At Dash Home Loans, we make the mortgage financing process quick, painless, and (dare we say?) enjoyable. If you’re looking for a no-money-down loan option with a competitive APR, our expert Mortgage Coaches can determine your Florida USDA1 loan eligibility.

Buying a home in Florida can be expensive but USDA home loans offer an affordable financing option for rural homebuyers. These government-backed loans have favorable terms and flexible credit requirements.

In this comprehensive guide. we’ll cover everything you need to know about USDA home loan requirements in Florida including

What Are USDA Loans?

USDA home loans, also known as Section 502 loans, are mortgage loans insured by the U.S Department of Agriculture (USDA) They help low- and moderate-income buyers purchase homes in eligible rural and suburban areas.

USDA loans offer:

- 100% financing – no down payment required

- Below-market interest rates

- Flexible credit guidelines

Borrowers can use USDA loans to build, repair, renovate or relocate a home. Funds may also be used to purchase and prepare the site, including installing water and sewage facilities.

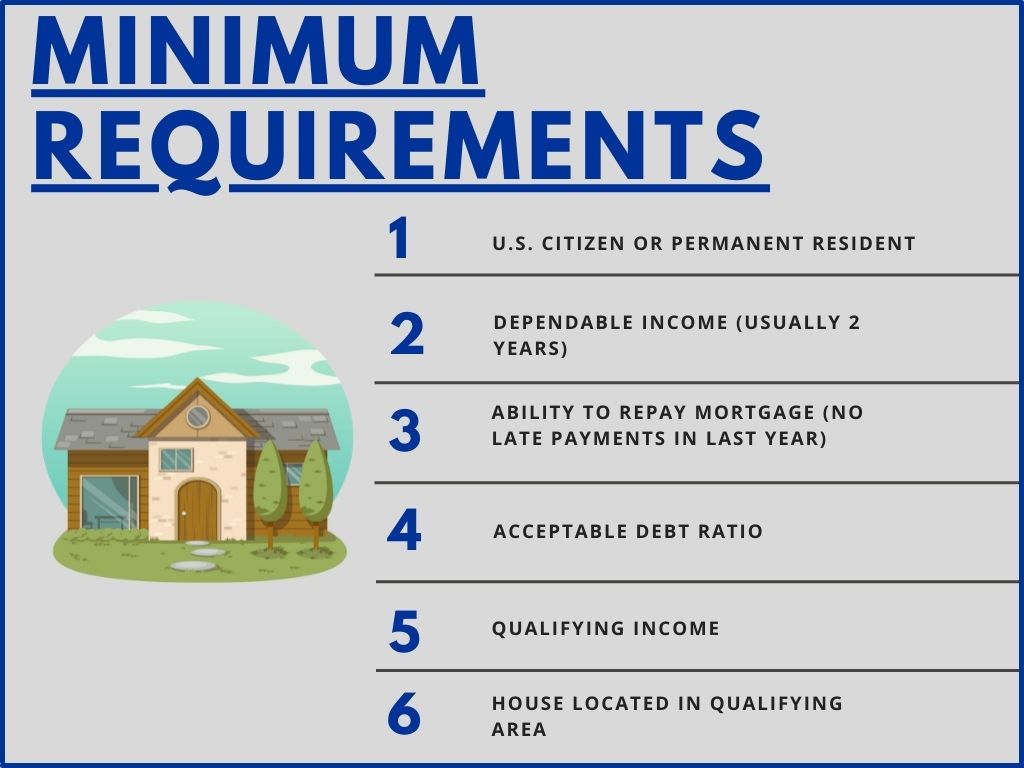

USDA Loan Requirements in Florida

To qualify for a USDA loan in Florida, borrowers must meet certain eligibility criteria:

Income Limits

Your household income must be below the applicable income limit for your area. Income limits vary by county and household size. You can check income eligibility using USDA’s income eligibility tool.

In 2023, income limits range from $64,900 (1-person household) to $113,300 (8-person household) in most Florida counties. The limits are higher in high-cost areas like Miami-Dade and Monroe counties.

