Buying your first home is an exciting milestone! But it can also feel overwhelming especially when it comes to finding the right mortgage. Two popular options for first-time buyers are FHA loans and USDA loans. Both are government-backed mortgages that offer more flexible eligibility requirements than conventional loans.

But how do you know whether an FHA or USDA loan is better for your situation? In this comprehensive guide, we’ll break down the key differences between FHA and USDA loans. I’ll explain the pros and cons of each so you can make an informed decision when applying for home loans.

Overview of FHA and USDA Loans

First, let’s cover the basics. FHA loans are insured by the Federal Housing Administration. USDA loans are backed by the U.S. Department of Agriculture. The government agencies guarantee these mortgages, protecting lenders from losses if borrowers default.

In exchange, lenders offer FHA and USDA borrowers

- Lower down payments

- More lenient credit requirements

- Lower interest rates

These perks make FHA and USDA loans ideal for first-time buyers and those with lower incomes or credit scores. You work directly with private lenders when applying. The lender handles underwriting and origination, while the government agency provides insurance.

Both loans charge an upfront mortgage insurance fee at closing, as well as ongoing monthly premiums. This helps fund the programs.

Now let’s get into the details on eligibility, costs, and other factors that differentiate FHA vs USDA loans.

FHA Loan Requirements

FHA loans are available nationwide to qualifying borrowers. Here are the basics on FHA eligibility:

- Minimum credit score: 500 with 10% down, 580 with 3.5% down

- Down payment: At least 3.5%

- Income limits: None

- Debt-to-income ratio: Typically up to 45%

- Loan amounts: Vary by county, up to $726,525 in high-cost areas

So FHA loans allow very low down payments and credit scores. You can also carry more existing debts compared to conventional loans.

However, FHA mortgage insurance is more expensive. Rates range from 0.45% to 1.05% of the loan amount annually. It lasts the life of the loan unless you put down at least 10%.

USDA Loan Requirements

USDA loans help low- to moderate-income buyers purchase homes in rural and suburban locales. Here are the eligibility basics:

- Minimum credit score: Typically 640

- Down payment: None required

- Income limits: Below 115% of the area median

- Debt-to-income ratio: Usually up to 41%

- Location: Property must be in an eligible rural zone

The big perks of USDA loans are zero down payment and lower mortgage insurance around 0.35% annually. But you must buy outside urban centers in a USDA-designated area. Income limits also apply.

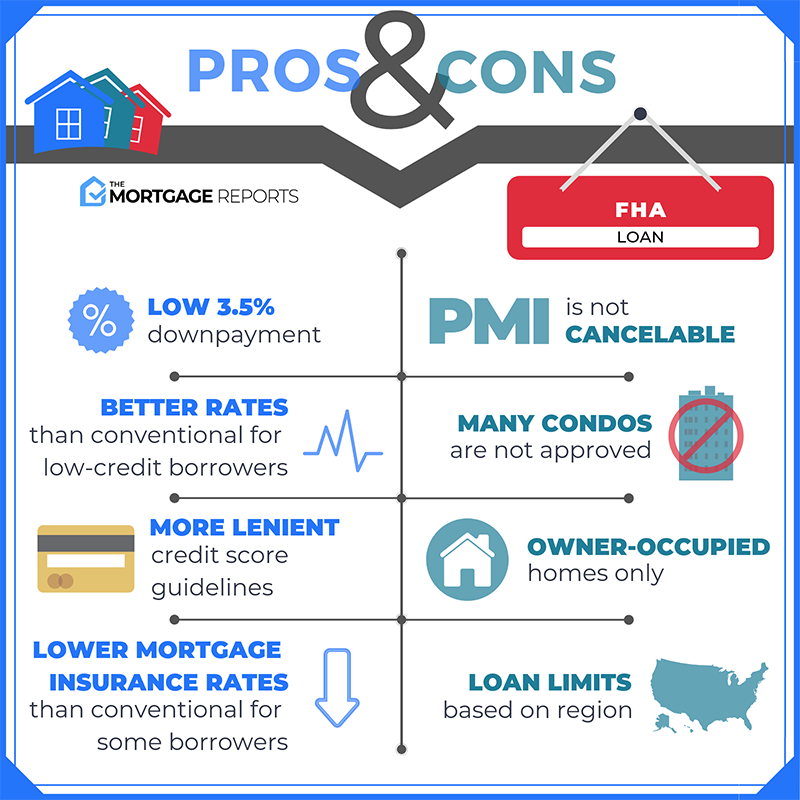

Pros and Cons of FHA Loans

Now that you understand the basics, let’s dive into the pros and cons of FHA loans compared to USDA mortgages. We’ll start with the key benefits borrowers enjoy with FHA financing:

Pros

- Available nationwide – No geographic restrictions like USDA loans

- Lower credit score requirements – Minimum 500 FICO

- Higher DTI allowed – Up to 45% in many cases

- Buy multifamily properties – USDA is single-family only

- Lower MI with 10% down – MIP drops off after 11 years

However, there are some potential drawbacks to weigh as well when considering an FHA loan:

Cons

- Higher monthly mortgage insurance – Around 0.85% of loan amount

- MIP never drops off – Except with 10%+ down payment

- Must be owner-occupied – Can’t be used for investment properties

- Lower purchase power – Due to DTI caps under 45%

As you can see, it’s a tradeoff. You gain more flexible credit requirements with an FHA loan. But you’ll also pay more in mortgage insurance over the long run compared to alternatives like USDA.

