Most preapprovals are good for 90 days, but some lenders issue 60-day and 30-day limits. Best practice is to get preapproved for a mortgage just before you begin serious house hunting.

Experian, TransUnion and Equifax now offer all U.S. consumers free weekly credit reports through AnnualCreditReport.com.

When a lender issues a mortgage preapproval letter, the document will indicate that it is only valid for a limited period of time. Most lenders issue 90-day preapprovals, but each lender sets its own time limit, and letters with 60-day and 30-day limits are issued as well.

Because preapprovals have relatively short shelf lives, its wise to time your preapproval applications carefully so you can use them effectively. Its also important to know how long a preapproval will last before you apply. Heres an overview of how to apply for a preapproval and how to use it efficiently.

Getting pre-approved for a mortgage is one of the most important steps when buying a home. It shows sellers you are a serious buyer and gets the tricky mortgage process started early. But mortgage pre-approvals do expire, usually within 60-90 days. Here’s what homebuyers need to know about how long mortgage pre-approvals last and why they expire.

What is Mortgage Pre-Approval?

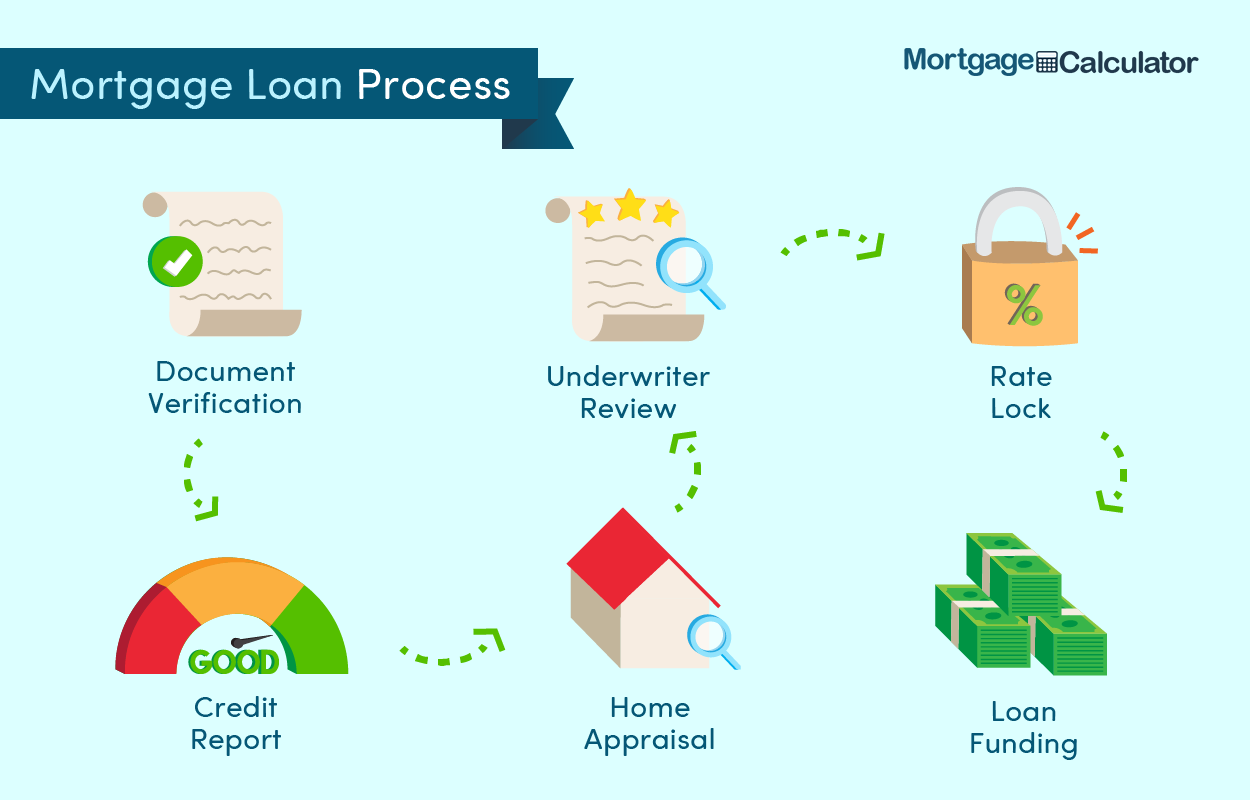

Pre-approval is when a lender evaluates your finances and credit to determine the loan amount you qualify for. Pre-approvals require submitting paperwork like pay stubs tax returns and bank statements so the lender can verify your income, assets, debts, and credit score.

The pre-approval letter estimates the mortgage amount, interest rate, and monthly payments you could qualify for. It doesn’t guarantee approval, but shows sellers you are qualified and ready to move forward.

Pre-approval is different than pre-qualification, which only requires stating your income and debts without documentation. Pre-qualification isn’t as strong of an offer as pre-approval.

Why Do Mortgage Pre-Approvals Expire?

There are a few key reasons mortgage pre-approvals expire after 60-90 days

-

Income and Employment – Lenders want to see stable, consistent income. If you get a new job after the pre-approval, the lender will want updated proof of employment.

-

Credit Score – Your credit score could change in 60-90 days, Lenders need to pull your credit again to guarantee you still qualify for the same rates and terms

-

Rates and Regulations – Mortgage rates and regulations fluctuate frequently. After 60-90 days, your pre-approval may no longer be valid.

-

Paperwork Expiration – Documents like bank statements and pay stubs have short validity periods. After 60-90 days, you’ll need to submit updated paperwork.

-

Housing Market Changes – Home prices can change quickly, especially in competitive markets. Your approved loan amount might change after 60-90 days.

Keeping pre-approvals short allows lenders to re-verify your finances and ensure your home buying ability is current.

