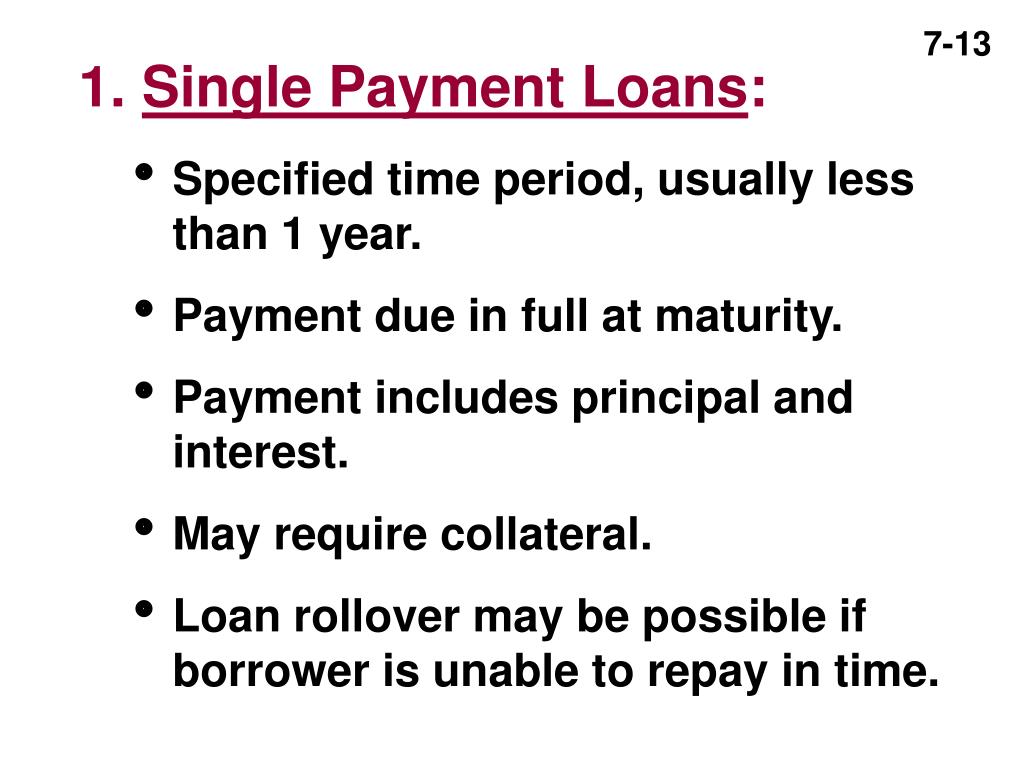

A single-payment loan requires the borrower to repay the entire principal balance and the interest in one lump sum on the due date.

The Ins and Outs of Secured Single-Payment Loans

Single-payment loans allow borrowers to get a lump sum of cash that must be repaid in full by a specific due date. These loans can provide fast access to funds but they also come with risks like high interest rates and fees. One defining feature of most single-payment loans is that they are secured loans meaning collateral is required.

As a financial writer trying to help readers make wise borrowing choices, I wanted to share an in-depth look at how securing a loan works, the assets that can be used as collateral, and the pros and cons of secured single-payment lending

What Does It Mean for a Loan To Be Secured?

When a loan is secured, the borrower pledges an asset they own as collateral for the debt. This collateral gives the lender recourse if the borrower defaults on the loan. The lender can seize and sell the collateral to recover their losses in the case of nonpayment.

Secured loans are tied to assets like:

-

Real estate – The home itself acts as collateral for mortgages.

-

Vehicles – The car, truck, motorcycle, etc. serves as collateral for auto loans.

-

Savings/Investment accounts – The funds in the account secure the debt.

-

Other valuable property like jewelry, art, or equipment.

The asset used for collateral must have sufficient value to secure the loan amount. Lenders want the asset’s resale value to cover the balance due if they must repossess and sell it.

Why Secured Loans Are Less Risky for Lenders

Lending money always involves some risk that the borrower will default. With unsecured loans, the lender has no recourse other than attempting to collect on the debt. This provides motivation for lenders to thoroughly vet borrowers’ creditworthiness and ability to repay before approving unsecured loans.

Conversely, secured loans give lenders a safety net – the valuable collateral pledged by the borrower. Even borrowers with poor credit may be approved for secured debt since the collateral reduces the lender’s risk.

According to research, most single-payment loans are secured loans rather than unsecured. This is likely because the single lump sum payment requirement amplifies risk for the lender. Adding collateral protection allows lenders to provide these risky, short-term loans that must be repaid in one shot.

The Pros of Secured Single-Payment Loans

Secured loans have advantages for both the lender and borrower in some situations.

For lenders

- Collateral reduces risk of default losses

- Interest rates and fees can be lower than unsecured alternatives

- Loan approvals can be quicker with less stringent credit checks

For borrowers

- Those with poor credit may qualify more easily

- Interest rates may be lower than unsecured options

- Quick access to a lump sum of funds when needed

Of course, pledging an asset you own as collateral is not without risk. Borrowers should carefully weigh the pros and cons before taking out a secured loan.

