You’re here because you want to know definitively: “Can you purchase land with a VA loan?“

The short answer is “YES,” you can use a VA loan to purchase land, but there are some important conditions and limitations to be aware of, which we’ll cover in this blog post.

The VA allows veterans to use their VA loan to buy land and construct a new home on the property at the same time.

VA loans must be used for eligible purchases, which includes the purchase or construct a residence, including a condominium or cooperative unit, to be owned and occupied by the veteran as a home.

Buying land to build your dream home can be an exciting prospect. With a VA loan, active duty military members, veterans, and surviving spouses may be able to finance both land and construction costs into one VA mortgage loan.

However, there are some specific requirements and limitations to be aware of when using a VA loan for a land purchase. In this comprehensive guide, we’ll cover everything you need to know about using a VA loan to buy land.

Can You Buy Raw Land With a VA Loan?

The short answer is yes, you can buy vacant land with a VA loan, but only if you construct a home on it simultaneously.

The VA will not finance the purchase of land by itself, The land purchase must be combined into one loan with the construction of a home that you intend to live in as your primary residence,

So if you find a perfect plot of land you want to buy now and build on later, a VA loan won’t work for the initial land purchase. You’d need to explore other financing options

However, if you wish to buy land and build right away, the VA will allow you to roll the land acquisition and construction costs into one VA loan. This is called a VA construction loan.

Requirements for Buying Land and Building With a VA Loan

While the VA does permit financing land and construction in one loan, there are strict requirements:

-

The home must be for your own occupancy and primary residence. Investment properties or vacation homes are not eligible.

-

The property can be no more than 4 units. Each unit must have its own connections for water, sewer, electricity, and gas.

-

The home must meet VA minimum property requirements as well as all local building codes and zoning laws.

-

The land cannot be in a flood zone or area with excessive noise such as an airport runway.

-

There cannot be environmental hazards nearby like a landfill or industrial plant.

-

The site cannot be vulnerable to landslides, earthquakes, or other instabilities.

-

Your builder must be registered with the VA and hold a valid VA ID number.

In addition to these requirements, you’ll need a Certificate of Eligibility proving your eligibility for a VA loan based on your military service.

How to Buy Land and Build a Home with a VA Loan

If you wish to buy land and build right away, there are a couple options:

