There is a good and a bad credit score range. Fortunately, a 680 FICO Score falls under the good credit score category. So, if you want to buy a house, it can put you at a great advantage so you can get a mortgage.

The kind of home loan you will get will absolutely depend on your personal needs and background. For example, if you are a service member, there’s a terrific job benefit you might want to avail yourself of. You might also be looking to move out into the country where you might feel safer and where there’s generally more space. With the COVID-19 pandemic still raging, many people have been trying hard to move out of the big cities. More than the credit score you have, circumstances such as these can dictate what mortgage you will eventually avail.

Having a credit score of 680 can make getting a mortgage loan trickier, but certainly not impossible. In this comprehensive guide, we’ll break down everything you need to know about getting a home loan with a 680 credit score.

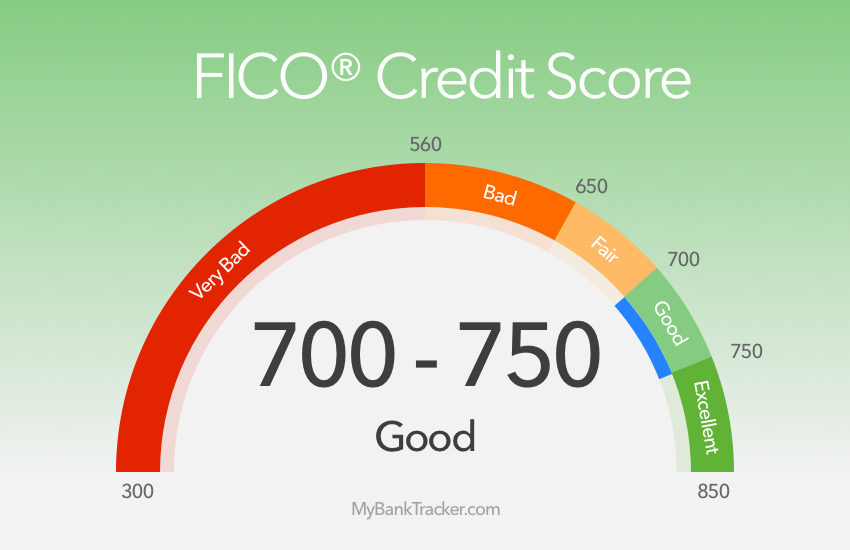

What is Considered a Good Credit Score for a Mortgage?

Before diving into the specifics of a 680 credit score, let’s first establish a benchmark for what is considered a “good” credit score when applying for a mortgage.

- 800+: Excellent

- 740-799: Very Good

- 670-739: Good

- 580-669: Fair

- 500-579: Poor

So at 680, a credit score falls into the “good” range, but it’s on the lower end. This means borrowers can still qualify for mortgages, but may not get the very best terms or lowest interest rates.

Is a 680 Credit Score Good Enough to Get a Mortgage?

The short answer – yes, a 680 credit score is generally good enough qualify for a mortgage, particularly government-backed loans like FHA, VA, and USDA loans which have lower credit requirements

However, borrowers with a 680 score will likely pay a higher interest rate and have fewer loan programs available compared to someone with a 700+ score

According to credit scoring agency FICO, 96% of mortgage lenders will approve borrowers with a minimum credit score of 680. So while it may take some extra work to find the right lender, a 680 credit score is still high enough for mortgage approval.

What Types of Mortgages Can You Get with a 680 Credit Score?

While a 680 credit score won’t unlock the lowest rates or every mortgage program, there are still several good loan options available including:

Conventional 97% LTV Loans

- Minimum 620 credit score

- 3% down payment

- PMI required

FHA Loans

- Minimum 500 credit score

- 3.5% down payment

- Upfront and monthly MIP

VA Loans

- Minimum 620 credit score

- No down payment required

- No monthly mortgage insurance

USDA Loans

- Minimum 640 credit score

- No down payment required

- Low monthly mortgage insurance

Of these, FHA loans will likely offer the most favorable terms for borrowers right around a 680 score. VA and USDA loans can also be great options if the borrower meets eligibility requirements.

Conventional loans are harder to get approved for with poorer credit, but a 680 score may still qualify depending on other factors like income, assets and debts.

How Do Mortgage Rates Compare with Different Credit Scores?

While a 680 credit score meets the minimum requirements for most mortgages, it won’t get you the lowest advertised rates you see online or in other marketing materials.

Prime borrowers with scores above 720 and 20% down payments get access to the very best rates. As credit scores go down, interest rates and fees go up.

