When taking out a personal loan, you’ll likely encounter something called a finance charge As a personal finance blogger, I want to provide a detailed explanation of what exactly a personal loan finance charge is, the different fees that comprise it, and why it’s an important factor when shopping for a personal loan.

What is a Personal Loan Finance Charge?

Simply put, a personal loan finance charge is the total cost of borrowing money through a personal loan. It includes interest and fees charged by the lender. Personal loan lenders use finance charges to generate revenue from lending money to borrowers like you and me.

Finance charges allow lenders to profit from personal loans so they can continue offering them to consumers. As a borrower, it’s key to understand what fees make up a finance charge so you can compare loan options accurately.

Common Personal Loan Finance Charges

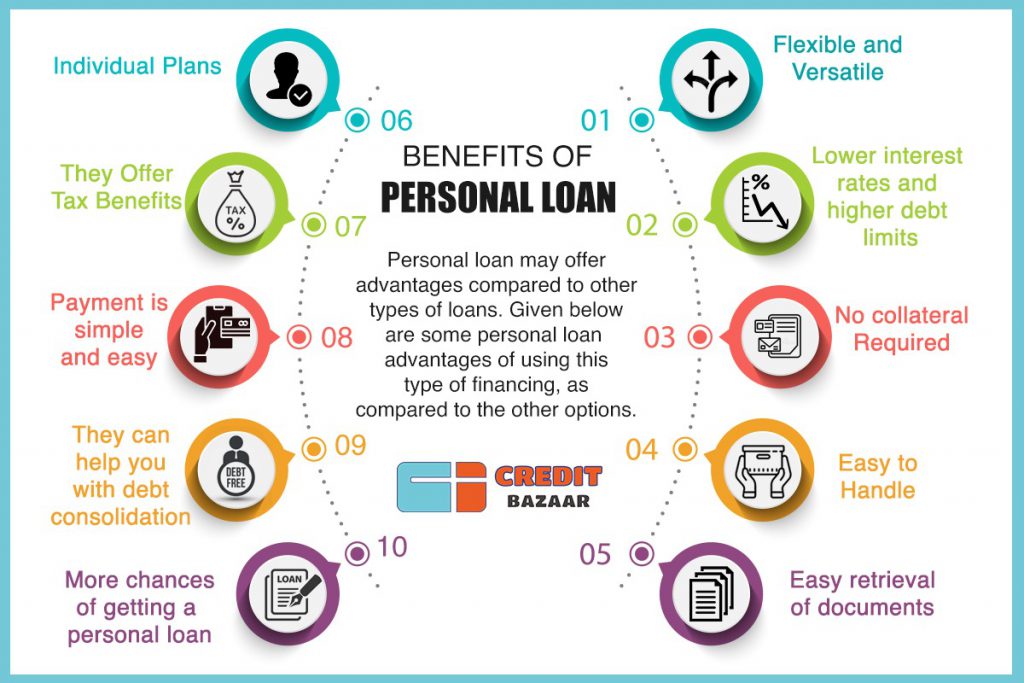

There are several different fees that commonly factor into a personal loan’s finance charge:

-

Origination fee – This upfront fee covers processing costs for originating your loan It’s usually 1-5% of the loan amount

-

Interest rates – The ongoing interest rate charged on the loan balance is part of the finance charge Interest rates vary based on your credit

-

Late fees – If you miss a payment, you may be hit with a late fee, often $25-50.

-

Prepayment penalties – Paying your loan off early may incur a prepayment penalty fee. Not all lenders charge this.

-

Annual Percentage Rate (APR) – The APR represents the total yearly cost of the loan, including interest and fees.Aim for the lowest APR when comparing loan offers.

As you can see, the specific composition of a personal loan finance charge can vary. It’s always wise to ask lenders to explain exactly what their finance charge includes before committing to a loan.

Why Personal Loan Finance Charges Matter

Now that you understand what a personal loan finance charge consists of, you may be wondering why it even matters to you as a borrower. Here are two key reasons:

-

Compare loan costs accurately – The finance charge gives you the full picture of how much a loan will cost in interest and fees. This allows you to accurately compare personal loan offers.

-

Avoid surprises – Knowing what fees comprise the finance charge helps avoid surprise costs after taking out the loan. You’ll know what to expect.

The bottom line is understanding personal loan finance charges makes you a savvier, more informed borrower. You can detect which lenders charge sneaky, hidden fees versus those that offer straightforward pricing.

Tips for Minimizing Personal Loan Finance Charges

As a personal finance blogger, I’m always looking for ways to save money on borrowing costs. Here are some tips to minimize personal loan finance charges:

-

Compare multiple lenders – Rates and fees vary, so shop around to find the most affordable loan. Online lenders like Rocket Loans often offer low rates.

-

Boost your credit – A higher credit score can qualify you for a lower interest rate, reducing your finance charge.

-

Shorten the repayment term – Choose a shorter loan term, which cuts down on interest costs over the life of the loan.

-

Pay early – Make extra payments when possible to pay off the balance quicker and reduce your finance charge.

-

Use autopay – Enrolling in autopay may score you a slight interest rate reduction with some lenders.

Follow these tips, and you’ll be on your way to reducing personal loan finance costs!

How to Calculate a Personal Loan Finance Charge

To get your exact personal loan finance charge amount, you’ll need to do a little math. Here’s a simple formula you can use:

Total finance charge = Total loan payments – Principal loan amount

Let’s look at an example:

- You take out a $10,000 personal loan

- The loan term is 3 years (36 months)

- Your monthly payment is $304

To find the finance charge:

-

Monthly payment ($304) x Number of months (36) = Total payments ($10,944)

-

Total payments ($10,944) – Principal amount ($10,000) = Total finance charge ($944)

So for this loan, your total finance charge is $944. Pretty simple, right? Knowing how to calculate this helps you determine just how much a personal loan will truly cost in fees.

