When it comes to mortgages, there are two main ways payments can be structured: amortized and interest-only. Both borrowing structures have advantages and disadvantages, so it’s essential to understand each before committing to a loan. Here’s a look at the differences between amortized vs. interest-only payments.

When taking out a loan, one of the most important things to understand is how the repayment schedule will work. Will your monthly payments go towards both interest and principal (amortized loan) or only cover accrued interest (interest-only loan)? Knowing the difference can help you make a more informed borrowing decision.

In this article, we’ll compare interest only and amortized loans, looking at the pros and cons of each as well as how to calculate payments. Read on for a full breakdown!

What is an Amortized Loan?

An amortized loan is one where the monthly payments cover both interest charges as well as paying down the principal balance. In other words, each payment reduces the amount you owe.

With an amortized loan, while you pay the same amount each month, what that money technically goes towards changes over time In the beginning, most of the payment covers interest charges But as the loan balance decreases, more money goes towards principal.

By the end of the loan term, the entire balance will be paid off through this process. That’s why amortized loans are also known as self-amortizing loans.

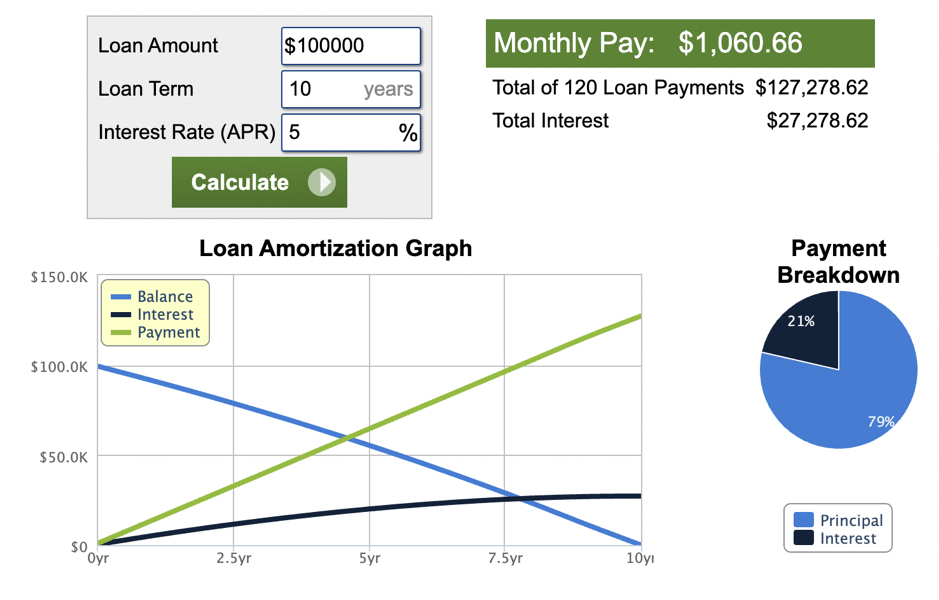

Amortized Loan Example

Let’s look at an example to understand amortized loans better Say you take out a $200,000 mortgage with a 30-year term and 5% interest Your monthly payment would be around $1,073.

Here’s a breakdown of how much would go toward interest versus principal in the first and last month of payments:

-

Month 1

- Interest payment: $833.33

- Principal payment: $239.67

- Remaining balance: $199,760.33

-

Month 360:

- Interest payment: $41.67

- Principal payment: $1,031.33

- Remaining balance: $0

As you can see, the interest portion decreases over time while the principal payment increases. This structure allows the entire balance to be paid off by the end of the term.

What is an Interest-Only Loan?

With an interest-only loan, as the name suggests, the monthly payments only cover accrued interest charges. None of the payment goes toward the principal loan amount.

So while amortized loans steadily pay down the balance each month, interest-only loans keep the principal amount static. The borrower’s payments solely cover ongoing interest as it accumulates.

Interest-Only Loan Example

Let’s use the same loan amount from our earlier example – $200,000 over 30 years at 5% interest.

With interest-only payments, the monthly payment would always equal just the interest accrued each period. So in this case, the borrower would pay $833.33 per month for 30 years.

At the end of the term, they would still owe the full $200,000 principal balance and would need to pay that off in a lump sum or refinance into a new loan.

The interest-only payments don’t build any equity in the property or pay down the amount borrowed at all.

Key Differences Between the Two Loans

Now that we’ve looked at examples, let’s summarize some of the major differences between amortized and interest-only loans:

-

Amortized loans pay down both interest and principal each month, interest-only loans only cover interest charges.

-

With amortized loans, the principal balance decreases over time. With interest-only loans, the principal stays the same.

-

Amortized loans build equity and are fully paid off by the end of the term. Interest-only loans build no equity and a large balloon payment is due at maturity.

-

Amortized loan payments are fixed if the interest rate is fixed. Interest-only payments can fluctuate if the underlying rate varies.

-

Amortized loans allow you to pay off your debt over time. Interest-only loans keep you in debt longer.

