Conventional mortgages are the most common type of home loan in the United States and usually offer the best overall deal for borrowers who qualify for one. If youâre ready to buy a home, itâs important to know how conventional loans work, the pros and cons of this mortgage type, and how to get one.

The debt-to-income ratio (DTI) is one of the most important factors lenders consider when approving borrowers for a conventional mortgage. Your DTI compares how much debt you have to your income giving lenders a clear picture of your ability to manage mortgage payments. DTI requirements can vary based on your specific financial situation but generally fall within a range of 36% to 50%.

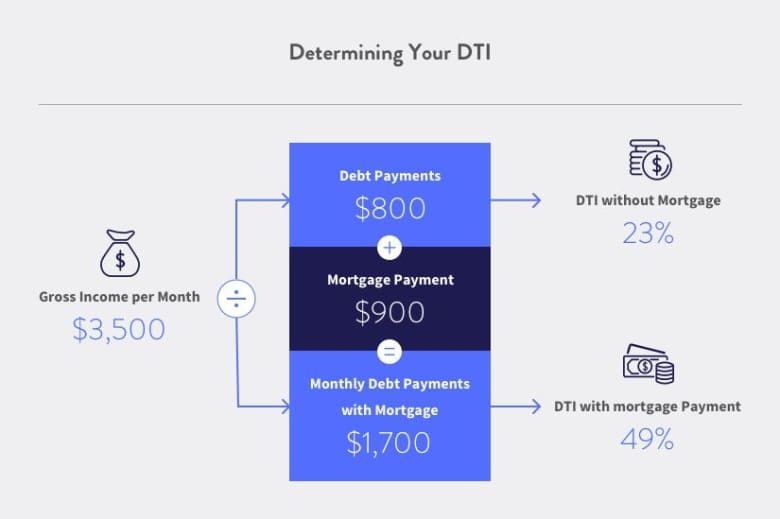

What is DTI and How is it Calculated?

Your debt-to-income ratio compares the amount of debt you have compared to your gross monthly income It’s calculated by dividing your total monthly debt payments by your total monthly gross income

For example:

- Monthly debt payments (mortgage, credit cards, auto loans, student loans etc): $2,000

- Gross monthly income: $5,000

- DTI = Monthly Debt Payments / Gross Monthly Income

- DTI = $2,000 / $5,000 = 40%

A lower DTI percentage is better, indicating you have more available income to put towards housing expenses.

Why DTI Matters for Mortgage Approval

Lenders want to make sure you have enough income to comfortably make your mortgage payment each month. Your DTI gives them a standardized way to measure your existing debts and gauge if you can manage additional housing debt.

In general, the lower your DTI ratio, the easier it will be to get approved. But maximum DTI limits can vary between lenders.

Conventional Loan DTI Limits

For conventional loans in 2023 here are some general DTI requirements to expect

-

DTI up to 36% – You’re in great shape if your total DTI is 36% or lower. Lenders like to see DTIs at 36% or less. This DTI range qualifies for the very best interest rates.

-

DTI 36% to 45% – Many lenders will approve DTIs in this range, but you may not qualify for the lowest interest rates. You’ll likely need good credit and substantial assets to be approved.

-

DTI 45% to 50% – Getting financing above 45% can be challenging but is possible. Strong compensating factors like excellent credit, large down payment and cash reserves are typically required. Maximum DTI varies by lender.

-

DTI above 50% – It will be very difficult to get approved with a debt-to-income level over 50%. You’ll need stellar credit and a large down payment to have a chance at approval.

As you can see, it’s ideal to have your DTI below 36% when applying for a conventional mortgage. But even with a higher DTI, approval is possible with other positive factors in your application.

Components of DTI

When calculating your debt-to-income ratio, lenders look at two main components:

Monthly Housing Expenses

- This includes your proposed principal and interest mortgage payment. Real estate taxes, insurance, HOA fees, and other housing expenses are sometimes included.

Monthly Debt Payments

- All recurring monthly debts like credit cards, auto loans, student loans, alimony, child support etc. Minimum required payments are used.

Debt payments do NOT include utilities, groceries, gasoline, childcare, and other flexible living expenses.

How to Improve Your DTI

If your DTI is too high, here are some strategies to improve it before applying:

-

Pay down revolving debts – Paying off credit cards and personal lines of credit can quickly lower your DTI. Pay down balances as much as possible.

-

Pay extra on installment loans – Consider paying more than the monthly minimum on auto loans and student loans to pay them off faster.

-

Consolidate debts – Combine multiple payments through a debt consolidation loan or balance transfer credit card with a lower monthly payment.

-

Increase income – Take on a side job or freelance work to increase your gross monthly income used in the DTI calculation.

-

Remove authorized user accounts – If you’re an authorized user on someone else’s high balance card, have yourself removed to stop counting against your DTI.

-

Sell assets – Consider selling assets like boats, ATVs, motorcycles, and cars you no longer need to eliminate associated loans and insurance payments.