Credit Requirements

USDA has flexible credit standards designed to help low-income borrowers. Minimum credit scores are not published, but many lenders require a score of 640 or higher.

You can qualify with a lower score by demonstrating extenuating circumstances for issues like medical debt or a lack of credit history. Limited traditional credit is acceptable if you have a strong history of paying utilities and rent on time.

Home Location

The home must be located in a USDA-designated rural or suburban area. Over 80% of Florida land area qualifies. You can verify eligibility by address using USDA’s Property Eligibility Site.

Properties in cities like Jacksonville, Tampa, Orlando, Miami and Fort Lauderdale qualify in certain neighborhoods. Subdivisions on the outskirts of town are often eligible.

Home Types

You can use a USDA loan to purchase an existing home, build a new home, or buy and rehabilitate a fixer-upper. Condos and townhomes are also eligible in some cases.

Manufactured and modular homes are eligible if they meet USDA’s construction and site standards.

The home must be modest, not overtly luxurious or designed for commercial use. It also must meet state and local building codes.

First-Time Homebuyer

USDA does not require first-time homebuyer status, so the program is open to repeat buyers too.

Homeownership Education

First-time buyers must complete a homebuyer education course to qualify. Many lenders and housing nonprofits offer online and in-person classes.

Occupancy and Property Requirements

You must occupy the home as your primary residence and maintain it as your permanent home. Non-occupant co-borrowers are not permitted.

The value of the home must be within USDA’s mortgage limits for the area:

- $381,900 for most Florida counties

- $726,525 in Monroe county

Seller Contributions

The seller can pay allowable closing costs and prepaids up to 6% of the home’s sale price. This helps buyers afford upfront expenses. Common examples are origination fees, appraisal fees, recording fees, prepaid taxes and insurance.

Repayment Ability

Lenders will evaluate your credit, assets, debts and income to ensure you can repay the loan. Factors like your expected property taxes, insurance, HOA fees and other obligations are considered.

Stable income from documented sources is required. Nontaxable income such as disability and Social Security benefits may be considered.

How to Apply for a USDA Home Loan in Florida

Follow these key steps to get a USDA-backed mortgage:

-

Check eligibility. Make sure you meet the income limits and locational requirements using USDA’s online tools.

-

Get pre-qualified. Work with a USDA-approved lender to get pre-qualified. This involves submitting financial documents so they can estimate your borrowing power.

-

Find a home. Once pre-qualified, you can confidently start home shopping within your approved price range.

-

Make an offer. When you find the right home, make an offer contingent on financing and appraisal.

-

Complete the full application. Your lender will guide you through documenting income, assets, debts, and more to underwrite your loan.

-

Close on time. Finalize the purchase after the home appraises for the purchase price and your loan is approved.

It’s wise to get pre-qualified early and start the process at least 3-4 months before your desired closing date. Rates lock after loan approval, protecting you from rate hikes.

USDA Loan Rates and Terms

Here are some key details on current USDA mortgage rates and terms in Florida:

- Interest rates – Fixed at around 4.875% as of July 2024

- Loan term – 30 years is standard; 33 or 38 years may be available

- Mortgage limits – Vary by county from $381,900 to $726,525

- Downpayment – None required

- Closing costs – Can be financed into loan amount

- Monthly mortgage insurance – 1% of loan amount

Borrowers who receive direct payment assistance from USDA may qualify for a reduced interest rate around 1%.

Pros and Cons of USDA Loans

USDA home loans offer many perks, but there are also some potential drawbacks to consider:

Pros

- No downpayment required

- Below-market interest rates

- Flexible credit requirements

- Low monthly mortgage insurance

- Fixed monthly payments

- Can finance closing costs

Cons

- Limited mostly to rural/suburban areas

- Upfront mortgage insurance fee

- Monthly mortgage insurance for full loan term

- Strict income and home eligibility rules

- Limited inventory of eligible existing homes

- Manual underwriting takes more time

Make sure to weigh the pros and cons before applying. While USDA loans are extremely affordable, they aren’t right for every homebuyer.

