Getting a mortgage is one of the biggest financial decisions you can make. With so many loan types and options to choose from, it can be overwhelming trying to determine the best fit for your needs. This is where using an all in one loan calculator can provide tremendous value.

In this article, we’ll look at what makes the all in one loan unique how its calculator works and how modeling different scenarios can help you identify the most favorable mortgage structure. Whether you want to pay off your home faster, access more liquidity, or simply save on interest, read on to see how this tool can help!

What Is an All In One Loan and How Is It Different?

An all in one loan combines a mortgage and home equity line of credit (HELOC) into a single lending product. This gives it some key advantages over regular mortgages:

-

Lower interest costs – Only charged interest on the amount you actually owe not the full loan amount.

-

Pay down principal faster – Apply deposits to immediately lower your principal.

-

Access home equity – Built-in HELOC provides liquidity and flexibility.

-

Works like a checking account – Make payments and transfers from the loan.

Having your mortgage and finances consolidated into one account provides opportunities for savings and convenience that separate loans don’t allow.

Benefits of Using an All In One Loan Calculator

With unique dynamics like these, modeling out your exact costs and terms requires a specialized all in one loan calculator. Here are some key benefits this tool provides:

-

Custom scenarios – Input your specific details to see personalized figures.

-

Payment projections – Review potential monthly payment amounts.

-

Total interest savings – See how much interest you can potentially save over the life of the loan.

-

Payoff comparisons – Compare how many fewer years to pay off principal.

-

What-if analysis – Easily adjust variables to model different options.

-

Shareable results – Email yourself scenarios to review later.

Having all this mortgage modeling capability in one place makes it easy to quantify the potential advantages of an all in one loan for your situation.

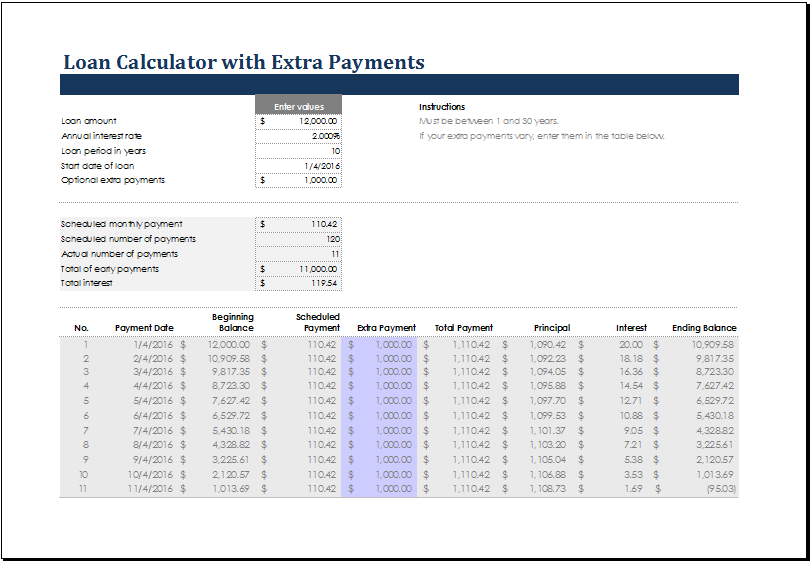

How an All In One Loan Calculator Works

These calculators take your inputs and financial data and use them to estimate:

- Monthly payments

- Total interest paid

- Years until payoff

- Lifetime savings

It runs these figures on both a standard mortgage and the all in one loan for an apples-to-apples comparison. This makes it easy to see how big of an impact consolidating into an all in one loan could have over the life of your mortgage.

Walkthrough of Using an All In One Loan Calculator

To give you a hands-on look at how these tools work, let’s walk through a hypothetical scenario:

Say you currently have a $200,000 mortgage at 4% interest, along with $40,000 in other debt like credit cards or student loans at 8% interest. You also typically have around $10,000 in your checking account earning little interest.

Here are the steps you might take to model your options with an all in one loan calculator:

-

Enter your current mortgage balance, rate, and terms.

-

Input your other debt amounts and rates.

-

Estimate your average checking account balance.

-

Review the total interest paid over time for each.

-

See the monthly payments for each option.

-

Check the lifetime savings from consolidating into an all in one loan.

-

Adjust variables like debt amounts, rates, etc. to model scenarios.

-

Email yourself the results for further review.

Running through exercises like this makes the potential money-saving benefits of an all in one loan much clearer tailored to your exact financial situation.

Key Factors to Model in an All In One Loan Calculator

As you use these calculators to explore mortgage scenarios, here are some of the key variables to adjust to understand their impact:

- Current mortgage balance

- Interest rate

- Loan term

- Payoff time frame

- Other debt amounts

- Checking account balances

- Credit profile factors

Seeing how these inputs change your estimated payments, interest costs, and payoff timing can illustrate how beneficial consolidating into an all in one loan could be.

