This calculator will help you to compare the costs between a loan that is paid off on a bi-weekly payment basis and a loan that is paid off on a monthly basis. You can use this for any type of loan including home loans. We also offer a separate biweekly mortgage calculator.

The Ins and Outs of Biweekly Loan Amortization Schedules

Taking out a loan is a serious financial decision that requires careful consideration One important factor when taking out a loan is understanding how the payments will be structured over the full repayment term This is where amortization schedules come in handy.

In this article, we’ll provide a comprehensive overview of biweekly loan amortization schedules—what they are, how they work, and how you can use them to your advantage when taking out a loan Whether you’re considering a mortgage, auto loan, or other type of installment loan, understanding biweekly amortization can help you make the smartest borrowing decisions

What is a Biweekly Loan Amortization Schedule?

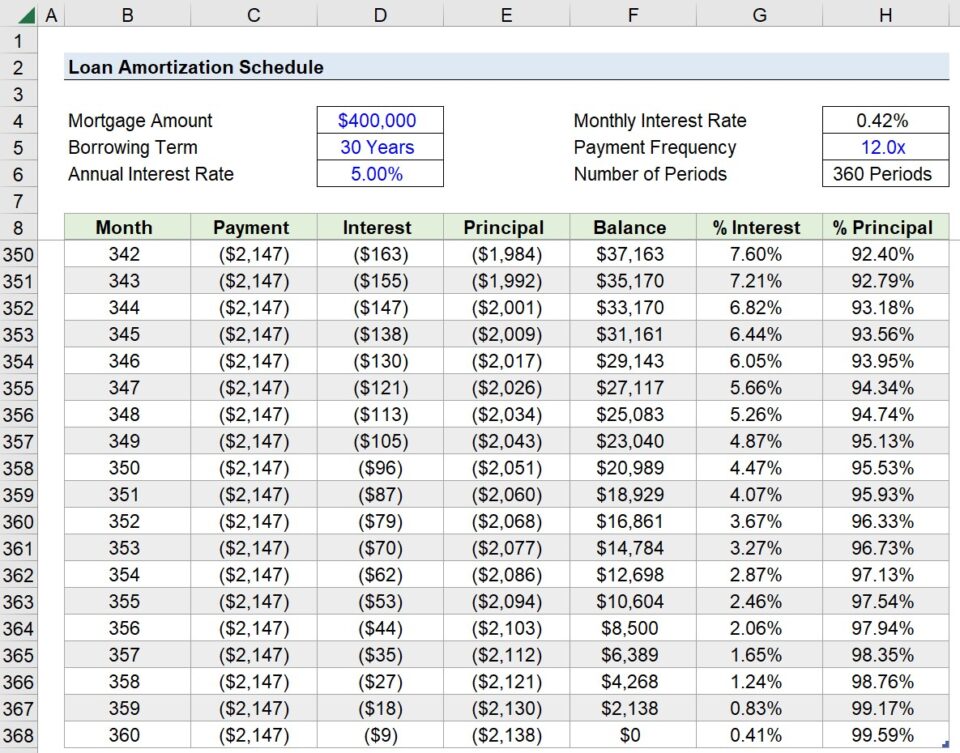

An amortization schedule is a complete table showing each payment on a loan over its full repayment term. It outlines how each payment gets divided between interest and principal repayment.

Biweekly amortization schedules apply to loans with payments made every other week, rather than monthly. With biweekly payments, there are 26 payment periods per year rather than 12. This increased payment frequency allows borrowers to pay down principal faster and reduce interest costs over the loan term.

Here’s an example biweekly amortization schedule for a $100,000 loan at 4% interest over 10 years:

Payment # | Payment Date | Beginning Balance | Interest | Principal | Total Payment | Ending Balance

Adding & Subtracting Time

Are you starting biweekly payments in a middle of a loan schedule?

- Common loan terms: Most home loans are structred as 30-year loans, which is 360 monthy payments. A 20-year loan is 240 monthly payments, A 15-year loan is 180 monthly payments, a 10-year loan is 120-monthly payments and 5 year loan is 60 monthly payments.

- Converting years to months: multiply the years in the loan term by 12.

- Payments made: If you do not know how much time you have remaining you can calculate the total number of payments in the initial loan term & then subtract how many payments you have already made. If you are 42 months into a 30-year (360 monthly payment) mortgage then you have 318 monthly payments remaining.

- Partial years: If you had 244 months remaining you could either enter 20 years and 4 months or 0 years and 244 months. If you enter both values they will be summed. For example, 1 year and 12 months will be added to 2 years.

