Many or all of the products featured here are from our partners who compensate us. This influences which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and heres how we make money.

The hardest thing about credit might be the never-ending game of chickens when it comes to getting credit—no one wants to give you credit if you haven’t used credit in the past.

However, this does not imply that you have a zero credit score if you have never had credit and do not have a credit score. You have the absence of a score: You’re “credit invisible. ”.

Yo, credit newbies! Ever wondered why you don’t have a credit score? Don’t worry, it doesn’t mean you’re starting from scratch or that you have a zero credit score It just means you’re credit invisible, a fancy term for not having enough credit history for the credit bureaus to calculate a score.

Why You Might Not Have a Credit Score

- Credit newbie: You’ve never had a credit card or loan in your name.

- Inactive credit: You haven’t used credit in at least six months.

- Recent credit user: You’ve only recently applied for credit or been added to an account.

What’s the Starting Point for Your Score?

Even though you don’t have a credit score yet it doesn’t mean you’re starting at the bottom. Think of it like starting a video game with a blank character sheet – you have potential but you need to build your skills and experience to level up.

The credit bureaus are unable to predict your likelihood of repaying a loan because they do not have enough information about you. However, as soon as you begin using credit responsibly, information is gathered and your score is determined.

How to Get Your Credit Journey Started

Ready to become a credit master? Here’s how to get started:

- Get a secured credit card: These cards require a security deposit, which becomes your credit limit. Use it responsibly and pay your bills on time to build a positive credit history.

- Consider a credit-builder loan: These loans are specifically designed to help you build credit. You make regular payments, and the lender reports them to the credit bureaus.

Pro Tips for Building a Stellar Credit Score

- Pay your bills on time, every time: This is the most important factor affecting your credit score.

- Keep your credit utilization low: Aim to use less than 30% of your available credit limit.

- Have a mix of credit accounts: Include both installment loans (like car loans) and revolving credit (like credit cards) in your portfolio.

By following these tips, you’ll be on your way to building a strong credit score, which will open doors to better interest rates, lower insurance premiums, and access to more financial products Remember, it’s a marathon, not a sprint, so be patient and consistent with your efforts.

Don’t Sweat the Numbers

While it’s important to build a good credit score, don’t get too hung up on the exact number. Your score fluctuates based on various factors, so focus on improving your overall creditworthiness.

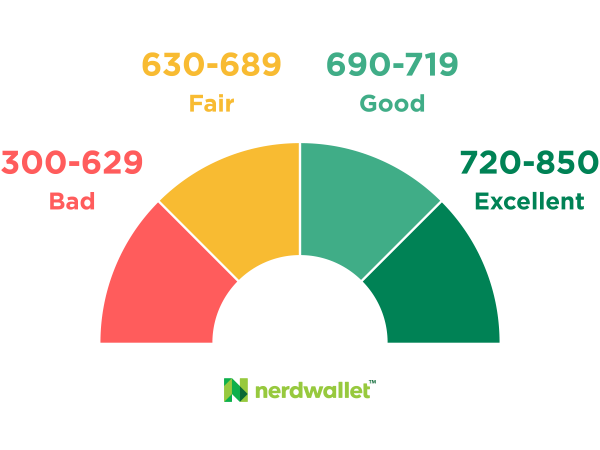

Instead of obsessing over the three-digit number, aim for the “general risk” category. Most lenders categorize scores as follows:

- 300-629: Bad credit

- 630-689: Fair credit

- 690-719: Good credit

- 720 and up: Excellent credit

You can open up a world of financial opportunities and naturally climb towards a higher credit score by concentrating on developing good credit habits.

Key Takeaways

- Having no credit score doesn’t mean you have a zero credit score.

- You can build a good credit score by using credit responsibly and making timely payments.

- Focus on improving your overall creditworthiness rather than obsessing over the exact score.

Now go forth and conquer the world of credit, young padawan!

What’s the starting point for your score?

Being new to credit does not imply starting at zero, nor does it imply starting at 300 in the basement. After all, if you’ve never had credit, you’ve never made score-devastating mistakes.

The credit bureaus simply don’t know enough about you when you don’t have a credit history to determine whether or not you will repay loans. And that’s all a credit score is: an estimation, derived from the information in your credit reports, of your propensity to repay the next credit you receive.

Once you begin using credit, scores can be calculated. You probably won’t have a high credit score to begin with, but you also won’t be at the very bottom.

Why you don’t have a credit score

No matter how severely someone has misused credit in the past, no one has a credit score of zero.

The most widely used credit scores, FICO and VantageScore, are on a range from 300 to 850. As of April 2021, only 3% of consumers had a FICO 8 score below 500. Tommy Lee, principal scientist at FICO, said scores of 300 are “extremely rare. “.

Reasons you might not have a score are:

- You’ve never been listed on a credit account.

- You haven’t used credit in at least six months.

- You haven’t added anything to your account or applied for credit until recently.

How Do I Get A Zero Credit Score?

FAQ

How do you get your credit score to 0?

How long does it take for your credit to go to zero?

|

How Long Information Stays on Your Credit Reports

|

|

|

Type of Information

|

Timeframe

|

|

Late or missed payments

|

7 years from the original delinquency

|

|

Default, including foreclosure, repossession and settlement

|

7 years from the original delinquency

|

|

Hard credit inquiries

|

2 years from the date of the inquiry

|

Is it good to have zero credit?

What credit score do you need for 0?

Do you have a credit score of zero?

No one actually has a credit score of zero, even if they have a troubled history with credit. The FICO scoring model, for instance, ranges between 300 and 850. It’s rare for anyone to have a score below 470. According to Experian, 99% of consumers have FICO scores higher than 470. But if you have no credit history, you don’t have a score at all.

How do I get a free credit score?

Get your free credit score. Sign up for your free credit report and credit-building Nerdy insights personalized to you. NerdWallet uses 128-bit encryption to secure your information. Check your free credit score and credit report, and get alerts about changes so you can manage your credit effectively.

How to build credit if you don’t have a credit score?

A secured credit card is one of the easiest ways to build credit if you don’t have a credit score. Secured credit cards require a deposit that will serve as collateral for the card company. The deposit will often equal the credit limit of the card. For example, a card with a $200 deposit will have a $200 credit limit.

Can I check my credit score without a credit card?

Yes! You can sign in to NerdWallet at any time to see your free credit score, your free credit report information — and much more. There’s no credit card required, no cost. If you’re curious, here’s how we make money. How can I check my credit score? How often does it change?