If you’re looking to build your dream home from the ground up a construction to permanent loan can be a great financing option. With this type of loan you get a single loan to cover both the construction phase and the permanent mortgage once the home is completed. But before you can get approved, you’ll need to meet certain requirements.

In this comprehensive guide, we’ll walk through all the key eligibility criteria lenders look for with construction to permanent loans. We’ll also provide tips for boosting your chances of qualifying. Whether you’re just starting your research or are ready to apply, read on to learn all the construction to permanent loan requirements you should be aware of.

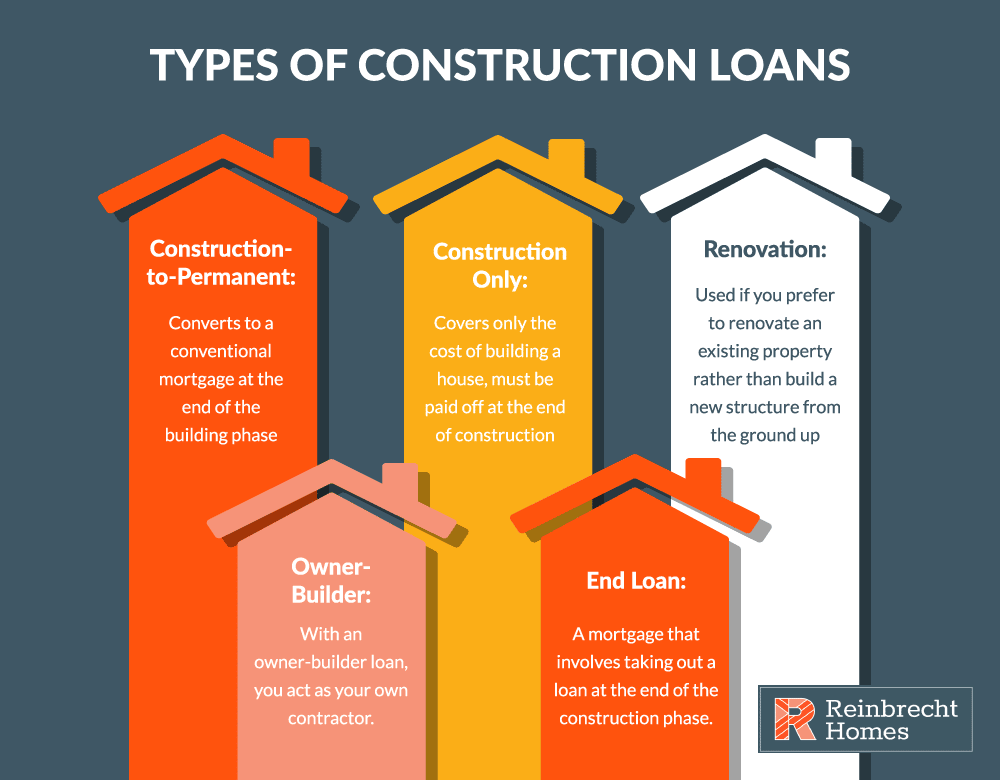

Overview of Construction to Permanent Loans

Before diving into the specific requirements, let’s quickly review how construction to permanent loans work.

With a construction to permanent loan, you get a single loan that converts from the construction phase to a permanent mortgage once building is finished. This avoids the need to take out a separate construction loan and permanent mortgage.

During construction, you’ll only pay interest on the money that’s been drawn to pay builders. The rate may be fixed or adjustable. Then once the home is move-in ready, the loan converts to a fixed-rate permanent mortgage amortized over 15 to 30 years typically.

Construction to permanent loans allow for a streamlined process since you only go through closing once. But you may face stricter eligibility standards compared to getting a construction loan and mortgage separately.

Down Payment Requirements

One key requirement for construction to permanent loans is the down payment. Many lenders want borrowers to make a down payment of at least 20% of the home’s projected value once completed. Some may require as much as 25% or even 30% down.

The reason behind the large down payment requirement is risk. Construction loans are riskier than mortgages on existing homes. Requiring more money down helps offset the chance you fail to complete the project or default on the loan.

Coming up with a 20-30% down payment can be a challenge. For a $400,000 home construction project, you’d need between $80,000 and $120,000 available. Here are some tips for funding a large down payment:

- Save aggressively for your down payment over several years

- Limit spending to direct more cash toward savings

- Ask family members for a down payment gift

- Withdraw funds from your retirement savings

- Use equity from an existing home you sell

Aim to have your down payment ready before applying since lenders want to see you have the funds available upfront.

Credit Score Requirements

Your credit score is another important eligibility factor for construction to permanent loans. Many lenders look for a minimum score of 620 to 640. But you’ll have much better odds if your score is 720 or above.

Here are some tips for boosting your credit score to improve approval odds:

- Pay all bills on time each month

- Pay down balances on credit cards and other debt

- Avoid new credit inquiries by only applying for loans sparingly

- Check credit reports for errors and dispute any inaccuracies

Having a cosigner with excellent credit can help too. Their higher score gets taken into account when applying.

Debt-to-Income Ratio Limits

Lenders also look closely at your debt-to-income ratio or DTI when reviewing a construction to permanent loan application. DTI compares your total monthly debt payments to your gross monthly income.

Many lenders cap DTIs around 43% for this type of loan. But the lower your DTI, the better. You may need a ratio below 36% to get approved if you have other risk factors like a low down payment or credit score.