For example, on a $300,000 30-year fixed-rate mortgage, here’s how rates and monthly payments might compare among different credit scores:

- 760+ credit score: 2.67% interest rate, $1,213 monthly payment

- 700-759 credit score: 2.89% interest rate, $1,248 monthly payment

- 680-699 credit score: 3.07% interest rate, $1,277 monthly payment

- 660-679 credit score: 3.28% interest rate, $1,312 monthly payment

As you can see, the borrower with a 680 credit score has a monthly payment that is $64 higher compared to someone with a 760 score. That equates to $768 more in mortgage interest paid every year, and over $23,000 extra over the life of a 30-year loan.

This demonstrates why it’s critical to get your score as high as possible before applying for a mortgage. Even minor differences can cost thousands long-term.

How to Improve Your Credit Score to Get a Better Mortgage Rate

If your credit score is currently 680 and you have time before buying a home, take steps to increase your score and get better mortgage rates. Here are some tips:

- Pay down debts and get current on any late payments

- Lower your credit utilization ratio

- Avoid new credit inquiries

- Become an authorized user on someone else’s account

- Correct any errors on your credit reports

Shopping mortgage lenders with a 680 credit score is also key. While one lender may turn you down or charge high rates, another may still approve you for a competitive loan program. Cast a wide net and apply with several lenders to increase your chances.

Alternatives if a 680 Credit Score is Too Low for Mortgage Approval

If your credit score is lower than 680, you may need to consider alternate options beyond a traditional mortgage:

FHA Loan with 10% Down: FHA allows credit scores as low as 500 with a 10% down payment.

VA or USDA Loan: No minimum credit score if you meet other eligibility criteria. Can be a great option for service members, veterans, or low-income borrowers in rural areas.

Apply with a Co-Borrower: Add someone with better credit to complement your application.

Consider Renting First: Take more time to improve your credit before trying to buy.

Explore Down Payment Assistance: Local and state programs provide grants and loans to cover down payments and closing costs.

Federal Housing Administration (FHA) 203(k) Loan: Special renovation mortgage allows you to wrap purchase + renovations into one loan.

When Credit Score is Less Important for Mortgage Approval

In some scenarios, your credit score carries less weight in the mortgage approval process:

Making a Large Down Payment: A down payment of 20% or more makes your loan less risky for lenders.

Buying Investment Property: Credit standards may be looser since the home isn’t your primary residence.

Working with Smaller Lenders: Local banks/credit unions may be more flexible than national lenders.

VA & USDA Loans: Government-backed loans with no down payment required are less credit dependent.

What Else Matters for Mortgage Approval Besides Credit Score?

While your credit score is important, lenders also closely evaluate these other factors:

- Debt-to-Income (DTI) Ratio

- Employment History & Income

- Down Payment Size & Cash Reserves

- Loan-to-Value (LTV) Ratio

- Overall Credit Report

A higher credit score can compensate for weaknesses in other areas. But if you have blemishes across multiple categories, your loan application will have a harder time getting approved, even with decent credit.

A credit score of 680 puts mortgage approval well within reach. While you may not qualify for rock bottom interest rates, there are plenty of loan programs like FHA and VA that can work for borrowers with credit scores in the high 600s.

The keys are researching multiple lenders, maximizing your down payment if possible, and taking steps to continue boosting your credit. With the right strategy, you can still achieve homeownership, even starting with less-than-perfect credit.

Minimum Credit Score for Mortgages

This year started with some of the lowest mortgage rates we have ever seen, and this is due to the pandemic. The Fed lowered rates to boost the economy, and this has enticed a lot more people to start applying for mortgages. Add this to the fact that people are just looking for more space and are probably getting sick of the limited territory they’ve been keeping into since the pandemic started. So you might understand how hot the housing market has become.

All that said, it’s an excellent thing that the USDA loan program exists. This is a home loan guaranteed by the U.S. Department of Agriculture, and there’s no minimum FICO score required. There’s also no minimum down payment and no mortgage insurance. So the USDA loan is ideal for people who want to move into a more isolated area as they ride this pandemic out.

Because there is no particular credit score needed, though, there are many things that can disqualify potential borrowers. For example, depending on your preferred location, there are household income caps, and there is such a thing as having too much money despite needing to take out a loan. Most importantly, you have to buy a house in a rural area to get approved.

This type of mortgage aims to hit two birds with one stone by stimulating rural economies and helping disadvantaged Americans get closer to homeownership.

The housing market is an essential part of the national economy as a whole, and it’s not just about the mortgages. Think of what usually happens after someone purchases a home. After you buy a house, you will want to furnish it, and maybe you’ll work on home improvement and need all kinds of stuff. So it is necessary to keep our housing market healthy because it supports so many other industries.

