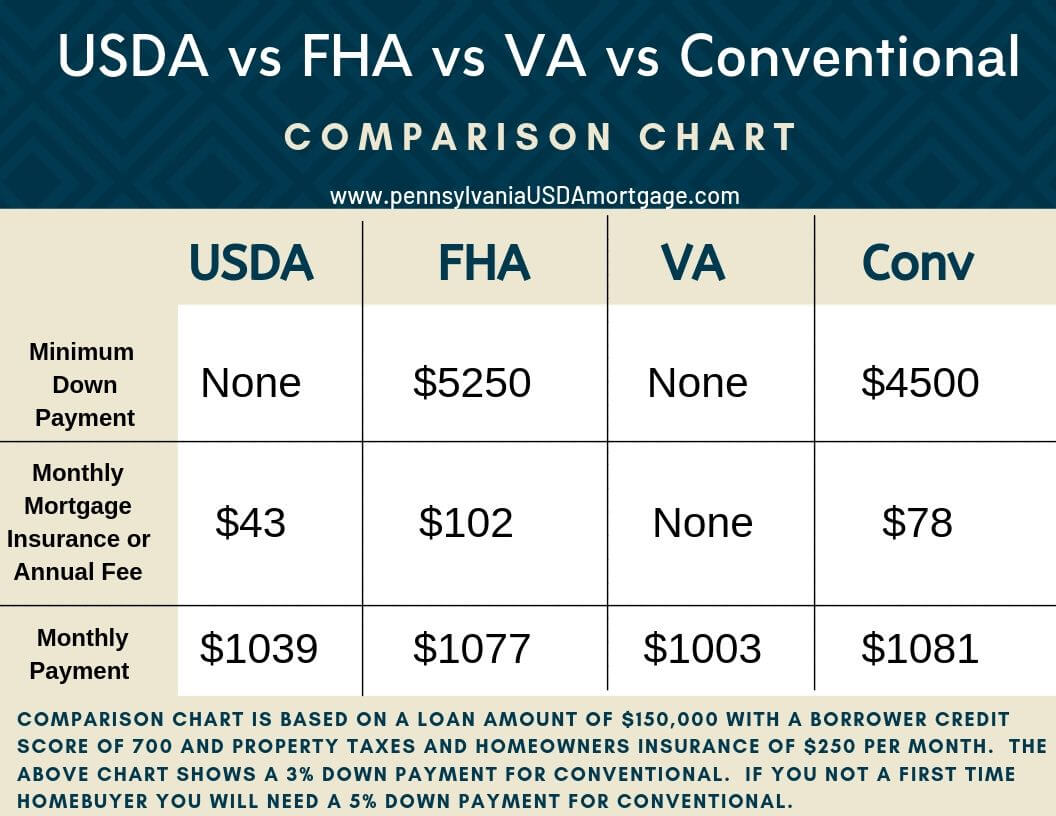

Buying a home is an exciting milestone but it also involves a lot of number crunching. As a potential homebuyer you need to figure out the full monthly costs – not just the mortgage principal and interest. Expenses like property taxes, home insurance, mortgage insurance and HOA fees all factor into your payment. This is where using a usda home loan calculator with taxes comes in handy.

I’ve purchased a home with a USDA loan before, so I know firsthand how confusing it can be to calculate everything. USDA loans have special features like guarantee fees and annual mortgage insurance that other loans don’t have. That’s why I recommend using a specialized USDA mortgage calculator that can factor in all the unique costs.

In this article, I’ll walk through the key facts about USDA loans, the additional fees to account for, and how to use an online USDA mortgage calculator with taxes to estimate your total monthly payment.

What Are USDA Loans?

USDA stands for the United States Department of Agriculture. The USDA runs a loan program to promote homeownership in rural areas These loans help lower income borrowers who may not qualify for a traditional mortgage

Some key advantages of USDA loans include

- 100% financing available – no down payment required

- More flexible credit score requirements

- Low fixed interest rates

- No prepayment penalties

Borrowers must meet income limits and purchase a home in an eligible rural area. The home size must be modest – under 2,000 sq ft. USDA loans require an upfront guarantee fee and annual mortgage insurance premium.

Now let’s look at how to calculate a USDA loan payment with all the costs included…

Factors That Impact Your USDA Mortgage Payment

As a first-time homebuyer using a USDA loan, I had to get familiar with terms like PITI, MIP and more. Here are the key components that factor into your monthly mortgage payment:

- Principal – The amount borrowed for the home loan

- Interest – The rate charged on the loan amount

- Taxes – Local property taxes on the home

- Insurance – Homeowners insurance premium

- Mortgage insurance – Also called a guarantee fee on USDA loans

- HOA fees – If the property is part of a homeowner’s association

The principal and interest make up your basic mortgage payment, also called P&I. But taxes, insurance and other costs get added on top to determine the total monthly payment.