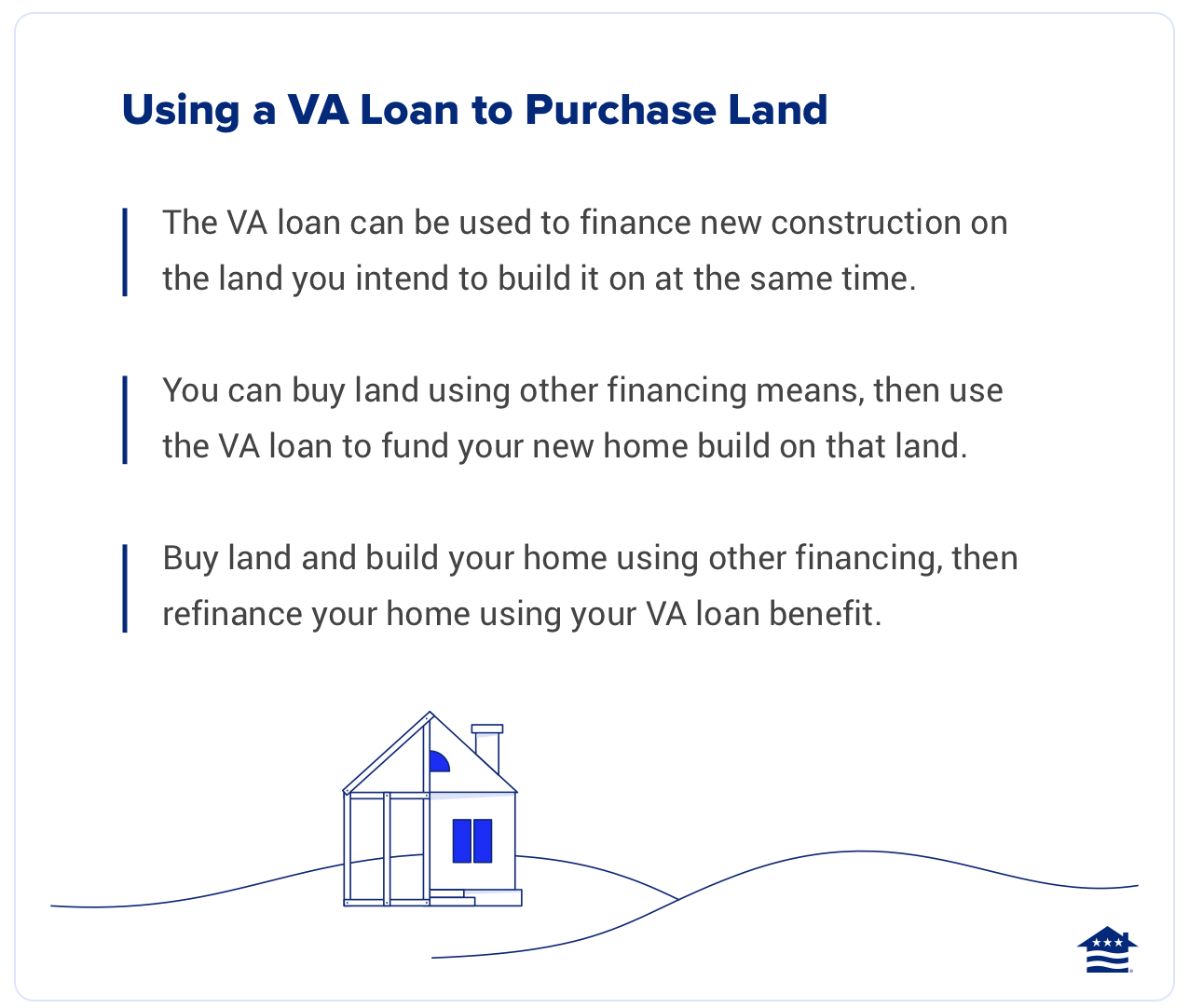

Finance the land purchase and construction together in one VA loan. This is a VA construction loan. With this option, you can roll the entire cost to acquire land and build a home into one VA mortgage. This avoids the need for two separate loans.

Buy the land separately, then get a VA construction loan. Alternatively, you can buy land with cash or another type of financing first. Then get a standalone VA construction loan to finance building the home. Once construction is complete, you may be able to refinance into a standard VA mortgage.

While permitted, most lenders do not offer VA construction loans frequently. You may need to shop around to find a lender able to assist with this type of transaction.

Your best bet is connecting with a knowledgeable VA loan specialist who can guide you through the process and requirements.

Are There Acreage Limits on VA Loans?

Unlike some other mortgage programs, there are no strict acreage limits imposed by the VA. As long as the property meets VA requirements, you can use a VA loan to buy land regardless of acreage.

Of course, lenders will limit the loan amount you qualify for based on your income, assets, and ability to repay the mortgage. But the VA does not set maximum acreage limits.

So whether you want to build on a quarter acre suburban lot or 80 acres out in the country, a VA loan can work provided you meet general VA requirements.

Pros and Cons of Using a VA Loan to Buy Land

VA loans offer key benefits like no down payment and no monthly mortgage insurance that make them very attractive for land purchases and construction. However, there are also some potential drawbacks to be aware of:

Pros

- No down payment required

- No monthly mortgage insurance (PMI)

- Potentially lower rates than conventional loans

- Builder must be VA-approved

- Lender oversees all stages of construction

Cons

- Stricter requirements than conventional loans

- Not all lenders offer VA construction loans

- Can only finance land if building a home immediately

- 1-2% VA funding fee

As with any major financial decision, it’s wise to weigh the pros and cons before choosing your financing. Speaking with a VA specialist can help you determine if a VA construction loan is the right fit.

Alternatives to Using a VA Loan for Land

If you decide a VA loan isn’t the optimal financing solution for your land purchase, here are a couple alternatives to consider:

-

USDA loans – Like VA loans, these require no down payment and no PMI. USDA loans can finance both land and construction costs. Eligibility is based on property location outside city limits.

-

Construction loans – Offered by many lenders, these short-term loans specifically finance construction. Once the home is built, you can pursue long-term financing.

-

Conventional loans – Loans that are not backed by a government program. May offer more flexibility than VA loans on land purchases.

-

Owner financing – The land owner finances the purchase directly. You repay the loan over time back to the seller.

As you can see, VA loans can be a great option if you want to buy land and build right away. Just be sure you understand the requirements and restrictions. Consulting with an expert VA lender is key to navigating the process smoothly.

