Buying a home is an exciting milestone in life. But it also involves a lot of big decisions, like choosing the right mortgage. Two popular options for first-time and low- to moderate-income homebuyers are FHA loans and USDA loans. So how do you decide between an FHA loan versus a USDA loan?

I compared the key differences between these government-backed mortgages. Keep reading to learn which type of home loan may be a better fit based on your budget, credit, down payment, location and more.

Overview of FHA and USDA Loans

First, let’s go over the basics of what makes FHA and USDA loans unique:

-

FHA loans are backed by the Federal Housing Administration, They offer low down payments and more flexible credit requirements FHA loans can be used in any location

-

USDA loans are backed by the U.S Department of Agriculture. They offer no down payment and low rates. But USDA loans can only be used in designated rural and suburban areas.

While FHA and USDA loans share some similarities, their main eligibility and program differences come down to location, income limits, and down payment requirements.

USDA Loan Overview

USDA loans help low- to moderate-income borrowers access affordable financing to buy homes in rural and suburban neighborhoods. Some key facts about USDA loans:

-

Location: The home must be in an eligible rural area as designated by the USDA property eligibility tool. Suburbs can qualify.

-

Income limits: Your household income must be below 115% of the area’s median income. USDA loans have income caps that vary by region.

-

Down payment: USDA loans require 0% down. You can finance 100% of the home’s purchase price plus closing costs.

-

Credit score: No official minimum, but most lenders require a credit score of at least 640.

-

Other costs: Upfront guarantee fee of 1% of the loan amount and annual fee of 0.35% of the balance.

A big perk of USDA loans is the zero down payment, which removes a major barrier to homeownership. USDA loans also come with competitive interest rates thanks to their government backing. Just keep in mind the property location and income limits when considering this option.

FHA Loan Overview

FHA loans are popular with first-time homebuyers, borrowers with lower credit scores, and buyers who can’t afford a large down payment. Here are the main features of FHA loans:

-

Location: FHA loans can be used to buy homes anywhere in the U.S. – urban, suburban or rural areas.

-

Income limits: No income limits for FHA loans. Your income just needs to be enough to repay the mortgage.

-

Down payment: Minimum 3.5% down if your credit score is 580 or higher. 10% down for scores of 500-579.

-

Credit score: Minimum 580 FICO score required in most cases. FHA loans are more flexible for buyers with less-than-perfect credit.

-

Other costs: Upfront mortgage insurance premium and annual mortgage insurance premium.

FHA loans offer more flexible qualifying guidelines for borrowers who don’t fit the criteria for conventional mortgages. Just be prepared for mortgage insurance premiums when budgeting your total monthly payment.

Comparing Key Differences

Now let’s dive deeper into how FHA and USDA loans stack up across some major factors:

Eligibility

One of the biggest differences between FHA and USDA loans comes down to location and income eligibility:

-

Location: FHA loans can be used anywhere in the U.S. USDA loans are restricted to designated rural and suburban areas.

-

Income limits: FHA loans don’t have income limits. USDA loans require your income to be at or below 115% of the median income for the area.

So right off the bat, your location and income level will determine if you qualify for one type of loan over the other. Use the USDA Property Eligibility tool to check if your target home is in a USDA-eligible area. And review the USDA income limits for your state and county.

Down Payment

FHA and USDA loans take different approaches when it comes to down payments:

-

FHA loans: Require a minimum down payment of 3.5% of the purchase price if your credit score is 580 or above. Or 10% down if your credit score is between 500 to 579.

-

USDA loans: Require 0% down. You can finance 100% of the home’s purchase price plus closing costs.

Clearly, USDA loans offer the biggest advantage if you don’t have savings for a down payment. With an FHA loan, you can still buy a home with a low 3.5% down payment. But the zero down payment feature of USDA loans makes them extremely attractive to eligible buyers.

Closing Costs

Closing costs may also factor into your decision between FHA and USDA loans:

-

FHA loans: Closing costs vary by lender. The buyer typically pays their own closing costs, which can be several thousand dollars.

-

USDA loans: Can finance up to 100% of the home’s value. This allows you to roll closing costs into the mortgage. USDA also allows 6% seller concessions.

As you can see, USDA loans offer more flexibility for financing closing costs. With an FHA loan, you’ll likely need to pay closing costs out of pocket, so save up accordingly.

Interest Rates

Thanks to government backing, FHA and USDA loans can feature lower interest rates than conventional loans:

-

FHA loans: Rates vary by applicant and market rates. Your down payment, credit score, and other factors determine your rate.

-

USDA loans: Rates can be competitive with FHA loans or potentially lower. Backing from USDA allows flexibility for reduced rates.

In general, both FHA and USDA loans make it possible to secure lower interest rates than you may get with a conventional mortgage based on your credit and financial profile. Shop around with multiple lenders to find the best rates.

Mortgage Insurance

With both FHA and USDA loans, you’ll pay mortgage insurance:

-

FHA loans: Upfront mortgage insurance premium of 1.75% of the loan amount. Plus an annual mortgage insurance premium of 0.45% to 1.05% of the loan amount.

-

USDA loans: 1% upfront guarantee fee and annual fee of 0.35% of the loan balance.

The mortgage insurance costs are baked into your loan with both products. USDA loans have slightly lower annual fees. But on an FHA loan, you may be able to cancel mortgage insurance after 11 years once you reach 20% home equity.

Credit Score Requirements

FHA and USDA loans are more flexible with credit requirements than conventional mortgages:

-

FHA loans: Minimum credit score of 580 for 3.5% down. Scores as low as 500 can qualify with 10% down.

-

USDA loans: No published minimum credit score. But lenders typically require a minimum score around 640.