Hopefully these differences make the two loan structures much clearer!

How to Calculate Payments

When evaluating loans, it’s helpful to understand how monthly payments are calculated. Here’s an overview of the formulas for amortized and interest-only payments:

Amortized Loan Payment Formula

Monthly payment = Principal x Interest rate / 12 months x [ (1 + Interest rate/12) ^ Total months ] / [ (1 + Interest rate/12) ^ Total months – 1]

This allows you to calculate the fixed monthly payment that will pay off an amortized loan by the end of the term. Plug in the principal balance, interest rate, and total number of monthly payments.

Interest-Only Payment Formula

Monthly payment = Principal x Interest rate / 12 months

To find the monthly interest-only payments, simply divide the principal amount by 12 months and multiply by the interest rate. This will give the amount needed to cover interest charges each month.

Pros and Cons of Each Loan Type

Now let’s explore some of the key advantages and disadvantages of amortized and interest-only loans:

Amortized Loan Pros and Cons

Pros:

- Pay off debt and build equity over time

- Fixed payments (for fixed rate loans)

- Don’t need large balloon payment at end

Cons:

- Higher monthly payments

- Less flexibility if financial situation changes

- More expensive overall than interest-only

Interest-Only Loan Pros and Cons

Pros:

- Lower monthly payments free up cash flow

- Good for short-term financing needs

- Interest may be tax deductible

Cons:

- No equity buildup

- Need large payoff when loan matures

- Risk being underwater if property value drops

- Pay more interest over life of loan

As you can see, there are tradeoffs to consider with each repayment structure. Evaluate your financial situation, goals, and risk tolerance to decide which option may be a better fit.

Which Loan Type is Right for You?

Should you opt for an amortized or interest-only loan? Here are some things to think about:

-

If you want to build equity and pay off debt, an amortized loan is likely the better choice.

-

If you need lower payments in the short-term and have a plan to pay off the balance later, interest-only could work.

-

Interest-only loans involve more risk and are best for savvy investors with a strategy.

-

Amortized loans tend to be better for long-term financing needs like mortgages.

-

Consult a financial advisor to determine what repayment structure aligns with your situation and goals.

The right loan type depends on your specific circumstances. Carefully weigh the pros and cons and make sure you have a solid repayment plan in place, especially with interest-only loans.

The Bottom Line

Understanding how your loan payments get applied is key to making informed borrowing decisions. With amortized loans, monthly payments chip away at the principal and interest. But interest-only loans keep the principal static, requiring a large lump-sum payoff down the road.

Carefully considering the differences between these two options can ensure you choose the repayment structure that best fits your financial situation. Use the information in this article to help demystify amortized vs. interest only loans!

Frequently Asked Questions

Amortized loans are better because they allow borrowers to slowly pay off the principal balance of a loan over time. This can be helpful when budgeting for monthly mortgage payments. It also means the borrower won’t face a large balloon payment at the end of the loan term.

What Is an Interest-Only Loan?

With interest-only payments, the monthly payment only applies to the interest on your loan. Your payment does not pay down the loan’s principal balance unless you pay more than the minimum interest required each month. Because you only pay the interest on the loan each month, your monthly payment is lower than it would be with an amortized payment. Still, you will not make any progress towards paying off the loan principal.

Based on the same 30-year loan for $100,000 at an interest rate of 5%, the monthly payment would be $416.67 (lower than the amortized payment of $536.82). However, in this case, the entire amount goes toward the interest—the balance does not decline over time unless you make extra payments. In this example, the borrower pays $150,000 in interest (more than the total loan amount) and still owes the lender $100,000 when they get to the end of their loan term if they did not make any additional payments.

HELOC: Interest Only vs Principal + Interest

FAQ

What is the difference between interest and amortization loans?

Is an amortized loan an interest-only loan?

What is the disadvantage of fully amortized loan?

What is the difference between amortization and IO?

What is the difference between fully amortizing and interest-only mortgage payments?

Interest-only payments, which are typical of some adjustable-rate mortgages, are the opposite of fully amortizing payments. Loans for which fully amortizing payments are made are known as self-amortizing loans. Mortgages are typical self-amortizing loans, and they usually carry fully amortizing payments.

What is an amortized loan?

An amortized loan is a type of loan with scheduled, periodic payments that are applied to both the loan’s principal amount and the interest accrued. An amortized loan payment first pays off the relevant interest expense for the period, after which the remainder of the payment is put toward reducing the principal amount.

Are mortgages amortized?

Mortgages are typically amortized, though there are products available which only charge interest during the early loan period, followed by large balloon payments at the end. Amortized mortgages carry consistent monthly payment amounts, but the way interest is applied over each loan’s life is different.

What is an interest only loan?

An interest only loan is exactly what it sounds like – it’s a loan where the payments only cover the interest accruing on a loan. Unlike amortized payments that pay down both interest and principal, interest only payments do not work to pay down the loan balance.