With a lower DTI, you’ll have an easier time qualifying for a conventional mortgage or get approved for a lower interest rate potentially saving thousands.

Manual Underwriting DTI Requirements

Most conventional mortgages today use automated underwriting through Fannie Mae’s Desktop Underwriter (DU) or Freddie Mac’s Loan Product Advisor (LPA) systems. This allows customized DTI requirements based on your overall financial profile including assets and credit history.

But some lenders still manually underwrite conventional loans without automated underwriting. In these cases, more strict DTI limits apply:

-

Maximum DTI of 36% – Manually underwritten conventional loans require a maximum DTI of 36% for the best pricing.

-

DTI up to 45% allowed – DTIs above 36% are permitted but will have higher interest rates. Compensating factors are required for approval.

-

DTI above 45% typically not permitted for manual underwriting.

The manual underwriting DTI limits highlight the importance of keeping your DTI at 36% or lower when possible.

Low Down Payment Programs and DTI

Many conventional loans allow down payments as low as 3% which helps first-time home buyers. But low down payment programs like conventional 97 loans do have stricter DTI requirements versus a 20% down conventional mortgage.

Here are some DTI variances based on your down payment amount:

-

20% down – Max DTI typically 45% to 50%

-

10% down – Max DTI typically 43% to 45%

-

5% down – Max DTI typically 41% to 43%

-

3% down – Max DTI typically 38% to 41%

To qualify for a low down payment conventional loan, focus on keeping your DTI on the lower side.

The Bottom Line

It’s important to understand DTI requirements and take steps to reduce your ratio before applying for a conventional mortgage. A DTI of 36% or lower gives you the best shot at approval and the lowest interest rate. But responsible borrowers can still qualify with DTIs up to 50% in some cases.

Knowing the DTI standards and making improvements to stay within those ranges will set you up for success to become a homeowner.

Conventional loans vs. USDA loans

The U.S. Department of Agriculture offers loans for low- and mid-income borrowers who want to buy a home in an eligible rural area.

Compared to conventional loans, USDA loans limit how funds can be used and require borrowers to meet income eligibility standards. Borrowers also must pay an upfront guarantee fee and an annual guarantee fee. However, USDA loans have no down payment requirement, which means they can be a good option for qualified borrowers with little savings.

Disadvantages of a conventional mortgage

- Stricter credit score requirement. Conventional loans generally require a higher minimum credit score compared with mortgages backed by government programs.

- Higher down payment requirement. To get a conventional loan, you need a down payment of at least 3%. Some government-backed loans allow borrowers to make a smaller down payment or no down payment at all.

- PMI requirement. You can expect PMI to cost $30 to $70 per month for every $100,000 you borrow. If you canât afford to put down 20%, then PMI will be an additional expense to pay until you reach 20% equity in your home.

Conventional Loans: Debt-to-Income (DTI) Ratio

FAQ

What is the conventional debt-to-income ratio for 2023?

What is the DTI limit for a conventional loan?

What is the DTI limit for a conventional loan in 2024?

Can you do a conventional loan with 5% down?

What is a good DTI ratio for a loan?

For a conventional loan, lenders prefer a DTI ratio under 36 percent. However, DTIs up to 43% are commonly allowed. In certain cases, you may even qualify with a DTI as high as 45-50%, if you have “compensating factors.” These factors could include a high credit score or significant cash reserves held in the bank.

What are the DTI requirements for a conventional loan?

There’s no single set of requirements for conventional loans. The DTI eligibility requirement typically depends on a borrower’s finances, credit history and loan type. Generally, borrowers need a DTI of 50% or less to qualify for a conventional loan. If your DTI is high, you’ll need to offset your debt with high cash reserves to secure a loan.

What is the maximum allowable DTI ratio?

The maximum can be exceeded up to 45% if the borrower meets the credit score and reserve requirements reflected in the Eligibility Matrix. For loan casefiles underwritten through DU, the maximum allowable DTI ratio is 50%. See B3-1-01, Comprehensive Risk Assessment for information about the DTI.

What does DTI mean on a mortgage?

DTI compares your total monthly debts (including mortgage costs) to your gross monthly income. Your lender uses DTI to determine how much a mortgage fits within your monthly budget. Many lenders want this ratio to be less or equal to 36% of the borrower’s income. However, conventional loans may allow a DTI as high as 49%.

Should DTI ratio be recalculated outside of du?

For DU loan casefiles, the DTI ratio should be recalculated outside of DU. If the recalculated DTI ratio exceeds 45% for a manually underwritten loan or 50% for a DU loan casefile, the loan is not eligible for delivery to Fannie Mae.

What is Fannie Mae’s DTI ratio?

The DTI ratio consists of two components: total monthly income of all borrowers, to the extent the income is used to qualify for the mortgage (see Chapter B3–3, Income Assessment). For manually underwritten loans, Fannie Mae’s maximum total DTI ratio is 36% of the borrower’s stable monthly income.