USDA loans also have upfront and annual fees:

- Upfront guarantee fee – 1% of the loan amount

- Annual guarantee fee – 0.35% of the loan balance

The upfront fee gets rolled into the loan amount. The annual fee gets bundled into the monthly mortgage insurance or MIP payment.

Now let’s go over how to use an online calculator to add up all these pieces…

How To Use a USDA Mortgage Calculator With Taxes

Using an online USDA mortgage calculator makes it easy to estimate your monthly payment. Here are step-by-step instructions:

-

Visit a mortgage calculator website and select the USDA loan option. I recommend starting with MortgageCalculator.org.

-

Enter the purchase price of the home you want to buy.

-

Input your down payment amount – for USDA loans this is often $0.

-

The calculator will determine your loan amount based on the price minus down payment.

-

Enter your estimated interest rate, loan term, home insurance and property tax amounts.

-

For mortgage insurance, input the upfront and annual guarantee fees charged on USDA loans.

-

Check the box if you want the upfront fee rolled into the loan.

-

Enter any additional monthly fees like HOA dues.

-

Tap the Calculate button to see your monthly principal & interest, as well as your total payment including taxes and insurance.

-

Use the print or download buttons to save your full amortization schedule.

Let’s look at a quick example…

For a $200,000 home with 0% down and a 3.5% interest rate, here are the numbers:

- Principal & Interest = $843

- Property Taxes = $250

- Home Insurance = $100

- Mortgage Insurance = $58

- Total Payment = $1,251

As you can see, the principal and interest are just a portion of the total payment. Using the USDA mortgage calculator ensures you factor in all the costs accurately.

Key Takeaways

-

USDA loans help make homeownership affordable for lower income borrowers in rural locations.

-

Take advantage of online USDA mortgage calculators to estimate your total monthly payment including taxes, insurance and fees.

-

Input the loan amount, interest rate, tax and insurance estimates to calculate the principal & interest.

-

Don’t forget to include the upfront guarantee fee and annual mortgage insurance costs specific to USDA loans.

-

Use the full amortization schedule from the calculator to understand how your payment changes over the loan term.

Knowing your complete monthly mortgage payment will help you budget and determine how much house you can afford. I recommend trying a few different home prices and down payments to find the payment you’re comfortable with.

The bottom line is that an online USDA mortgage calculator with taxes saves you time and effort. Within minutes, you can calculate your monthly home loan payment and preview your amortization schedule. Give it a try today before you start applying for USDA loans or making offers on homes.

Choose Property in a USDA Rural Area

As a main requirement, you can only select homes in qualified USDA rural areas. The USDA generally defines rural areas as towns, communities, or small cities occupied by less than 20,000 people. But in other instances, they may approve locations with up to 35,000 residents. These places should not be located in a metropolitan statistical area (MSA) and must lack mortgage credit for low to average income households. Urban areas, meanwhile, are usually defined as places with a population of 50,000 or more.

In 2015, the USDA announced updated guidelines for what they consider as rural areas. This update made it more challenging to get approved for a USDA loan, especially since populations have grown substantially since the prior categorization. Prior to 2015, over 90% of property in the U.S. qualified for USDA financing.

Though these guidelines may seem too restrictive, extended parts of metro areas in small cities and towns may be eligible. To verify if your area qualifies for a USDA loan, you can check interactive maps on the USDA website. You simply type in the address and it will indicate if the location is eligible or not.

To obtain a USDA loan, you must fall under the required income limit for moderate income. Moderate income is defined as the greater of

- 115% of the U.S median family income,

- 115% of the state-wide and state non-metro median family incomes, or

- 115/80ths of the area low-income limit.

Limits are based on both the local market conditions and the size of a family. Household income is calculated by adding the loan applicant’s income plus the income of other family members in a home. This rule applies even if the household member does not share the same family name.