Are you paying high interest rates on your debts? If so you may be able to take advantage of low personal loan rates, consolidate your debts using home equity, or refinance your Wilmington mortgage at todays low rates. Rate tables for various loan products are shown in the tabs below. Calculator Mortgage Heloc Personal Loans

| Loan Details | Amount |

|---|---|

| Principal balance owed: [?] | |

| Annual interest rate (APR): (Get Current Rates) | |

| Remaining loan term (years): | |

| Remaining loan term (months): |

| Monthly Payments | Amount |

|---|---|

| Monthly payment amount: | |

| Interest youll pay with monthly payments: |

| Biweekly Payments | Amount |

|---|---|

| Bi-weekly payment equivalent to monthly payment: | |

| Accelerated bi-weekly payment: | |

| Interest youll pay with accelerated bi-weekly payments: | |

| Bi-weekly savings: |

How Bi-Weekly Payments Work

The concept of a twice-monthly payment is a bit misleading. Bi-weekly is not the same as twice a month. There are 52 weeks in the year, which means that on a biweekly payment plan, you would make 26 payments per year. However, there are only 12 months in the year, and if you were making two payments each month, you would only be making 24 payments a year.

By making payments every other week, you are actually paying an additional loan payment each year. Therefore, if your monthly payment is $1,500 a month, you would pay $18,000 a year with monthly payments. If you made payments every other week, you would end up paying $19,500 for the year.

The primary advantage of more frequent payments is paying down your principal balance faster, reducing the amount of interest you pay and shaving years off your loan. For example, if you have a 30-year $250,000 mortgage at a 5 percent interest rate, you will pay $1,342.05 per month, not counting property taxes and insurance. You would pay $233,139.46 in interest over the life of the loan making the standard monthly payments. If you switched to a biweekly plan, you would pay only $189,734.44 in interest and will cut four years and nine months off the life of your loan. Depending on the terms of your loan, switching payment frequency could cut your loan by as much as eight years.

You dont necessarily have to pay every other week to get the savings. You can just divide your mortgage payment by 12 and add 1/12th the amount to your payment each month. Therefore, if your regular payment is $1,500 a month, you would pay $1,625 each month instead. Some people also use tax refunds, performance bonuses & other similar streams to help create a 13th yearly payment.

Make sure that any additional payments you make will be applied directly to the principal.

The same sort of benefits which happen on mortgages also apply to other forms of lending. Typically other loans have a shorter duration for interest to accrue, but they also typically come with higher interest rates. Cars depreciate quickly & unsecured loans have higher rates of interest to compensate for the risk of non-payment.

Unfortunately, switching may not be as simple as writing a check every two weeks. If you are already on an automatic payment plan, you will need to find out from your lender if you can cancel or change it. You will then need to find out if your lender will even accept biweekly payments, or if there is a penalty for paying off your loan early.

Some services offer to set up bi-weekly payments for you. However, these companies may charge you a fee for the service (as much as several hundred Dollars), and they may only make the payment on your behalf once a month (negating any savings).

Instead, you must make the payment directly to the lender yourself, and you must be sure that it will be applied right away and that the extra will be applied toward your principal.

As long as you have strong will, its better to make the payments directly instead of signing up for an automatic payment plan since it will give you more flexibility in case of lean times.

Use the above calculator to determine how much you can save by switching to bi-weekly mortgage payments. Youll also find out how much more quickly you can pay off your loan. Play with different amounts to see how much you can save by paying more each month.

Biweekly Mortgage Analysis

FAQ

How to calculate biweekly amortization?

How much faster will I pay off my loan with biweekly payments?

How to figure out biweekly payments?

How much do biweekly payments shorten a 20 year mortgage?

What is a biweekly mortgage calculator with amortization schedule?

Biweekly mortgage calculator with amortization schedule is a home loan calculator to calculate biweekly payments for your mortgage. The biweekly loan calculator has a biweekly amortization schedule excel that breaks down all the payment details.

Does the bi-weekly amortization calculator account for extra payments?

A3: It does not account for extra payments; consider adjusting the loan amount for such scenarios. The Bi-Weekly Amortization Calculator simplifies the complex process of loan payment calculations, providing users with valuable insights into their financial commitments.

What is the amortization schedule calculator?

Our amortization schedule calculator helps you to figure out the payment on a loan and provides you with the interest and principal breakdown per payment, as well as the annual interest, principal, and loan balance after each payment.

How do I calculate bi-weekly loan amortization?

Using the Bi-Weekly Amortization Calculator is straightforward. Input your loan details into the provided fields, click the “Calculate” button, and instantly receive detailed information about your bi-weekly loan payments. The formula used for bi-weekly loan amortization is: P=1−(1+r)−ntr⋅PV Where: t is the loan term in years.