. Complete a loan application. You’ll provide documents verifying your income, assets, employment and credit history.

5. Get pre-approved. The lender will process your application and issue a pre-approval letter if approved. This shows sellers you are a qualified buyer.

6. Make an offer. Your real estate agent can help negotiate the purchase contract. Keep in mind, USDA loans require a professional appraisal and home inspection.

7. Finalize loan details. The lender will verify all information and documentation prior to closing. You’ll complete paperwork and sign disclosures.

8. Close on your new home! At closing, you’ll sign the final loan documents and receive the keys.

It’s a good idea to get pre-qualified before starting your home search. This provides an estimate of what you can afford and your likelihood of approval.

The entire process usually takes between 30-60 days from completed application to closing. Having all your financials and paperwork ready to go will help speed things along!

Pros and Cons of USDA Loans in Delaware

USDA home loans offer big benefits, but also have some limitations to be aware of:

Pros

- Low interest rates and low mortgage insurance

- No down payment or minimum cash required

- More flexible credit requirements

- Fixed rate provides stability in monthly payments

- Could finance up to 100% of purchase price plus closing costs

Cons

- Limited to rural/suburban locations only

- Upfront guarantee fee is 1% of the loan amount

- Monthly mortgage insurance payment required

- Home selection limited to modest properties

- Home inspection and appraisal required

- Homeownership education class required

- Potential for payment recapture if you sell in < 5 years

As you weigh the pros and cons, make sure to consider your specific homebuying situation and financial goals. A USDA loan may be an excellent fit if you are looking to buy in a rural area as your primary residence and want to put down minimal cash.

USDA Loan Requirements in Delaware

When applying for a USDA loan, there are some requirements you’ll need to be prepared for. Here are key details:

-

Homebuyer education – You must complete an approved course prior to closing. Many lenders offer classes.

-

Property appraisal – The lender will order an appraisal to ensure the purchase price is supported.

-

Minimum 620 credit score – Guidelines allow 640 and above, but most lenders require 620 minimum.

-

Stable employment history – Two years at the same job or field is recommended. Switching jobs recently could make approval more challenging.

-

Funds to cover closing costs – If closing costs aren’t financed into your loan, you must show funds in your accounts to cover them.

-

Debt-to-income (DTI) limits – Your total monthly debt payments, divided by gross monthly income must be below 29%/41% front-end and back-end ratios.

Being aware of these requirements and having all documentation ready will give your application the best chance for a smooth approval process.

Alternatives to USDA Loans in Delaware

Though they offer great benefits, USDA loans aren’t for everyone. Here are a few alternatives to consider for your Delaware home purchase:

-

FHA loans – Require a 3.5% down payment but offer low rates and more flexible credit like USDA loans.

-

Conventional 97 – Put down just 3% with a conventional loan. Could be an option if in an ineligible USDA area.

-

Down payment assistance – Local programs like DPA provide grants to help cover your down payment. This allows a lower mortgage amount.

-

VA loans – For eligible military members, zero down payment VA loans are an excellent option.

-

Ask lenders about alternative credit mortgages if you don’t meet minimum score requirements. Or take some time to improve your credit before applying.

Be sure to talk to a loan officer about your specific situation to determine the best loan type for you.

USDA Loan Limits for Delaware Counties

The maximum USDA loan amount you can qualify for depends on the county where the home is located. Here are the 2023 loan limits for Delaware:

| County | Limit |

|---|---|

| Kent | $420,000 |

| New Castle | $420,000 |

| Sussex | $420,000 |

Depending on your finances and the purchase price, your loan amount may be lower than the county limit. The lender will determine the maximum you qualify for based on your credit, debt, and repayment ability.

USDA Income Limits for Delaware Counties

In addition to loan limits, annual income caps apply based on family size and county. Here are the 2022 income limits for Delaware US

What are the Delaware USDA Rural Housing Income Guidelines for 2023?

The income limits for Delaware USDA Rural Housing loans are based on the number of people in the house and the county that the property is located. The Delaware USDA Loans Income Limits for 2023 are as follows:

New Castle County Maximum Income Limits for 2023

1 -4 Person 5-8 Person

$0 – $128,350 $0 – $169,400

Kent County & Sussex County Maximum Income Limits for 2023

1 – 4 Person 5 – 8 Person

$0 – $110,650 $0 – $146,050

Property Eligibility Update for June 4, 2018

USDA updated its eligible property areas for a Delaware USDA loan and Middletown, Delaware is no longer eligible as of June 4, 2018. Below is map showing the Middletown Delaware area with the new updated areas. The areas in Orange is no longer eligible for a USDA financing as of June 4, 2018.

Pros and Cons of a USDA Loan | All You Need to Know About USDA Home Loans EXPLAINED

FAQ

Can you get an USDA loan in Delaware?

Is it easier to get FHA or USDA?

What is the debt to income limit for USDA loan?

What does your credit score need to be for a USDA loan?

What is a USDA Rural home loan in Delaware?

Delaware USDA Rural Housing Loans 100% Financing – No Down Payment Loans! Delaware USDA Guaranteed Rural Development Home Mortgage Loanis a flexible no down paymentgovernment insured mortgage loan program that is growing in popularity for rural areas of Delaware.

Can you get a USDA home loan in Delaware?

A common misconception about the USDA home loan program is that it’s for farmers, but this mortgage loan is for those who want to purchase a primary residence outside the urban areas. In Delaware you will find that many suburban areas qualify for this program as well such as Smyrna, Delaware. Benefits of USDA Home Loan 100% Financing:

How do I get a USDA mortgage in Delaware?

Need a USDA Mortgage Lender Delaware – Call the John Thomas Team at 302-703-0727to apply for a Delaware USDA Rural Housing Loan or send an e-mail to [email protected] APPLY ONLINE NOW!! Primary Residential Mortgage, Inc. 248 E Chestnut Hill Rd, Newark, DE 19713 #DelawareUSDARuralHousingLoans #USDALoans #DelawareUSDALoans #USDAHomeLoans

How much does a USDA mortgage guarantee cost?

USDA Rural Housing Loans require that borrowers pay a upfront mortgage guarantee fee that as of June 2017 is 1% of the loan amount but USDA lets you finance this upfront fee into the loan.