The Potential Downsides of Secured Single-Payment Loans

While secured lending has its place, these types of loans can be problematic when used for the wrong purposes. Here are some key disadvantages to weigh:

-

Risk of repossession – Defaulting leads to seizure of your pledged asset. You can lose your car, home, or other collateral.

-

Short repayment term – The single lump sum payment schedule can strain finances. Can you realistically repay in full that quickly?

-

High costs – Even with security, short-term loans often have very high APRs and fees. Read the fine print.

-

Credit damage if unpaid – Secured loans still appear on your credit reports. Default hurts your credit score.

-

Predatory lending practices – Some lenders exploit naive borrowers and place collateral at risk unfairly. Avoid lender tricks and traps.

Because of these concerns, secured short-term loans are best limited to true financial emergencies that leave you no other options. They are not wise for recurring expenses or nonessential purchases. Be a well-informed borrower.

Common Assets Used as Collateral

While any valuable item could theoretically be used to secure a loan, some specific assets are more commonly leveraged.

Vehicles – Cars, trucks, motorcycles, RVs. Auto loans are a prime example. The vehicle’s title is signed over until the loan balance is repaid.

Real estate – Your home or land can secure mortgage and home equity loans or lines of credit. The property acts as collateral.

Savings accounts – Some lenders allow savings account balances to secure personal loans. Your money serves as the collateral.

Equipment – Businesses often secure loans against expensive equipment, machinery, tools, and other assets.

Jewelry and art – While less common, high-value jewelry, paintings, collectibles may secure some personal or business loans.

The key is picking an asset with sufficient value compared to the loan amount. Lenders want to minimize losses in a default scenario.

Alternatives to High-Cost Secured Loans

Secured short-term loans often have exorbitantly high costs and risky terms. Before resorting to options like payday loans or auto title loans, exhaust other alternatives first:

-

Borrow from family or friends – If possible, get a zero-interest loan from loved ones and repay them.

-

Use available credit – Consider a credit card or personal line of credit if you have one.

-

Payment plans – Some service providers will break bills into installments.

-

Traditional personal bank loans – These give longer repayment terms and lower rates.

-

Employer advances – Some companies offer pay advances in a bind.

The bottom line? Secured lending has valid uses when done responsibly. But secured short-term loans should be a very last resort for emergencies only after exploring smarter alternatives. Prioritize your financial health and credit standing while still getting the funds you need.

The Basics: Your Credit History

Before we talk more about borrowing money, we need to discuss a topic that is crucial to the whole process. Credit history is one of the crucial ways lenders and creditors assess how responsible you are with your financial obligations. The better your credit history and higher your credit score, the more likely you are to get approved for a loan with the most favorable interest rates, possibly resulting in a lower monthly payment. Before borrowing money, it’s important to know what it means to be fiscally responsible and to understand how credit scoring works.

What Is A Single-payment Loan?

Single-payment loans can come in several different forms. Many loans require the borrower to make several monthly payments until their loan is paid in full. However, single-payment loans are paid back with one large payment by the due date decided by the lender. One common form of a single-payment loan is called a payday loan. According to the U.S. Chamber of Commerce, approximately 12 million Americans borrow funds using payday loans each year!1

Loans are a big part of today’s society and understanding them is one key to financial success. Loans are typically issued by financial institutions (such as banks), corporations, and governments. There are many types of loans, so how can you know which one to pick?

There are several types of loans out there. The easiest way to break them down is by “secured” and “unsecured.” A secured loan is one that requires the borrower to offer up collateral in order to take out the loan. This way, if the customer defaults on the loan, the lender can sell the collateral to cover their loss. An unsecured loan is the opposite in that it requires no collateral.

Single Payment Loans

FAQ

What are single-payment loans secured by?

What is a single-payment loan called?

What is a type of single-payment loan?

Which of the following regarding single-payment loans is true?

Is a mortgage a secured option?

A mortgage is a secured loan with real-estate as collateral. Another typical example of a secured option is a car loan. If Mike can’t pay his $175 per month as compensation for his loan, the lender might seize his new car. That’s why making your loan payments is important.

What is a single payment loan?

A single-payment loan is a loan that borrowers must repay in one lump sum, including interest and additional fees. A single-payment loan requires the borrower to repay the entire principal balance and the interest in one lump sum on the due date. What Is A Single-payment Loan? Single-payment loans can come in several different forms.

How do secured personal loans work?

Secured personal loans work by allowing borrowers to use their assets as collateral. This protects lenders against nonpayment from borrowers and allows them to offer lower interest rates or larger loan amounts than would otherwise be available. To secure a loan, a borrower must provide an item of value, such as their home or car, as collateral.

Do secured loans have higher interest rates?

Secured loans may allow borrowers to enjoy lower interest rates, as they present a lower risk to lenders. However, certain types of secured loans—including bad credit personal loans and short-term installment loans —can carry higher interest rates.