Follow these tips to lower your DTI before applying:

- Pay off smaller debts to reduce monthly payments

- Avoid taking on new loans or lines of credit

- Ask creditors for lower interest rates to save on payments

- Boost your income with a side gig or promotion at work

Keeping housing expenses reasonable for your income is also key. Don’t overbuild relative to your budget.

Loan Eligibility Requirements

Beyond your finances, lenders also place requirements around the loan itself and property you wish to build on. Here are some of the key eligibility criteria to be aware of.

Loan Amount

Lenders will cap the maximum they’ll lend based on factors like your income, existing assets and credit profile. Many max out loan amounts at $750,000 but some may go higher. Applying with a cosigner can allow you to qualify for a larger construction loan amount too.

Inspections

You may need to pay for multiple inspections during the build. This includes soil tests, surveys, appraisals and more. Be prepared to cover these costs.

Home Type

Most lenders limit construction to permanent loans to single-family home builds only. So you may not be able to get this type of financing for a duplex, triplex or other multi-family property.

Primary Residence

Lenders typically require you to use the home as a primary residence once completed, rather than an investment property you rent out.

Licensed Builder

You’ll need to use a licensed, bonded general contractor for construction. Lenders want to see they are legitimately in business.

Building Plans

Your lender will require you to provide detailed building plans upfront before approving the loan. Blueprints may also be needed.

Tips for Securing a Construction Loan

If you want the best shot at getting approved, keep these tips in mind:

-

Shop with multiple lenders to compare terms and requirements. Aim for the one with the most lenient eligibility criteria you can qualify for.

-

Ask the lender what specifics they look for in terms of credit score, income, loan amount, down payment percentage, etc. so you can prepare adequately.

-

Have all your financial paperwork in order, including bank statements, tax returns, income documentation and credit reports.

-

Be conservative with the loan amount. Don’t max out what you may qualify for. Leave some wiggle room.

-

Keep your debt-to-income ratio on the lower side if possible.

-

Consider using a cosigner if you’re light on income or have existing debt.

-

Highlight any assets beyond the down payment you can use as collateral or reserves.

Meeting all the requirements for a construction to permanent loan can be challenging. But taking the time to prepare your finances and put together a strong application is worth the effort. With an affordable down payment, excellent credit, and sensible loan amount, you can make your dream of building your own home a reality.

Example of All-in-One Loan

Weve got two common scenarios to illustrate how this works. Keep in mind that these are intended to give you a general idea of how an All-in-One Loan works, and actual underwriting is based on loan to value (LTV) which is then based on the lesser of either the appraised value or the acquisition costs. The maximum LTV on primary home is 80%. Now for the examples:

- Borrower 1 owns a building lot worth $275,000 free and clear. They wish to build a new home for $450,000. The total acquisition cost would be $725,000 ($275,000 + $450,000). WaFd will lend 80% of the acquisition cost, in this case $580,000, which is more than the borrower needs to build the home, since they only need to borrow $450,000.

- Borrower 2 owns a building lot worth $175,000 with a loan balance of $85,000 remaining. The cost to construct a new home is $375,000. The total acquisition cost is $550,000 ($175,000 + $375,000). 80% of the acquisition cost is $440,000, which is enough to cover the cost of building the new home. However, the existing lot loan must be paid off at closing, and after setting aside the $375,000 to build the home there is only $65,000 remaining in the new loan, so the borrower will need to pay $20,000 at closing.

Every situation is different, so its important to do the math to find out if a WaFd Banks construction to permanent loan is right for you. Our friendly neighborhood loan officers are great at math and are more than happy to crunch the numbers for you. You can also check out WaFd Banks custom construction loan rates and use our construction loan calculator to get an idea of what your payment might look like.

How is WaFd Bank a Unique Lender for All-in-One Loans

Many banks that offer construction financing do so in two steps. The first loan covers construction only. After that, youll need a second, permanent mortgage loan which will require two closings and two sets of fees. If these lenders do not offer one interest rate at the start of construction through the completion of your home and after youve moved in, you may need to plan for fluctuations in interest rates. Mortgage rates may increase before your home is finished which puts pressure on the ability to afford your payments once your home is complete. You might also have to deal with a second application process and even a second appraisal at the completion of your home, depending on your lenders requirements. At WaFd, the construction and permanent financing are rolled into one loan with one permanent rate. Plus, WaFd is a portfolio lender, which means your loan will never be sold and youll always know who to go to with questions.

Construction to Permanent Loan Advantages & How They Work | WaFd Bank

FAQ

What is the primary disadvantage of a construction permanent loan?

How does construction to perm loan work?

Is a construction loan harder to get than a mortgage?

What is the minimum FICO score for a construction loan?

What are the requirements for a construction-to-permanent loan?

Since there’s more risk involved with building a home, lenders typically have more stringent requirements for construction-to-permanent loans. Along with having your finances in order, you’ll need to submit detailed plans and work with approved professionals. Here are the typical requirements:

What is a construction to permanent loan?

Construction to permanent loans eliminate the need for two different loans. Instead, you get a single loan to purchase the land and build the home that will convert to a permanent mortgage when construction is complete. Loan terms usually range from 15 to 30 years and have fixed interest rates, similar to other types of mortgage loans.

Where can I get a construction-to-permanent loan?

Many types of lenders offer construction-to-permanent loans, but you’ll most often find them at a bank or with a lender that specializes in construction financing. What is a construction-to-permanent loan?

What is a construction-to-permanent mortgage?

Once the home is built, the loan converts into a traditional mortgage, usually with a 15- or 30-year term. Conventional construction-to-permanent loans can have fewer restrictions than government-backed loans.