Can I Use My VA Loan to Buy Land?

Yes, you can use your VA loan to buy land; however, there are some important conditions and limitations to be aware of:

- Construction Intent: The primary purpose of using a VA loan to purchase land is for building a home on that land. VA loans are not typically used for vacant land purchases without the intention of constructing a home within a reasonable timeframe.

- Eligibility: To use a VA loan to buy land and build a home, you must meet the eligibility requirements for a VA loan. This typically involves being an eligible veteran, active-duty service member, member of the National Guard or Reserves, or a surviving spouse of a service member who died in the line of duty or because of a service-connected disability.

- Entitlement: Your VA loan entitlement limits the total amount of the loan you can obtain without a down payment. This limit can vary depending on your location and whether you have used your VA loan entitlement before.

- Construction Plans: When you use a VA loan for land and construction, you will need to have approved construction plans and obtain necessary permits. The VA lender will need to review and approve these plans.

- Construction Timeline: The construction must typically start within a certain timeframe after the land purchase, usually within one year. The VA wants to ensure that the land purchase is not speculative and that the primary purpose is to build a home.

- Loan Limits: VA loan limits vary by county, and there may be a maximum loan amount that you can borrow. Be sure to check the loan limits in your area.

- Appraisal and Valuation: The land you intend to purchase will need to be appraised, and the VA lender will consider the appraised value when determining the loan amount. The appraisal must also consider the future value of the completed home.

It’s essential to work with a VA-approved lender who is experienced with VA land and construction loans, as the process can be more complex than a traditional VA home loan.

District Lending can guide you through the requirements and ensure that you meet all the necessary criteria for using a VA loan to purchase land and build a home.

In conclusion, purchasing land with a VA loan is indeed possible, but it comes with specific conditions and limitations designed to ensure that the primary purpose is to construct a home on the property.

Veterans and eligible individuals can use a VA loan to buy both land and property together, provided they have approved construction plans, intend to build on the land immediately, and meet various eligibility criteria.

While these requirements may seem stringent, they are in place to safeguard the intent of VA loans and ensure that they are used for their intended purpose of helping veterans secure a home.

To navigate the complexities of VA land and construction loans, it is crucial to collaborate with a knowledgeable VA-approved lender like District Lending, who can guide you through the process and help you fulfill all the necessary criteria for purchasing land and building your dream home with a VA loan.

How Can You Purchase Land With a VA Loan?

According to VA loan guidelines, eligible borrowers can use a VA loan to buy land and property together, but not land by itself.

That means you can’t buy a piece of land with your VA loan and sit on it.

You can use your VA loan to buy land directly if you also have plans to build on the property right away.

You can apply for a combined purchase and construction loan through a VA-approved lender like District Lending.

You’ll need to submit formal construction plans and, upon completion, have the finished property inspected.

Additionally, your construction plans must meet the following criteria:

- You must work with a VA-approved builder with valid VA identification.

- You cannot build a home with more than four units. Each unit must have its own utility connections, and you must occupy one of the units as your primary residence.

- Your property must be built on and affixed to a permanent foundation.

- Your property must conform to the VA’s minimum property requirements. It must also meet federal and local building requirements.

- Your land cannot be in a flood or noise zone, near a landfill, or in an area vulnerable to major natural disasters like landslides or earthquakes.

Can You Use the VA Loan to Buy Land?

Can you buy land with a VA loan?

There are no VA loan acreage limits. In other words, the VA does not set a maximum size for the property you can buy. You may be limited, however, by what the lender is willing to approve you for based on affordability. Should You Use a VA Loan to Buy Land?

Can a VA loan buy a house?

For military borrowers, loans backed by the U.S. Department of Veterans Affairs (VA) are an attractive option, since they don’t require a down payment and can offer better terms than a land loan from a bank or credit union. You can use a VA loan to buy land as long as the land currently has, or will soon have, a home on it.

Can a VA loan be used for a farm residence?

VA loans can be a great tool for acquiring a farm residence. You can use your VA home loan benefit to purchase, build or repair a farm residence on land you own or land you plan to buy. Requirements to use a VA loan for farm land include: The VA home loans discussed above can be used to buy and build your next home.

Can veterans use VA home loan benefits to buy land?

The best way for veterans to use their VA home loan benefits to buy land is by starting home construction right after buying the land. The benefit of this method is the opportunity for borrowers to roll the total cost of land and construction into one loan.