Small business loans can assist in covering the costs of improving your small business, which can be quite expensive. For small businesses looking for additional financing, Small Business Administration (SBA) loans have some of the best terms available. Given how appealing SBA loans are, the query “can you have multiple SBA loans?” inevitably arises. Below, we dissect that query and provide you with a thoughtful response. Keep reading….

Can you have multiple SBA loans?

If you’re wondering if you can have multiple SBA loans, the short answer is yes. But it’s crucial to address two additional issues that will also be relevant.

Should I get multiple SBA loans? is the second question a business owner might want to ask. The response to this question has more specifics and considerations, which will ultimately be related to the “borrowing business” in question.

The second question that naturally comes to a business owner’s mind is, “Can I qualify for more than one SBA loan?” Once again, the answer to that query will depend on specific information pertaining to the company that is requesting the SBA funding.

Let’s address each question separately in order to further develop these responses.

Should you get multiple SBA loans?

You should carefully consider your options before deciding whether or not to apply for multiple SBA loans. The reason is that loan stacking, which involves taking out multiple loans at once, may carry risks that aren’t worth the benefits that could result. How you use the loans and your overall financial responsibility will really determine whether multiple SBA loans help your business succeed.

Fundamentally, every business owner must exercise caution to avoid overextending themselves by taking on more debt than they can reasonably afford to repay on time. The risk is obviously lower if your business is doing well and you can afford to take out multiple SBA loans quickly.

In conclusion, use your best judgment when deciding how much you can afford to borrow, and make sure you follow all SBA guidelines at every step of the way.

Can you qualify for multiple SBA loans?

Can you have multiple SBA loans? Yes.

Depending on the viability of your company’s finances, you might want to consider obtaining multiple SBA loans.

Can you qualify for multiple SBA loans? Let’s find out!

Consider the following questions:

1. Lenders will want to know that you can pay back the loan(s) that they approve because otherwise they’re putting themselves at risk of not getting paid back! Just like you don’t like dealing with late-paying customers, lenders don’t either, so they’ll want to know that your cash flow is strong. If you want to be approved for your first SBA loan, let alone a second or third, you must consistently have a positive cash flow. Additionally essential to ensuring that your company doesn’t overextend itself is a healthy cash flow.

2. The requirements for SBA funding vary between the various types of SBA loans, so check your credit score. In general, a personal credit score of 650 and a business credit score of at least 140 (FICO) are needed to be eligible for an SBA loan.

After receiving your first SBA loan, there’s a good chance the lender will demand a credit score of at least 650 if you want to be approved for another one. Business owners can raise their credit score by using credit cards to increase their chances of being approved for an SBA loan.

3. Most lenders view you as riskier as a borrower the more debt you have, so consider whether you have valuable assets to secure another SBA loan. Many lenders will require you to provide collateral in order to balance that risk. In this manner, the lender will be able to seize your valuable assets if you are unable to repay the loan or fail to do so for some other reason. Think about applying for unsecured business loans if you lack valuable assets to use as security for a loan.

Why would you need multiple SBA loans?

There are numerous factors that could force a business owner to obtain multiple SBA loans. For instance, if your first SBA loan was used to transform a very underdeveloped business into a fully functional company, a second SBA loan might be required for:

If you used a second SBA loan for one of the aforementioned purposes, you could then use a third SBA loan to cross off a different item on that list. The process of enhancing your small business requires numerous steps, each of which has a cost. You can use several SBA loans to pay for the costs associated with enhancing your business, whatever the reason.

Borrowing Limits for SBA Programs

The maximum SBA loan amount is $5 million, regardless of whether you combine SBA loans or not. There are various borrowing limits for the various SBA loan programs.

Borrowing limits for different types of SBA loans:

SBA Loan Type Borrowing Limit Standard 7(a) Loan $5 Million 7(a) Small Loan $350,000 504 Loan $5 Million Express Loan $350,000 Export Express Loan $500,000. Community Advantage Loan $250,000. Microloan $50,000. Disaster Loan $2 Million.