To help people become homeowners, the government has this loan program that encourages first-time homebuyers to take on mortgages. The Federal Housing Administration ensures this. It is not, however, specific to first-time home buyers. Remember, what’s important to the government is that more people eventually buy homes, and to ensure this, the minimum credit score needed to apply for an FHA loan is just 500. That’s about the minimum starting FICO Score of 99% of American consumers. Only 1% of potential borrowers cannot be approved for this program, and these are really exceptional cases.

A 500 FICO Score, however, is not enough. You will need at least 10% for a down payment if your score is lower than 580. Now, if your score is 580 or higher, you can put down as little as 3.5 percent. It’s a great deal, considering how many first-time homebuyers will most likely have less than stellar credit scores.

Since you have a 680 credit score, you might actually be disinterested in this kind of offer, and we’ll tell you why. First, FHA loans charge for mortgage insurance, which is unsurprising since most people who’ll apply probably have poor credit. Mortgage insurance is also charged for other types of loans, but what makes FHA loans all the less enticing is how the mortgage insurance stays for the whole life of the loan. However cheaper the insurance rate can be, that’s nothing to sneeze at if you’ll be paying for it for 30 years.

Let’s see if the alternative will sound better for you.

So what could be the ideal loan to get with a 680 credit score? This is one of the two loan options that you may want to consider.

Conventional loans are the exact opposite of government-backed loans. For examples of government-backed, we’ve already mentioned USDA and FHA loans. Conventional loans are your more traditional mortgages, regulated by Fannie Mae and Freddie Mac, which are the institutions that set the loan limits for these home loans.

To qualify for this type, you need a credit score of at least 620. With a 680 credit score, you’re already in a better than safe range to get approved.

With a traditional mortgage, you can even put as little as 3% down, and you can apply for a higher loan amount the higher your credit score gets. What makes this type of loan a lot more preferable than FHA loans, though, is that the mortgage insurance goes away once you get at least 22% home equity. You can even skip it entirely if you have enough money for a 20% down payment.

Last but definitely not least, we have VA loans, which the Department of Veterans Affairs guarantees. Even if you already have a 680 credit score, you can still get disqualified for a VA loan if you are not a service member or eligible spouse as defined by the VA. To qualify for a VA loan, you need a minimum credit score of 640.

We still mention this loan option because this is arguably the best you can get in the current climate.

VA loans feature some of the best mortgage benefits without the usual disadvantages. You can get a house anywhere in the country, and you don’t even have to put any money down. You also don’t have to pay for mortgage insurance, although a small VA funding fee will be charged to you at closing. Finally, VA loans have some of the best interest rates in the industry, so what is there not to like?

If you are in the right profession, this is really the best mortgage option for you.

The Right FICO Score

Since you are applying for a mortgage, you might also want to ensure that you are using the right FICO Score. When you apply, mortgage lenders will get your credit report from the three big bureaus: Equifax, Experian, and TransUnion. All of these three companies can actually show different scores under your name. To get the credit score that they need for your application, mortgage lenders don’t get the average of your three scores. They also don’t use the highest. Instead, they use the middle value of the three.

Another thing that you have to consider is if you’re buying a house with a partner. If another person’s name is written on the mortgage, you have to know the FICO Score of the person buying the house with you. The mortgage lender will use the lower FICO Score between yours and this person for your application. And remember, for each one of you, they will be getting three credit reports to get the middle score value for your personal accounts.

Mortgage costs increase for credit scores over 680?!

FAQ

Can I get approved for a mortgage with a 680 credit score?

How much loan can I get with a 680 credit score?

Is 688 a good credit score to buy a house?

What credit score do you need for a 250k mortgage?

Is 680 a good credit score for a mortgage?

So when mortgage lenders are looking at a 680 credit score, they’ll typically see it as good enough to qualify you for a loan — but not high enough to offer lower interest rates. That means it’s extra important to shop around with a few different lenders before deciding on a mortgage loan.

Which credit score is best for a mortgage?

Here’s what you need to know: 1.**Conventional Loans**: – **Best Credit Score**: For optimal terms, aim for a credit score in the **high 600s and 700s**.Anything higher is considered “exceptional”

Can you get a car loan with a 680 credit score?

By improving your credit score, you can get average interest rates as low as 4.75% for a new car or 5.99% for a used car. It may also be beneficial to use a loan calculator to see how much a loan will cost you over time. Can You Get a Mortgage With a 680 Credit Score? It shouldn’t be a problem to qualify for a mortgage loan with a 680 credit score.

Can I get a personal loan with a 680 credit score?

Yes, you should be able to get a personal loan from many lenders with a 680 credit score. Some lenders may require a higher score in the 700s, and these lenders may also give you a better interest rate.