Closing Thoughts

Being aware of them allows you to accurately compare loan options to find the most affordable financing for your needs. And you can use the tips and formula provided to minimize your personal loan finance charges.

At the end of the day, knowledge is power when it comes to managing personal finances and borrowing wisely. So the next time you need a personal loan, make sure you ask lenders to break down their finance charges so you can make the optimal decision.

What is a Finance Charge?

A finance charge refers to any cost related to borrowing money, obtaining credit, or paying off loan obligations. It is, in short, the cost that an individual, company, or other entity incurs by borrowing money. Any amount that a borrower needs to pay in addition to paying back the actual money borrowed qualifies as a finance charge.

The most common type of finance charge is the amount of interest charged on the amount of money borrowed. However, finance charges also include any other fees related to borrowing, such as late fees, account maintenance fees, or the annual fee charged for holding a credit card.

- A finance charge refers to any type of cost that is incurred by borrowing money.

- Finance charges exist in the form of a percentage fee, such as annual interest, or as a flat fee, such as a transaction fee or account maintenance fee.

- Consumers with long-term loans – such as an auto loan or mortgage – can significantly reduce the total amount of finance charges in the form of interest by making additional payments to reduce the outstanding balance on the principal loan amount.

Banks, credit card companies, and other financial institutions that lend money or extend credit are in business to make a profit. Finance charges are the primary source of income for such business entities. Such charges are assessed against loans, lines of credit, credit cards, and any other type of financing.

Finance charges may be levied as a percentage amount of any outstanding loan balance. The interest charged for borrowing money is most often a percentage of the amount borrowed. The total amount of interest charged on a large, long-term loan – such as a home mortgage – can add up to a considerable amount, even more than the amount of money borrowed.

For example, at the end of a 30-year mortgage loan of $132,000, paid off on schedule, carrying a 7% interest rate, the homeowner will have paid $184,000 in interest charges – more than $50,000 more than the $132,000 principal loan amount.

Other finance charges are assessed as a flat fee. These types of finance charges include things such as annual fees for credit cards, account maintenance fees, late fees charged for making loan or credit card payments past the due date, and account transaction fees. An example of a transaction fee is a fee charged for using an automated teller machine (ATM) that is outside of the bank’s network.

Transaction fees may also be charged for exceeding the maximum allowable monthly number of transactions in a bank or credit union account. For instance, some checking accounts allow the holder only ten free transactions per month. Every transaction over the ten-transaction monthly limit incurs a transaction fee.

Finance charges that may be calculated as a percentage of the loan amount or that may be charged as a flat fee include charges such as loan application fees, loan origination fees, and account setup fees.

The finance charges that a borrower may be subject to depend a great deal on their creditworthiness as determined by the lender. The borrowers’ credit score at the time of financing is usually the primary determinant of the interest rate they will be charged on the money they borrow.

How to Save Money on Finance Charges

As noted in our example of a 30-year mortgage loan above, the finance charges on borrowed money can eventually add up to a sum even greater than the amount of money borrowed. Credit cards with high interest rates can end up costing much more in finance charges than the amount of credit utilized.

So, how can one save money on finance charges? With credit cards, the easiest way to save money is by paying off the full outstanding balance on the customer’s credit card bill each month. By doing that, the borrower avoids interest charges entirely and only need to pay finance charges such as annual fees. If they’re unable to pay the full balance, they can still save a considerable amount in interest charges by at least paying more than the required minimum payment for each month.

Similarly, homeowners with mortgage loans or individuals with auto loans can save a lot of money in finance charges by making extra payments on the principal loan amount with each monthly payment. For example, if their mortgage payment is $850 per month, they can send a payment of $1,000 to your lender each month, designating the extra $150 as an “additional payment to the principal loan amount.”

It not only reduces the outstanding loan balance by more each month – thus, reducing the amount of interest charged in the future – it would also lead to seeing the loan completely paid off much earlier than scheduled.

CFI is the official provider of the Commercial Banking & Credit Analyst (CBCA)™ certification program, designed to transform anyone into a world-class financial analyst.

In order to help you become a world-class financial analyst and advance your career to your fullest potential, these additional resources will be very helpful:

- Share this article

What Is A Finance Charge On A Loan?

FAQ

What is a finance charge in a personal loan?

How can I avoid finance charges on my personal loan?

Why am I getting a finance charge?

How much should a finance charge be?

What is a loan finance charge?

A loan finance charge can be a one-time fee, like an origination fee, or a recurring fee, like interest rates. It could be charged as a flat fee, or a percentage-based fee, like APR. There are multiple types of finance charges that may apply to a loan. They include: If you pay off a loan early, some lenders charge fees called prepayment penalties.

What is a personal loan finance charge?

One type of personal loan finance charge is the interest rate, which is a percentage of your principal loan amount. It’s the amount of money you’re charged for the loan. Interest rates can be variable or fixed. Variable interest rates can change over the course of the loan, while fixed interest rates stay the same.

What types of Finance Charges apply to a loan?

There are multiple types of finance charges that may apply to a loan. They include: If you pay off a loan early, some lenders charge fees called prepayment penalties. The reason: When a borrower pays a loan in full before the end of the loan term, the lender loses money on interest charges. Not all lenders charge prepayment penalties.

What are finance charges?

Finance charges are a form of compensation to the lender for providing the funds, or extending credit, to a borrower. These charges can include one-time fees, such as an origination fee on a loan, or interest payments, which can amortize on a monthly or daily basis. Finance charges can vary from product to product or lender to lender.