The moderate income guarantee loan limit is the same in any given area for households of 1 to 4 people, and is set to another level for homes of 5 to 8 people. The following table lists examples of limits from a few select areas in the country:

| Location | 1 to 4 Person Limit | 5 to 8 Person Limit |

|---|---|---|

| Fort Smith, AR-OK MSA | $110,650 | $146,050 |

| Northwest Arctic Borough, AK – with a road system (115%) | $124,300 | $164,100 |

| Northwest Arctic Borough, AK – without a road system (150%) | $192,850 | $254,550 |

| Oakland-Fremont, CA HUD Metro | $161,200 | $212,800 |

| San Francisco, CA HUD Metro | $238,200 | $314,400 |

The floor values on the above limits are $110,650 and $146,050, respectively. Homes with more than 8 people in them can add 8% for each additional member. You can verify income limits in your local area by checking the USDA income limits page, or you can use the eligibility checker to enter your personal details.

For example, let’s say the income limit in your area for a 1-4 person household is $110,650 per year. That means you can qualify for a USDA loan with an annual income of $110,650 or less. 15% of $96,200 is equivalent to $14,450, which we added to $96,200 to obtain the $110,650 income limit.

What if I can pay 20% down? Generally, if you can afford to make a 20% down payment on top of your mortgage, you won’t qualify for a USDA loan. If you have assets that exceed the imposed income limits, you likely won’t be approved. But in some cases, a USDA-sponsored lender may approve your loan and require you to make a down payment.

Loan Amount Limits

Loans can be used for regular, manufactured, or modular homes which are no more than 2,000 square feet in size. As of 2023 the effective loan limit starts at $377,600 in low-cost areas and goes as high as $871,400 in expensive (or high-cost areas) in states like California. You can view loan amount limits in your local area here.

As for credit requirements, USDA lenders prefer a FICO credit score of 640. This is the minimum credit score required to qualify for the USDA’s automated writing system. Homebuyers who satisfy this requirement receive streamlined processing of their application. Meanwhile, borrowers with credit scores below 640 (some lend as low as 620) must submit to a manual underwriting process. If you have further credit issues on your record, your application will take longer to approve.

Conventional loan lenders, on the other hand, usually prefer borrowers with a credit score of 680 and above. If you have limited income and an average credit score, consider taking a USDA loan. Again, homebuyers who cannot qualify for a traditional conventional mortgage may be eligible for a USDA home financing.

Improve Your Credit Score

Before applying for any loan, make sure to check your credit report. Borrowers can request for a free copy at AnnualCreditReport.com. Avoiding late payments and reducing your outstanding debts helps improve your credit score. In the long run, having a good credit profile will help you obtain more favorable loan deals in the future.

Like other types of mortgages, borrowers must also meet the required debt-to-income ratio (DTI) to obtain a USDA loan. DTI is a risk indicator which measures the sum of your total monthly debts compared to your gross monthly income.

- Front-end DTI ratio – The front-end DTI limit for USDA loans should not exceed 29%. This is the percentage of your income that pays for all housing-related expenses. It includes monthly mortgage payments, property taxes, homeowners insurance, etc.

- Back-end DTI ratio – The back-end DTI limit for USDA loans should not exceed 41%. This is the percentage of your earnings that pay for your housing-related costs together with your other debts. It includes your car loan, credits cards, student loans, etc.

A low DTI ratio shows you have a good balance of income and debt. This lowers default risk for lenders, which increases your chances of loan approval. On the other hand, a high DTI ratio indicates you cannot take on further debt. DTI requirements for USDA loans are quite similar to conventional mortgages. For conventional loans, the front end-DTI limit is 28%, while the back-end DTI is 43%, but this can be as high as 50% if you have compensating factors.

Current Local Mortgage Rates

Here is a table listing current Denver mortgage rates.

The following table shows current 30-year mortgage rates available in Denver. You can use the menus to select other loan durations, alter the loan amount, or change your location.

USDA Mortgage Calculator: Here’s how to CORRECTLY calculate a USDA monthly payment

What is a USDA loan calculator?

Our USDA loan calculator helps you estimate your monthly mortgage payments, including taxes and insurance, to give you a better idea of what to expect when financing your home purchase using the USDA loan program.

What is a USDA payment calculator?

A **USDA payment calculator** is a tool that helps you estimate your monthly payments for a USDA mortgage.It takes into account factors such as your estimated home price, down payment, loan term, and interest

How does the USDA mortgage calculator work?

The USDA mortgage calculator is easy to use with breakdowns of every payment shown in the mortgage amortization schedule with monthly and biweekly payment options. The USDA PMI calculator also offers extra payment options that show you how much faster you can pay off the mortgage if you are making regular extra payments.

What is a USDA mortgage & closing cost calculator?

This USDA mortgage and closing cost calculator will estimate the loan amount for eligible home buyers, including the USDA funding fee, and the monthly loan payment; including real estate taxes, home insurance, and monthly mortgage insurance (also called PMI).