So FHA loans offer more leeway for buyers with poorer credit. If your score is below 640, an FHA loan likely presents the easier path to approval. USDA also allows manual underwriting for low scores under 640. But most lenders will want to see higher scores.

Pros and Cons of FHA vs. USDA

| Pros | Cons | |

|---|---|---|

| FHA Loans | – Available anywhere in U.S.<br>- No income limits<br>- Lower minimum credit scores<br>- Low 3.5% down payment | – Mortgage insurance premiums<br>- Must have funds for down payment + closing costs |

| USDA Loans | – 0% down payment <br>- Can finance closing costs <br>- Low rates with government backing<br>- Lenient credit guidelines | – For rural/suburban areas only<br>- Income limits apply<br>- Potentially longer approval process |

To recap, FHA loans are more widely available and better for lower credit scores. But USDA loans offer the biggest advantage with their no down payment program. Think about which features matter most as you weigh FHA vs. USDA loans.

Which Is Better for You?

There’s no definitive answer to whether FHA or USDA loans are better across the board. The right loan type depends on your specific homebuying situation.

Here are a few key questions to help you determine if an FHA or USDA loan may be a better fit:

- Is your income below the limits in your area for a USDA loan?

- Is the home you want to buy in an eligible rural or suburban location for a USDA loan?

- How much money have you saved for a down payment and closing costs?

- What is your current credit score?

- Do you value flexibility in location over the lowest down payment?

Look at your unique goals and financial circumstances. If you meet location an

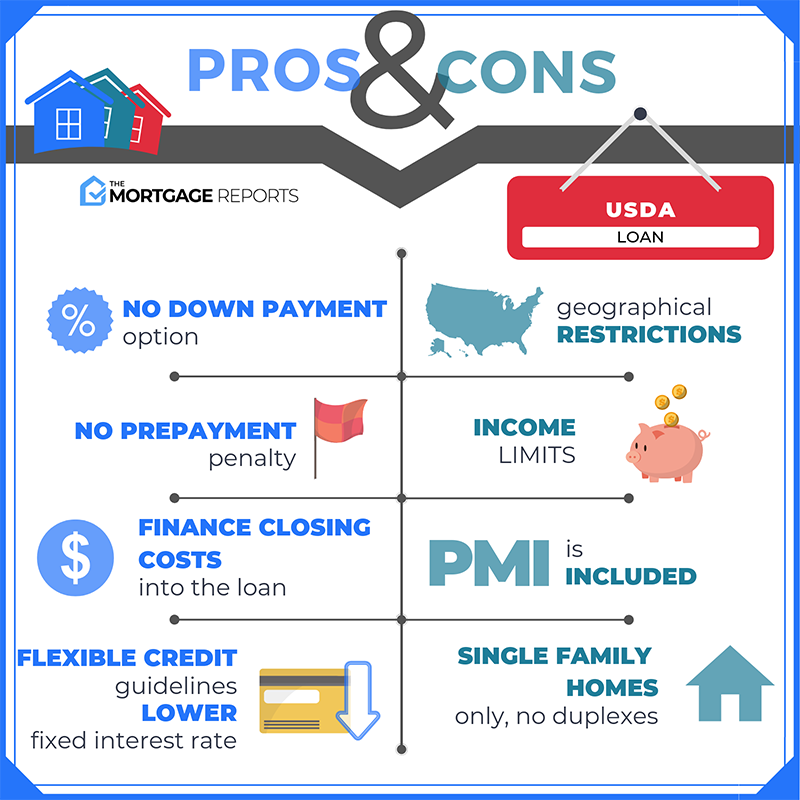

Pros and cons of USDA loans

The USDA loan has quickly risen in popularity with first-time and lower-income borrowers thanks to its zero-down allowance and low rates. But not everyone will qualify. Here’s what you should know.

Con: You must buy in a rural location

USDA eligibility depends on the location of the home. You must purchase a property in a rural area as the USDA defines it. But the definition of “rural” is quite liberal, and it’s based on U.S. census information from more than 15 years ago. So many suburban areas are still eligible.

USDA publishes online maps that buyers can use to check the eligibility of a certain address or geographical area. Buyers will find that some entire states are USDA-eligible. Even highly populated states contain surprisingly vast qualifying areas. An estimated 97% of the American landscape is geographically eligible for a USDA loan.

Still, some buyers might find that eligible areas are too far outside employment centers and, for that reason, choose an FHA loan, which comes with no geographical restrictions.

FHA Loan vs USDA

FAQ

Is a USDA loan better or FHA?

What is one advantage a USDA loan has over the FHA loan ______?

Are USDA loan payments cheaper?

Can you have a USDA and FHA loan at the same time?

How do I qualify for an FHA vs USDA loan?

Being eligible for an FHA vs. USDA loan means meeting specific requirements. To qualify for an FHA loan, prepare to: Make a down payment of at least 3.5% with a credit score of 580 or higher, or a down payment of 10% with a credit score between 500 and 579. Pay an upfront mortgage insurance premium at closing equivalent to 1.75% of the loan.

Are USDA loans better than FHA loans?

USDA loans require a higher credit score than FHA loans, and they also carry geographical restrictions for where you can buy a qualifying home. USDA loans also have income limits for prospective homeowners, while FHA loans impose no such limits.

Why are USDA and FHA loans so popular?

Home buyers with low or moderate incomes may gravitate toward mortgages with more lenient borrowing requirements, especially when it comes to down payments and mortgage insurance. This is why USDA and FHA loans can be so appealing to borrowers. How do the two types of mortgage loans differ, though?

What is the difference between USDA & FHA mortgage eligibility?

USDA and FHA loans differ in their mortgage eligibility requirements. A few of the biggest eligibility factors include the location of the home and your income level, credit score, debt-to-income (DTI) ratio and down payment amount. Let’s break down each of these qualifications.