Combining different types of SBA loans

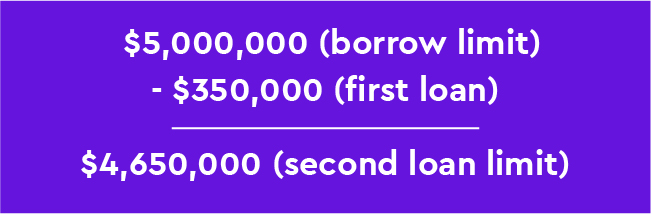

There are no restrictions on combining various SBA loan types aside from the borrowing cap. Any combination of SBA loans is acceptable, provided that the total amount of financing does not exceed the $5 million cap, despite the fact that different SBA loan types are designed to meet specific needs for business owners.

Here’s an example to illustrate this point more clearly:

Imagine that your business received a $350,000 SBA Express Loan to help with marketing, and that you then wanted to apply for a SBA 504 Loan to purchase new equipment to enable you to expand the company. That second loan amount could not be more than $4. 65 million.

Can you have multiple SBA loans? Yes, with restrictions. Now that you are aware that you can obtain a number of SBA loans, you should also be aware of the risks involved.

The dangers of stacking SBA loans

Loan stacking is the practice of a business owner taking out multiple loans at once. Loan stacking isn’t necessarily dangerous in and of itself. When deciding whether or not to take out multiple loans concurrently, there are additional factors to take into account.

Why do people stack loans?

To put it simply, improving your small business requires money. Additionally, small business owners frequently want to take several actions at once, which will result in higher costs to be paid all at once. So in order to cover those various expenses, they will jointly take out a number of business loans.

Why is loan stacking dangerous?

The issue with loan stacking is less related to the fact that multiple loans are being taken out at once. The problem is more with the justification for taking out multiple loans at once, as well as the viability of the business in question.

If the answer to either of these questions is yes, then the business owner is putting the company in danger by taking out multiple loans in order to use one loan to pay the costs of another, or by taking out multiple loans simply because they are available. This is what is meant by ‘stretching out too thin’.

The types of loans that a business can stack are frequently very expensive to take. Additionally, the more loans a company takes, the more money it spends on repaying its creditors. That leaves the business with very little money to use for crucial, even fundamental, operations.

How to apply for SBA loans

Using cutting-edge algorithms, Become is revolutionizing the business lending process. Utilizing Become’s in-house technologies, applying for SBA loans is now quicker and easier than ever. Additionally, the likelihood of approval is increased for small businesses applying for SBA loans through Become

Step-by-step guide for applying for SBA financing:

Boost your small business

The answer to the question “Is it hard to get an SBA loan?” is a resounding “No!” when applying for small business financing through Become. SBA loans are among the best types of business financing available, so what are you waiting for? Get started on improving your small or medium-sized business today with SBA funding.

We hope that this information will be useful to you as you decide whether or not to obtain multiple SBA loans. Disclaimer: The information in this article is provided for informational purposes only and is not intended to be, nor should it be construed as, legal advice on any subject. The author disclaims all liability for any damage resulting from the use of such information.

To get access to the full article answer 2 quick questions:

![]()

We value your interest in applying, so check your eligibility to expedite the process.

FAQ

Is there a limit on SBA loans?

Loan amounts The majority of 7(a) loans have a $5 million maximum loan amount. However, the maximum loan amount for SBA Express loans is $500,000 The maximum loan amount for SBA Export Express loans is $500,000 The SBA’s maximum exposure is $3. 75 million ($4. 5 million under the International Trade loan).

Can you get SBA loan 2 times?

There is no restriction on the number of SBA loan applications that may be submitted. The Paycheck Protection Program (PPP), a special lengthy program, is the only exception to this rule.

Can you get another SBA loan if you already have one?

There is nothing stopping you from having multiple SBA loans as long as each of them complies with the SBA’s lending requirements. Both SBA 7(a) and SBA 504 loans are affected by this.

Can you get multiple EIDL loans?

You may apply for only one COVID-19 EIDL. However, you may apply for both a COVID-19 EIDL and a separate EIDL if your company is situated in a region that has been declared a disaster area and has sustained additional economic harm.