Pros and Cons of USDA Loans

Now let’s walk through the unique benefits and drawbacks of USDA lending:

Pros

- Zero down payment – 100% financing available

- Very low mortgage insurance – Around 0.35% annually

- Competitive interest rates – Due to government backing

- Income limit flexibilities – In some cases >115% of median

Cons

- Limited availability – Only designated rural areas

- Strict income caps – Household must be below limit

- Longer closing timelines – Due to extra USDA underwriting

- Single-family only – No multi-unit USDA loans

The tradeoffs are reversed here. You gain exceptional affordability via the zero-down allowance and cheap mortgage insurance. But availability is restricted based on location and income.

How To Choose: FHA vs USDA

Now that you understand the key differences, how do you choose between FHA and USDA loans?

Here are a few key questions to ask yourself:

-

Is my target home in a USDA-eligible area? Check the USDA property eligibility map. If not, FHA is your only option.

-

Do I meet USDA income limits for my county? Look up the limits to see if your household qualifies. If not, consider FHA.

-

How is my credit score? FHA allows scores as low as 500, whereas USDA typically requires 640+. Weigh options if your score falls in between.

-

Can I afford the USDA upfront guarantee fee? It’s 1% of the total loan amount. Save with FHA if you can’t pay this at closing.

-

Which mortgage insurance costs less? Compare options based on your down payment, loan amount, and credit score.

Doing a full comparison of mortgage rates and costs will help determine whether FHA or USDA offers the most savings. Be sure to get rate quotes from multiple lenders as you assess your options.

While eligibility rules may steer you toward one or the other, your budget and goals should drive the final decision. Meet with loan officers to discuss your unique situation before applying.

Next Steps After Choosing FHA or USDA

Once you select the government-backed loan that best fits your needs, what comes next? Here are key steps to take after choosing FHA vs USDA:

-

Get pre-approved – Confirm you qualify and what rates/fees to expect

-

Shop for homes – Focus your search on properties that meet loan requirements

-

Make an offer – Get pre-approved first to make your offer more attractive

-

Finalize loan – Provide documents for underwriting as needed

-

Close on home – Review closing disclosures; ask about final costs

-

Move in – Complete final walkthrough; get keys and start enjoying your new home!

The pre-approval process will verify eligibility for your selected loan program. This gives you bargaining power when submitting offers since sellers know you can secure financing.

Stay in close touch with your loan officer throughout the transaction. They’ll guide you through final underwriting, the closing process, and answering any last-minute questions about your FHA or USDA mortgage.

The Bottom Line

Whether you choose an FHA loan or USDA mortgage, you’ll benefit from competitive rates and buying power. Both offer more accessible financing than conventional loans. Your personal situation will determine which government-backed option fits best.

Now you have a complete guide comparing FHA and USDA loans. Follow the steps above to pick the right loan, get pre-approved, and start turning your homeownership dreams into reality!

Pro: Zero down payment required

USDA loans require no down payment. You may finance up to 100% of the property value, which, sometimes, is above the home’s purchase price. In these cases, the buyer can finance closing costs.

For example, say you make an offer on a home for $200,000. The lender’s official appraisal report states the home is worth $205,000. The buyer can open a USDA loan for the full value, as long as the excess funds are applied to closing costs such as the title report, loan origination fees, homeowner’s insurance, and prepaying property taxes and homeowner’s insurance.

So, in the end, USDA borrowers could get into a home with close to nothing out of pocket.

With FHA, the home buyer must come up with a 3.5% down payment plus closing costs. The FHA has no guidelines stating that the loan amount can exceed the purchase price. The only way to get a zero-out-of-pocket loan with FHA is to get a substantial down payment gift, down payment assistance, or seller contributions for closing costs.

The USDA is more flexible, and buyers with little cash on hand should look into this option first.

Pros and cons of FHA loans

While USDA loans stand out for being ultra-affordable, many borrowers prefer an FHA mortgage for its looser underwriting requirements.

There are no income limits for an FHA loan, and you might be able to get away with a lower credit score and higher debts than USDA or conventional lenders would allow. Here’s what you should know.

FHA Loan vs USDA

FAQ

What credit score do you need for a FHA and USDA loan?

What’s the difference between FHA and USDA loans?

Does USDA follow FHA guidelines?

What are the pros and cons of a USDA loan?

|

Pros

|

Cons

|

|

No down payment

|

Income limits

|

|

Competitive interest rates

|

Property restrictions

|

|

Relaxed credit requirements

|

Occupancy requirements

|

|

No PMI requirement

|

USDA program fees

|

What is a USDA home loan?

A USDA home loan, backed by the United States Department of Agriculture, is a type of mortgage offered to eligible buyers of approved properties in rural locations that qualify. USDA loans require no down payment for qualified borrowers.

How do I qualify for an FHA vs USDA loan?

Being eligible for an FHA vs. USDA loan means meeting specific requirements. To qualify for an FHA loan, prepare to: Make a down payment of at least 3.5% with a credit score of 580 or higher, or a down payment of 10% with a credit score between 500 and 579. Pay an upfront mortgage insurance premium at closing equivalent to 1.75% of the loan.

Are FHA loans better than USDA loans?

FHA loans are more widely accessible since they’re generally not limited by location, and they often help first-time buyers. USDA loans, on the other hand, help people afford homes in rural areas. FHA loans are widely available mortgage loans offered by private lenders and insured by the FHA.

Why are USDA and FHA loans so popular?

Home buyers with low or moderate incomes may gravitate toward mortgages with more lenient borrowing requirements, especially when it comes to down payments and mortgage insurance. This is why USDA and FHA loans can be so appealing to borrowers. How do the two types of mortgage loans differ, though?