How to Extend a Pre-Approval

If your mortgage pre-approval expires before you find a home, you can usually get it extended by:

- Contacting your lender as soon as possible, ideally 15-30 days before expiration

- Updating any expired paperwork like pay stubs and bank statements

- Allowing another credit check to show your score is still solid

- Providing proof of major financial changes like a job change

- Signing a rate lock if you want to lock the interest rate

As long as you still qualify and your financial situation is stable, lenders will often grant 30-60 day extensions. Make sure to request extensions proactively, not after the pre-approval expires.

Shopping Around Before Your Pre-Approval Expires

It’s smart to shop around with multiple lenders when getting a mortgage pre-approval. But doing too many applications at once can hurt your credit score.

The ideal strategy is to start with your top lender choice, then if you aren’t satisfied, apply with another lender once the first pre-approval expires. This avoids having too many hard credit checks at once.

You can also ask other lenders to pre-qualify you without a hard credit check. Then only do a full pre-approval application with your top choices. Shopping strategically allows you to find the best rates while minimizing credit impact.

Preparing for a Strong Pre-Approval Application

You can boost your chances of getting a great pre-approval offer by:

- Maintaining a credit score over 740

- Having a low debt-to-income ratio below 36%

- Having at least a 15-20% down payment saved

- Gathering required paperwork like tax returns and bank statements

- Correcting any errors on your credit report

A strong pre-approval application represents you as a low-risk, qualified buyer. That makes sellers more confident about accepting your offer.

What to Do When Your Pre-Approval Expires

If your pre-approval expires before finding a home, don’t worry. You have a few options:

- Request an extension with your current lender if you still want to work with them

- Shop around and apply for a new pre-approval with another lender

- Consider switching to a pre-qualification if you need more time to find a home

- Build up your finances, credit score, or down payment before reapplying

The most important thing is communicating with lenders before your pre-approval expires. They can guide you on the best options to move forward with a strong mortgage offer.

Final Tips for Pre-Approval Success

Here are some final tips for making the most of your mortgage pre-approval:

- Only apply for pre-approval when you’re seriously ready to buy a home.

- Compare multiple lender rate quotes and fees to find the best deals.

- Lock in an interest rate once you’re under contract to avoid fluctuations.

- Understand all the costs at closing so there are no surprises.

- Be proactive about extending your pre-approval and updating paperwork.

- Discuss any major financial changes with your lender right away.

- Allow 2-4 weeks to complete the full mortgage approval once under contract.

Getting pre-approved is an essential part of the home buying process. Following mortgage best practices will set you up for success through the pre-approval and the final mortgage approval. With the right preparation, you can get a pre-approval that transitions smoothly into your dream home loan.

What Is a Mortgage Preapproval?

A mortgage preapproval is a document from a lender indicating you are conditionally approved for a mortgage loan—up to a specific amount—to buy a house. It usually specifies the type of loan you qualify for and the interest rate the lender would charge you upon completion of a full mortgage application.

Applying for preapproval is essentially the same as applying for a mortgage. Your lender will assess your income, assets, debt and employment history, and review your credit report and credit score. Keep in mind, preapproval should only be viewed as a preliminary document. This means your lender will not fully approve your loan or finalize terms until they verify information about you and any other borrowers on the loan application as well as the property you wish to buy.

A mortgage preapproval letter is valuable because it attests to your ability to follow through on a purchase offer. It can provide a significant advantage in competitive housing markets: When a seller is considering several similar offers for a home, a bidder with preapproved financing may have an edge over others who do not, on the grounds that your ability to secure financing is more certain than that of rival bidders. In hot housing markets, sellers may only consider offers from prospective buyers who are already preapproved for a loan.

Gather Your Financial Information

Gathering your financial documents—including those related to employment, income and assets—can help your application process go smoothly. Documents lenders typically require include the following:

- Personal information: Youll need to provide your drivers license, passport or other proof of identity. You dont need to be a U.S. citizen to apply for a mortgage. You are eligible for a mortgage as a foreign national if you can prove your residency status.

- Income information: Be prepared to submit recent pay stubs, account statements and your past two annual tax returns.

- Asset and debt information: Youll need to provide your lender with account statements that show your savings, investments, property and other assets. Conversely, your lender will want to see your current credit card, loan and other debt balances. Ultimately, lenders want to see that you have the financial means to cover the mortgage down payment and to help you afford your loan payments if there is a change in your job or income.

How long is a Home Loan Approval good for?

FAQ

How long is mortgage approval good for?

How long is a loan good for once approved?

Does a mortgage approval expire?

How long is a mortgage loan valid for?

How long is a preapproved loan valid?

In most cases, it’s valid for around 60 – 90 days. Your financial situation can change substantially within a few months, and many lenders require you to get preapproved again if you’ve gone beyond the 90-day mark. It can, however, be a good thing for a borrower’s financial situation to change.

How long does a mortgage preapproval last?

Now, regarding the duration of a mortgage preapproval, it can vary depending on the lender.Here are some typical timeframes: – **On average**, a mortgage preapproval typically lasts for about **60 to

When should I get a mortgage pre-approval?

The general guideline is to get a mortgage pre-approval at least 90 days before you plan to buy to give you enough time to find a home and close on your loan. While you can wait to get pre-approved until you’ve found a home you’re ready to make an offer on, a pre-approval can help you during your home search — some agents even prefer it.

Do mortgage lenders provide pre-approvals?

Mortgage lenders provide pre-approvals. To get a pre-approval, the mortgage lender will look at: Mortgage pre-approvals only take a few minutes to complete and can be done online, over the phone, or in-person — whichever you prefer. Learn more about how pre-approvals impact your credit score. When Should You Apply for Pre-Approval?