Finding the Right All In One Loan Calculator

Now that you see how an all in one loan calculator can demystify this financing option, you probably want to try modeling some scenarios yourself. Here are a few tips on picking the right tool:

- Provides detailed side-by-side comparisons to standard loans.

- Allows input of your full financial picture, including other debts.

- Offers customized scenarios you can save and share.

- Includes helpful explanations and visuals about the all in one loan.

- Is mobile-friendly for use on all devices.

- Comes from a reputable all in one loan provider like CMG Financial.

The All In One Loan Calculator from CMG checks all those boxes, making it easy to quantify potential savings from this innovative lending option.

Take Control of Your Mortgage with Informed Modeling

Buying a home is emotional, but make sure you crunch the numbers too. An all in one loan calculator gives you the power to explore your mortgage objectively and quantitatively. This allows you to find potential cost savings and efficiency gains that work for your financial situation.

So rather than just going with the first mortgage you’re offered, take the time to model different scenarios with a specialized all in one loan calculator. Having personalized simulations at your fingertips makes it easy to feel confident you’ve found the optimal home financing solution.

Home financing & personal banking combined into one simple tool

The following examples are based on results from the All In One Loan Simulator, an interactive mortgage calculator. All examples are hypothetical and for illustrative purposes only. The quoted rates do not include origination fees and other lender fees, points, third-party closing costs, taxes and government fees, and prepaid expenses and deposits. Any rates quoted on the examples are not annual percentage rates. Rates used in the examples are based on historical averages and do not reflect currently available rates. The savings quoted are estimates and not guaranteed. Your HELOC disclosure and brochure will provide the actual rates, terms and fees associated with the All In One Loan.

The example below is based on $10,000 in monthly deposits to your AIO checking account and $6,000 in monthly withdrawals.

*Projected interest savings and time to payoff depend on the starting amount of the HELOC at account opening , annual percentage rate, APR rate environment, checking account deposit and withdrawal activity. Actual results may vary for a variety of reasons and may result in less interest savings and a longer time to payoff.

Example of 80% LTV (20% cash down) 30-Year Conventional Loan Program with $700,000 sale price. $560,000 loan amount, $140,000 cash down payment, 30-year fixed rate loan with zero points. 360 monthly payments of $4,157.98 each (P&I only). Monthly payments do not include required mortgage insurance, taxes, insurance premiums or other applicable escrows. Actual payment amount will be higher. Example assumes 740 credit score. Interest rate is 8.125%, APR 8.162%. Rates as of April 3, 2024.

The All In One® Home Equity Line of Credit (AIO HELOC) is a variable rate, 30-year, home equity line of credit (HELOC) combined with a Northpointe Bank checking account and secured by a first lien on residential real property. The APR changes monthly based on the 1-Year Treasury Rate (CMT) Index plus a margin. Example of an AIO HELOC with a line amount of $560,000 at opening with APR of 9.003% has an average minimum monthly payment of $2,345.65. Example assumes an owner-occupied primary or second residence with 80% LTV and 740 credit score. Rate will not exceed 15.003% APR. Annual fee of $60 after the first year or other amount as permitted by state law. Property insurance required. Borrower is responsible for doc stamps, intangible tax, transfer tax, recording tax and mortgage tax, if applicable. Rates as of April 3, 2024.

All loans are subject to credit review and approval. This is not a commitment to lend. Rates, fees, other charges and terms subject to change. Available loan programs and terms will vary by state. Other terms and conditions may apply.

All In One Loan is a registered trademark of CMG Financial Services.

HOW & WHY the ALL IN ONE Loan Works

FAQ

What is the downside of an all in one loan?

How do you calculate all in cost of a loan?

What is the monthly payment on a $50,000 HELOC?

How much would a $5000 personal loan cost?

|

Interest rate

|

Monthly payment

|

Total interest

|

|

8 percent

|

$157

|

$640.55

|

|

12 percent

|

$166

|

$978.58

|

|

16 percent

|

$176

|

$1,328.27

|

What is an all in one loan?

Mortgage interest can be one of life’s biggest financial obstructions. The All In One Loan was developed by homeowners and mortgage professionals as a solution. By combining banking functionality with home financing into one dynamic instrument, borrowers are able to save tens of thousands of dollars and years off their loan.

What is a loan calculator?

This loan calculator will help you know how much money you have to pay each month with interest. For example, if you want to buy a product, the total value of this product is X and there is a Y % interest rate.

How much does an all-in-one mortgage cost?

All-In-One Mortgages require a FICO score of 700+ with an annual fee that ranges from $50-$100 depending on your creditworthiness. You can get up to 30 years at an adjustable mortgage rate. They usually have higher APR rates than traditional mortgages.

What is the difference between an all-in-one mortgage and a HELOC?

HELOCs have a variable interest rate and the HELOC balance will fluctuate. The All-In-One Mortgage offers an adjustable interest rate to keep your payments fixed, even as rates change or you make additional principal payments. If you need to access money in case of emergency you don’t have to apply for a new loan.