Alternatives to USDA Loans

If you don’t qualify for a USDA loan, here are a few alternative home financing programs to consider:

- Conventional 97 – 3% downpayment with flexible credit criteria

- FHA loan – 3.5% down with lenient guidelines

- VA loan – No downpayment option for veterans

- Florida Assist – Downpayment and closing cost help from Florida Housing Corp

- Community seconds – Piggyback loan with downpayment funds from nonprofits

Shopping lenders and mortgage programs is wise to find your best fit. Your loan officer can help you compare options for your situation.

The Bottom Line

USDA home loans are an excellent financing solution for eligible borrowers in rural Florida. Their hallmarks of no downpayment, low rates, and flexible credit help first-time buyers and low-income families achieve homeownership.

If you’re purchasing in an eligible area, starting the pre-approval process is the best way to determine if a USDA loan is right for you. Pay close attention to the specific income, credit, and property requirements to ensure you qualify.

Frequency of Entities:

usda: 24

florida: 17

home: 16

loan: 16

loans: 7

mortgage: 6

requirements: 5

income: 5

credit: 5

rural: 4

eligible: 4

buyers: 3

areas: 3

location: 2

limits: 2

interest: 2

payments: 2

downpayment: 2

applicants: 2

lenders: 2

homebuyers: 2

closing: 2

costs: 2

USDA vs. FHA Loans

Both USDA and FHA loans are designed to make homeownership more affordable and achievable for low- to moderate-income families. Since both are backed by a government agency (FHA loans are guaranteed by the Federal Housing Administration), lenders can offer competitive rates to borrowers with less-than-perfect credit. But what’s the difference between the two mortgage options and which is best for your family?

Unlike USDA loans, which require no money down, FHA loans require 3.5% down for applicants with a credit score of 580 and higher. Applicants with a shaky credit history are often required to dish out even more money – about 10% of the total loan amount. Fortunately, borrowers can have a slightly higher debt-to-income ratio than those applying for a USDA loan.

FHA loans are more lenient in other ways too. Whereas the U.S. Department of Agriculture has both income and geographical restrictions, the Federal Housing Administration doesn’t have specific salary parameters. You’re also free to buy a house wherever you like.

Learn more about FHA loans in Florida.

Florida USDA Loan Requirements

USDA loan requirements are fairly consistent across the country. To qualify for a USDA loan in Florida, you must meet the following criteria:

- Income Limits: You cannot make more than 115% of your area’s median income.

- United States Citizenship: Only permanent residents can apply for a USDA loan.

- Mortgage Insurance: USDA loans require mortgage insurance.

- Primary Residence in a Rural Area: The home must be located in an area with less than 20,000 people. It must also be your primary residence, not a vacation home or investment property in Florida.

If you meet these requirements, a USDA loan could be the right home financing tool for you. But if you make a little too much cash or are hoping to flip a fixer-upper, explore Dash’s other lending options. You’re sure to find something that suits your needs.

Florida USDA Mortgage Qualifying & Application Process

What are the requirements for a single family home loan?

The property must be in an eligible rural area, and borrowers must meet household income requirements that vary by location and household size. The USDA offers the Single Family Housing Direct Loan through the Section 502 Direct Loan Program to help low-income families buy, build, or fix up small homes in rural areas.

How do I qualify for a USDA loan?

– The home you intend to purchase must be located in an eligible rural area as defined by the USDA. 2.**Residency and Citizenship**: – You must be a **U.S. citizen**, a **permanent resident**, or an

How does the USDA finance a home loan?

The USDA provides funding for direct loans, which have favorable terms like low interest rates (as low as 1% with payment assistance) and long repayment periods (up to 38 years for eligible applicants). Income, creditworthiness, and the property’s location in an eligible rural area all affect eligibility.

How do USDA loans work in Florida?

USDA loans in Florida count the entire HOUSEHOLD’S income when determining if you’re eligible. The household’s income must be below the area median as defined by the tables below. So even if a person isn’t on the loan, the lender must verify that person’s income and include it towards the USDA income limits in Florida. Debt-to-Income Ratio